Sales Tax vs. Use Tax in New Jersey: What Businesses Often Get Wrong

Most finance teams can explain New Jersey's 6.625% sales tax rate without much effort. Far fewer can explain exactly when that rate applies to a purchase versus when the business itself owes use tax on a transaction where no sales tax was charged. The distinction matters more than it seems. Getting it wrong does not just create an audit risk. It creates a pattern of errors that compounds across every out-of-state purchase, every cross-border transaction, and every vendor invoice that arrives without a tax line.

This blog breaks down the difference between sales tax and use tax in New Jersey, explains the scenarios where each applies, walks through the mistakes that trip up even experienced AP teams, and explains what it takes to get it right consistently.

For a broader overview of New Jersey's sales tax structure, including rates, exemptions, and Urban Enterprise Zone rules, see the New Jersey State Sales Tax guide.

The Basic Distinction: Who Collects vs. Who Owes

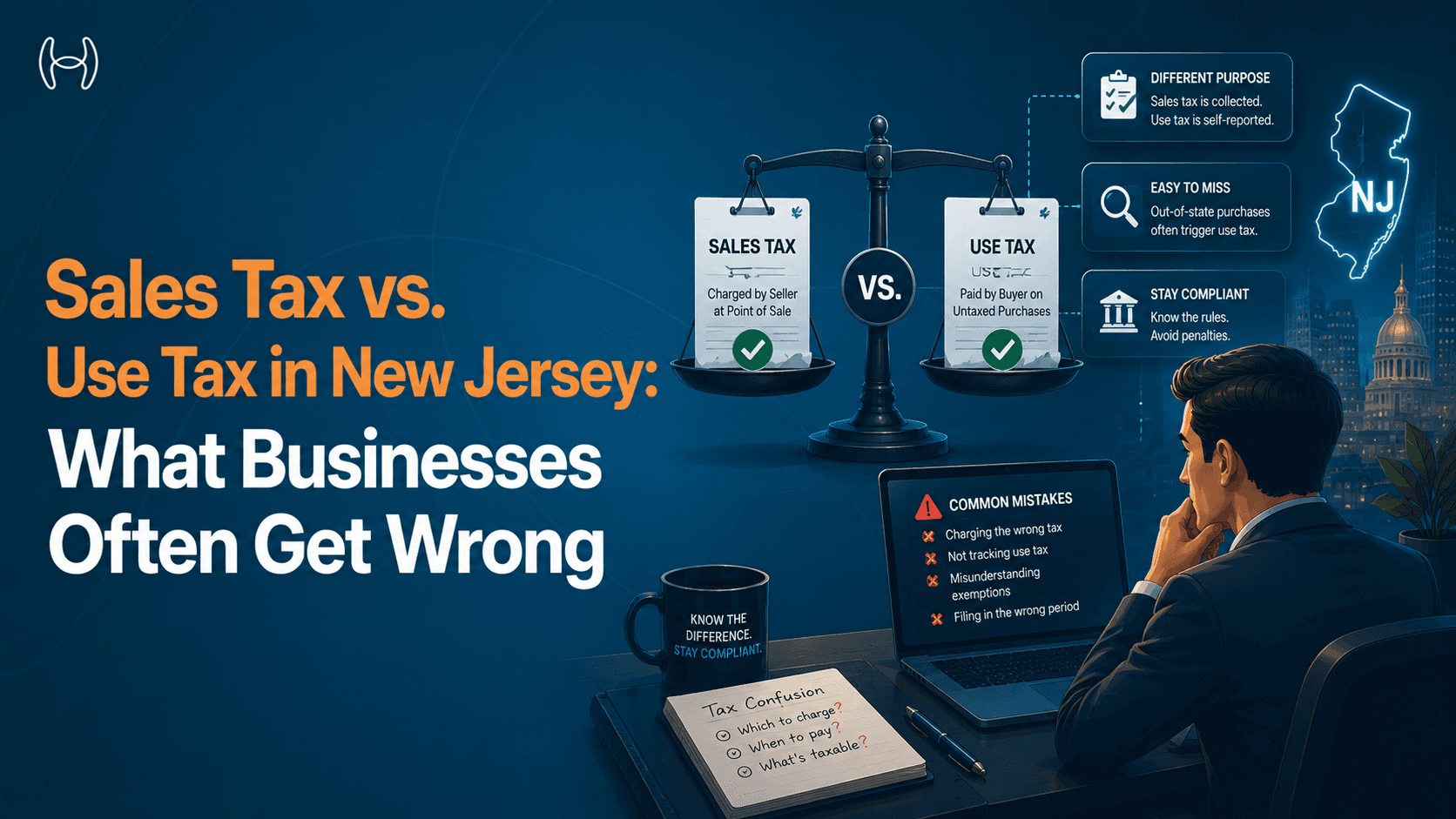

Sales tax and use tax are two sides of the same compliance obligation. They cover the same taxable transactions. The difference is in who is responsible for remitting the tax and under what circumstances.

Sales tax is collected by the seller at the point of sale and remitted to the state. When a business buys office supplies from a New Jersey vendor, the vendor charges 6.625% and sends that amount to the New Jersey Division of Taxation. The buyer pays it but is not responsible for filing anything related to that transaction.

Use tax is a self-assessed tax owed by the buyer when sales tax was not collected by the seller. New Jersey imposes use tax at the same 6.625% rate as sales tax. If a business purchases goods or taxable services from an out-of-state vendor who did not charge New Jersey sales tax, and those goods are used, stored, or consumed in New Jersey, the buyer owes use tax on that purchase and must report and remit it directly.

The practical way to think about it: use tax fills the gap where sales tax was not collected. The two taxes are designed to ensure that equivalent taxable transactions bear the same tax burden regardless of where the seller is located.

