Taxable vs Exempt Products in Pennsylvania: Common Business Mistakes

A practical guide to Pennsylvania sales tax rules, product classification mistakes, and how businesses reduce compliance risk across taxable and exempt items

Pennsylvania has one of the more nuanced sales tax systems in the United States. Its 6 percent statewide rate is straightforward enough, but the list of what is taxable and what is exempt does not always follow the logic businesses expect. Clothing is largely exempt. Most groceries are exempt. But prepared food is taxable. Digital products are taxable. And the line between exempt and taxable shifts depending on the context in which a product is sold.

This guide is written for business owners, finance managers, AP teams, and tax compliance professionals operating in Pennsylvania, whether you are a retailer, a digital product seller, a food service operator, or a multi-category business trying to get classification right across everything you sell. It is also relevant for businesses in other states selling to Pennsylvania customers.

These distinctions create real compliance risk. A misclassified product generates either a tax liability the business did not collect or an overcharge that damages customer relationships. This guide covers the main taxable and exempt categories, the specific distinctions that trip businesses up most often, and how AI automation reduces the classification burden that creates these mistakes in the first place.

For a comprehensive overview of how Pennsylvania's entire sales tax system works, including vendor licence requirements, filing frequencies, and use tax obligations, the guide to Pennsylvania's sales tax system covers the full picture.

Pennsylvania Sales Tax Rates: Statewide, Allegheny County, and Philadelphia

Pennsylvania charges a statewide sales and use tax of 6 percent on most tangible goods and certain services. Two counties carry higher rates: Allegheny County adds 1 percent for a total of 7 percent, and Philadelphia adds 2 percent for a total of 8 percent.

Businesses selling to customers in Philadelphia or Allegheny County must apply the correct local rate, not just the statewide 6 percent. Collecting only 6 percent from a Philadelphia customer creates a personal liability for the 2 percent difference. This is one of the most common and most expensive mistakes businesses make before they fully understand Pennsylvania's rate structure.

The same rate applies as a use tax when a business purchases a taxable item from an out-of-state seller who does not collect Pennsylvania sales tax. The business owes that tax directly to the Department of Revenue.

What Products Are Taxable in Pennsylvania

Most tangible personal property sold at retail is taxable in Pennsylvania. This includes electronics, furniture, household goods, sporting goods, cosmetics, toys, and computer hardware.

Beyond physical goods, several categories that businesses sometimes assume are exempt are in fact taxable.