Definitions

Sales Tax: A transaction tax imposed on the sale of taxable goods and services in New Jersey. The seller collects it from the buyer at the point of sale and remits it to the New Jersey Division of Taxation. The buyer has no direct filing obligation for that transaction.

Use Tax: A self-assessed tax imposed on the buyer for the use, storage, or consumption of taxable goods and services in New Jersey when sales tax was not collected by the seller. The buyer is responsible for calculating, reporting, and remitting use tax directly to the state. It applies at the same rate as sales tax and covers the same categories of taxable goods and services.

Sales Tax vs. Use Tax: Side by Side

Sales Tax | Use Tax | |

Who pays | Buyer | Buyer |

Who collects and remits | Seller | Buyer, self-assessed |

When it applies | Sale of taxable goods or services by a NJ-registered seller | Purchase where sales tax was not collected by the seller |

Rate in New Jersey | 6.625% | 6.625% |

What triggers it | Transaction with a seller who has NJ nexus | Out-of-state purchase, online purchase from unregistered seller, or exemption that later lapses |

How it is reported | Seller files directly with the Division of Taxation | Buyer reports on Form ST-50 (if registered for sales tax) or Form ST-18 (standalone use tax filer) |

Who is audited for compliance | Seller | Buyer |

Credit for tax paid in another state | N/A | Yes, up to the NJ rate of 6.625% |

When Use Tax Applies: The Scenarios That Matter

Out-of-State Purchases Brought Into New Jersey

This is the most common use tax trigger. A business purchases equipment or supplies from a vendor based in another state. The out-of-state vendor either has no New Jersey nexus and does not charge sales tax, or the buyer provides a resale certificate that later turns out not to apply. The goods arrive in New Jersey, where the business uses them. Use tax is owed on the purchase price.

The same logic applies to goods purchased while employees are traveling. If a company employee buys supplies in Pennsylvania and brings them back to the New Jersey office, use tax may apply on those items if Pennsylvania sales tax was not paid at a rate equal to or greater than New Jersey's rate.

Online Purchases from Sellers Without New Jersey Nexus

Before the 2018 South Dakota v. Wayfair Supreme Court decision, many remote sellers did not collect New Jersey sales tax because they lacked physical presence in the state. Businesses that purchased from those sellers owed use tax on those transactions even though the seller did not charge anything. After Wayfair, New Jersey adopted economic nexus rules requiring remote sellers who exceed $100,000 in New Jersey sales or 200 transactions annually to register and collect sales tax. However, some smaller remote sellers still may not be registered. Use tax obligations remain for any taxable purchase where sales tax was not collected.

Taxable Services Sourced from Outside New Jersey

New Jersey taxes certain services, including repair and maintenance services, certain professional services, and information services. If a business contracts with an out-of-state provider for a taxable service that is delivered into or consumed in New Jersey, and that provider does not charge New Jersey sales tax, the buyer may owe use tax on the service fee.

Goods Purchased for Resale That Are Later Used Internally

This scenario catches businesses off guard. A business purchases goods under a resale exemption certificate. The goods are later withdrawn from inventory and used internally rather than resold. The original exemption no longer applies to those items. The business owes use tax based on the purchase price or fair market value of the goods at the time they are put to taxable use.

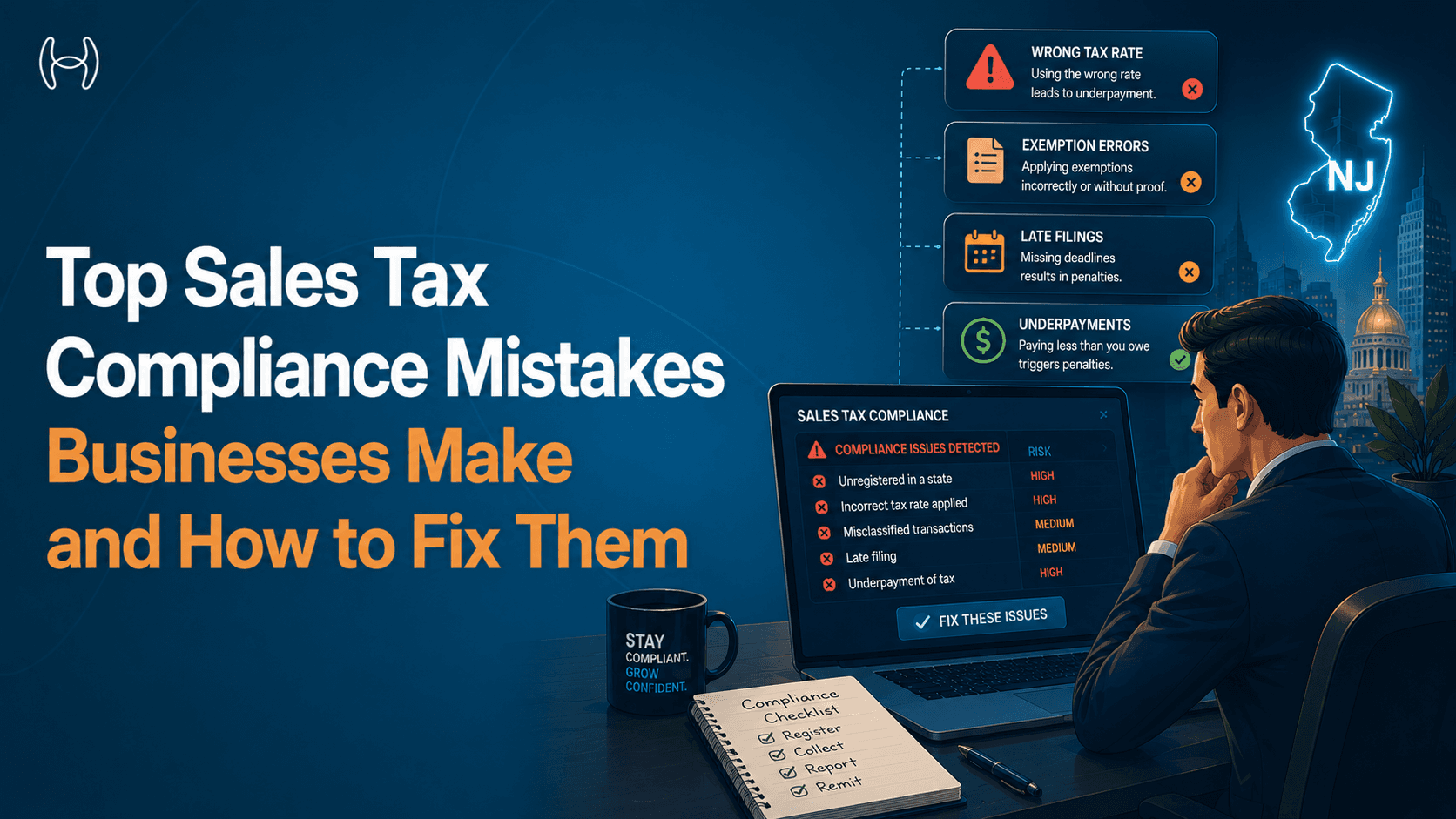

Where the Confusion Starts: Common Mistakes Businesses Make

Assuming No Invoice Tax Line Means No Tax Obligation

When a vendor invoice arrives without a sales tax line, many AP teams process it as a non-taxable transaction. The invoice may genuinely be non-taxable. Or the vendor may not be registered in New Jersey and simply did not charge the tax they should have, or that the buyer now owes as use tax. The invoice itself does not tell you which situation you are in. The answer depends on where the vendor is registered, where the goods are delivered, what the goods are, and whether an exemption applies.

Applying Exemptions That Do Not Transfer

New Jersey offers exemptions for groceries, prescription drugs, medical devices, manufacturing equipment, and certain other categories. Some businesses assume that if a category of goods is exempt from sales tax, it is also exempt from use tax. That is generally correct since the same exemptions apply to both. The mistake is applying an exemption that does not fit the actual transaction. For example, a manufacturer may purchase a piece of equipment believing it qualifies for the manufacturing exemption, but if the equipment is primarily used in an administrative function rather than directly in production, the exemption does not apply and use tax is owed.

Missing Cross-Border Complexity Near New York and Pennsylvania

New Jersey shares borders with New York and Pennsylvania, two states with their own sales tax rates and rules. Businesses operating near these borders often have vendors, employees, and inventory flowing across state lines regularly. The rate paid in another state can offset the New Jersey use tax obligation, but only if the tax was actually paid, and only up to the New Jersey rate. Tracking which transactions were taxed, at what rate, and in which state requires more than a quick review of the invoice.

Not Filing Use Tax Returns

New Jersey requires businesses to report and remit use tax on a regular basis. Many businesses are unaware that they have a use tax filing obligation separate from any sales tax registration. Businesses that do not file use tax returns are not off the hook simply because no one has asked. The obligation accrues from the date of the taxable purchase, and the Division of Taxation can assess use tax, interest, and penalties retroactively during an audit.

A Practical Decision Framework

The question that should run through every AP transaction involving goods or taxable services is straightforward:

Was New Jersey sales tax collected by the vendor?

│

├── YES → Verify the rate and amount are correct.

│ No further use tax obligation for this purchase.

│

└── NO → Is this purchase taxable in New Jersey?

│

├── NO → Document the exemption basis. No tax due.

│

└── YES → Was tax paid to another state?

│

├── YES → Was it paid at a rate equal to or higher

│ than NJ's 6.625%?

│ │

│ ├── YES → No additional NJ use tax due.

│ │

│ └── NO → NJ use tax due on the difference.

│

└── NO → NJ use tax due at 6.625% on purchase price.

This flowchart covers the majority of transactions. Edge cases, particularly around services, digital products, and mixed-use goods, require additional analysis.

Real Examples That Illustrate the Rules

E-Commerce Business Purchasing Fulfillment Equipment

A New Jersey-based e-commerce company orders warehouse shelving units from a manufacturer based in Ohio. The Ohio seller is a small operation below New Jersey's economic nexus threshold and does not charge New Jersey sales tax. The shelving is delivered to the company's New Jersey warehouse. The company owes New Jersey use tax on the full purchase price of the shelving at 6.625%. Because the seller did not collect it, the company must self-assess and remit it on its use tax return.

A Professional Services Firm Buying Software Subscriptions

A New Jersey professional services firm purchases a cloud-based project management software subscription from a vendor headquartered in another state. New Jersey taxes certain digital products and software services. If the vendor does not have New Jersey nexus and does not collect sales tax on the subscription, the firm owes use tax on the subscription fees for each period the software is used in New Jersey. This is a use tax obligation that many service firms do not recognize because they assume software subscriptions are not taxable.

A Retailer Purchasing Display Fixtures in New York

A retailer with stores on both sides of the New York City and New Jersey border purchases display fixtures in New York City and pays 8.875% New York City sales tax. The fixtures are then brought to the New Jersey location. New Jersey use tax is technically triggered when taxable goods are brought into the state. However, because the rate paid in New York City (8.875%) exceeds New Jersey's rate (6.625%), no additional New Jersey use tax is owed. The New York City tax fully satisfies the New Jersey use tax obligation for that purchase.

A Manufacturer Misusing a Resale Certificate

A New Jersey manufacturer purchases cleaning supplies using a resale certificate, intending to incorporate them into products. The supplies are instead used to clean the factory floor and administrative offices. The resale exemption does not apply. The manufacturer owes use tax on those supplies from the point at which they were applied to a taxable use. This is one of the most common audit findings in manufacturing.

The Table That Most Finance Teams Need

Scenario | Sales Tax Charged by Vendor? | Use Tax Owed by Buyer? | Rate |

NJ vendor, goods delivered in NJ | Yes | No | 6.625% via vendor |

Out-of-state vendor, no NJ nexus, goods used in NJ | No | Yes | 6.625% self-assessed |

Out-of-state vendor, tax paid at lower rate | Yes, at a lower rate | Yes, on the difference | Difference up to 6.625% |

Out-of-state vendor, tax paid at equal or higher rate | Yes, by another state | No | N/A |

Goods purchased exempt, later used internally | No | Yes | 6.625% on fair market value |

NJ-exempt goods (groceries, Rx drugs) | No | No | N/A |

Taxable digital product, out-of-state vendor, no NJ registration | No | Yes | 6.625% self-assessed |

Service purchased from out-of-state provider, taxable in NJ | No | Yes | 6.625% self-assessed |

Why Manual Processes Break Down Here

The rules above are clear enough in isolation. The difficulty is applying them consistently across hundreds or thousands of transactions per month, each with a different vendor, different goods category, different origin and destination, and different exemption status.

Most AP teams rely on a combination of invoice review and manual lookups to determine tax treatment. This works when volume is low and vendors are familiar. It stops working when the business grows, when vendors are added across multiple states, or when the AP team is handling cross-border purchases regularly.

The most common failure point is not ignorance of the rules. It is the time and attention required to apply the rules correctly to every transaction. A missed use tax accrual on one invoice is small. A pattern of missed accruals across a year of transactions creates a material liability.

Accurately categorizing line items for tax purposes is its own challenge, and it sits upstream of the sales tax versus use tax question. If line items are miscategorized, the tax analysis that follows is wrong regardless of how well the rules are understood.

How Hyperbots Handles Sales Tax vs. Use Tax Automatically

Hyperbots' Sales Tax Verification Co-Pilot is built to address exactly this problem. When an invoice is processed, the Co-Pilot extracts and validates the origin and destination addresses, classifies each line item against applicable tax categories, and determines whether the vendor charged the correct tax for the jurisdiction.

For transactions where a vendor did not charge New Jersey sales tax, the system identifies whether use tax should apply based on the nature of the goods, the delivery location, and the applicable tax category. This happens at the line-item level, not just at the invoice level, which matters because a single invoice may contain both taxable and exempt items that require different treatment.

The Sales Tax Verification Co-Pilot integrates with your ERP and processes invoices with 99.8% extraction accuracy. Up to 80% of invoices move through the full cycle without manual intervention, which means your AP team's attention is directed to the exceptions that genuinely require human review rather than routine tax lookups on every transaction.

For businesses managing use tax obligations across multiple vendors and states, the Co-Pilot maintains consistent logic across all transactions. The same rules that apply to a New Jersey vendor's invoice apply to an out-of-state vendor's invoice. The decision is made by the system based on the transaction data, not by whoever happens to be reviewing the invoice that day.

Tax mismatch identification and reporting flags discrepancies automatically, including cases where sales tax was charged incorrectly, where use tax accruals are needed, or where an exemption was applied to a transaction that does not qualify. This reduces the cost of invoice processing by up to 80% compared to manual review processes, while maintaining an audit-ready record of every decision.

The system goes live in one month, with no custom model training required. It connects to your existing ERP and begins processing from day one of deployment.

What This Means for Use Tax Accruals

Use tax is not just a compliance filing. It is an accounting obligation. When a business owes use tax on a purchase and does not accrue it, the financial statements understate the tax liability for that period. This creates both a compliance issue and a financial reporting issue.

For businesses with consistent use tax exposure, setting up a proper accrual process is essential. The accrual should be estimated based on the volume of out-of-state purchases, the applicable rate, and any exemptions that apply. It should be reversed or settled when the actual use tax return is filed and payment is made.

Where Hyperbots helps in this context is upstream of the accrual itself. The Sales Tax Verification Co-Pilot flags invoices where sales tax was not charged but should have been, or where the tax charged does not match what the jurisdiction requires. Those flags are what tell your finance team that a use tax liability exists for a given transaction. Rather than discovering these gaps during a quarterly review or an audit, the team gets a clear, transaction-level signal at the point of invoice processing. That signal is what makes the accrual process reliable. The finance team still books the accrual, but they are working from accurate, complete information rather than trying to reconstruct which purchases created a liability after the fact.

Building a Use Tax Process That Holds Up in an Audit

The New Jersey Division of Taxation audits use tax compliance. Auditors look at purchase records, vendor invoices, exemption certificates, and use tax returns. The documentation requirements are not complex, but they require consistency from transaction to transaction.

For every purchase where use tax applies or was considered, the business should be able to show the invoice, the basis for the tax determination, and either the use tax accrual or the basis for exemption. For every exemption certificate used, the certificate should be on file and valid for the period of the purchase.

Audit trails for sales tax verification maintained by Hyperbots cover every invoice processed, every tax determination made, and every exception flagged. The audit trail is maintained automatically with timestamps, so the documentation that auditors require is generated as part of normal processing rather than assembled after the fact.

A Note on Digital Products and Cloud Services

New Jersey taxes specified digital products and certain cloud services. This is an area where use tax compliance is frequently missed. A business subscribing to a SaaS platform or purchasing a software license from an out-of-state provider may owe New Jersey use tax on those fees if the provider does not collect sales tax. Pure cloud storage without accompanying software access is a more nuanced category and may not qualify as a specified digital product under New Jersey's definitions.

The rules around digital products are detailed and category-specific. Not every cloud service is taxable in New Jersey. Whether a service is taxable depends on what the service does, how it is delivered, and whether it falls within the state's definitions of specified digital products or information services. Getting this right requires category-level analysis of the service, not just a general assumption.

The tax category classification capability within Hyperbots' Co-Pilot handles this at the line-item level, applying the correct tax treatment to each service type based on New Jersey's definitions, rather than applying a blanket rule to all digital purchases.

Frequently Asked Questions

Is the use tax rate in New Jersey the same as the sales tax rate?

Yes. New Jersey's use tax rate is 6.625%, the same as the state sales tax rate. The two taxes are designed to be equivalent. Use tax applies when sales tax was not collected at the point of purchase, so the total tax burden on a taxable transaction is the same regardless of whether the seller or the buyer remits it.

Do I owe New Jersey use tax if I already paid sales tax in another state?

It depends on the rate. If you paid sales tax in another state at a rate equal to or greater than 6.625%, no additional New Jersey use tax is owed. If the rate you paid was lower, you owe the difference. For example, if you paid 4% sales tax in another state on a taxable purchase brought into New Jersey, you would owe an additional 2.625% as New Jersey use tax.

How does my business report and pay use tax in New Jersey?

Businesses registered in New Jersey for sales tax report use tax on their combined sales and use tax return, Form ST-50. Use tax accrued during the period is reported alongside any sales tax collected. Businesses that are not registered for sales tax but have standalone use tax obligations must register with the New Jersey Division of Taxation separately and file Form ST-18, the Use Tax Return. The filing frequency is typically quarterly for new registrants, with monthly filing required once certain revenue thresholds are crossed.

Are digital products and SaaS subscriptions subject to use tax in New Jersey?

New Jersey taxes specified digital products, which includes electronically delivered software, digital audio and video files, and certain information services. A SaaS subscription may be taxable depending on how it is classified under New Jersey's rules. Pure cloud storage without accompanying software access is a more nuanced category and may not qualify as a specified digital product under New Jersey's definitions. If an out-of-state provider delivers a taxable digital product or service to a New Jersey customer and does not collect sales tax, the buyer owes use tax on those fees. The category-level analysis matters here because not every cloud service falls within the taxable definitions, and the correct determination depends on what the service actually does.

What happens if a vendor charges sales tax on a transaction that should have been exempt?

The buyer can request a refund or credit from the vendor for incorrectly charged sales tax. If the vendor has already remitted the tax to the state, the vendor must file for a refund from the Division of Taxation and pass it back to the buyer. AP teams should flag overcharged sales tax during invoice review rather than accepting the charge as correct. This is a common source of tax overpayment that goes undetected when invoice validation is done manually.

If we buy goods for resale and later use them internally, when does the use tax obligation begin?

The use tax obligation begins on the date the goods are withdrawn from resale inventory and put to an internal taxable use. The taxable amount is typically the purchase price or the fair market value of the goods at the time of the change in use. Businesses should track these withdrawals and accrue use tax in the period in which they occur, not at the time of the original purchase.

Does the economic nexus threshold affect our use tax obligations as a buyer?

Economic nexus rules determine whether a remote seller must collect and remit New Jersey sales tax. They do not change the buyer's use tax obligation. If a seller is below the threshold and does not collect sales tax, the buyer still owes use tax on taxable purchases delivered into New Jersey. The threshold is relevant to whether the seller collects the tax, not to whether the transaction is taxable.

The Bottom Line

Sales tax and use tax in New Jersey follow consistent rules. The challenge is not understanding the rules. The challenge is applying them correctly to every transaction, every month, without gaps or inconsistencies.

The most common mistakes, including processing invoices without a tax line as non-taxable, missing use tax on out-of-state purchases, and misapplying exemptions, all have the same root cause. The determination requires more information and more analysis than a quick invoice review provides, and the volume of transactions in most AP functions makes thorough manual review impractical.

AI-driven tax compliance solves this at scale. Every transaction gets the same level of analysis regardless of volume, and the system maintains the documentation to support every decision it makes.

See it in action with a demo or start your free trial today.

For a full overview of New Jersey's sales tax structure, rates, exemptions, and Urban Enterprise Zone rules, visit the New Jersey State Sales Tax guide.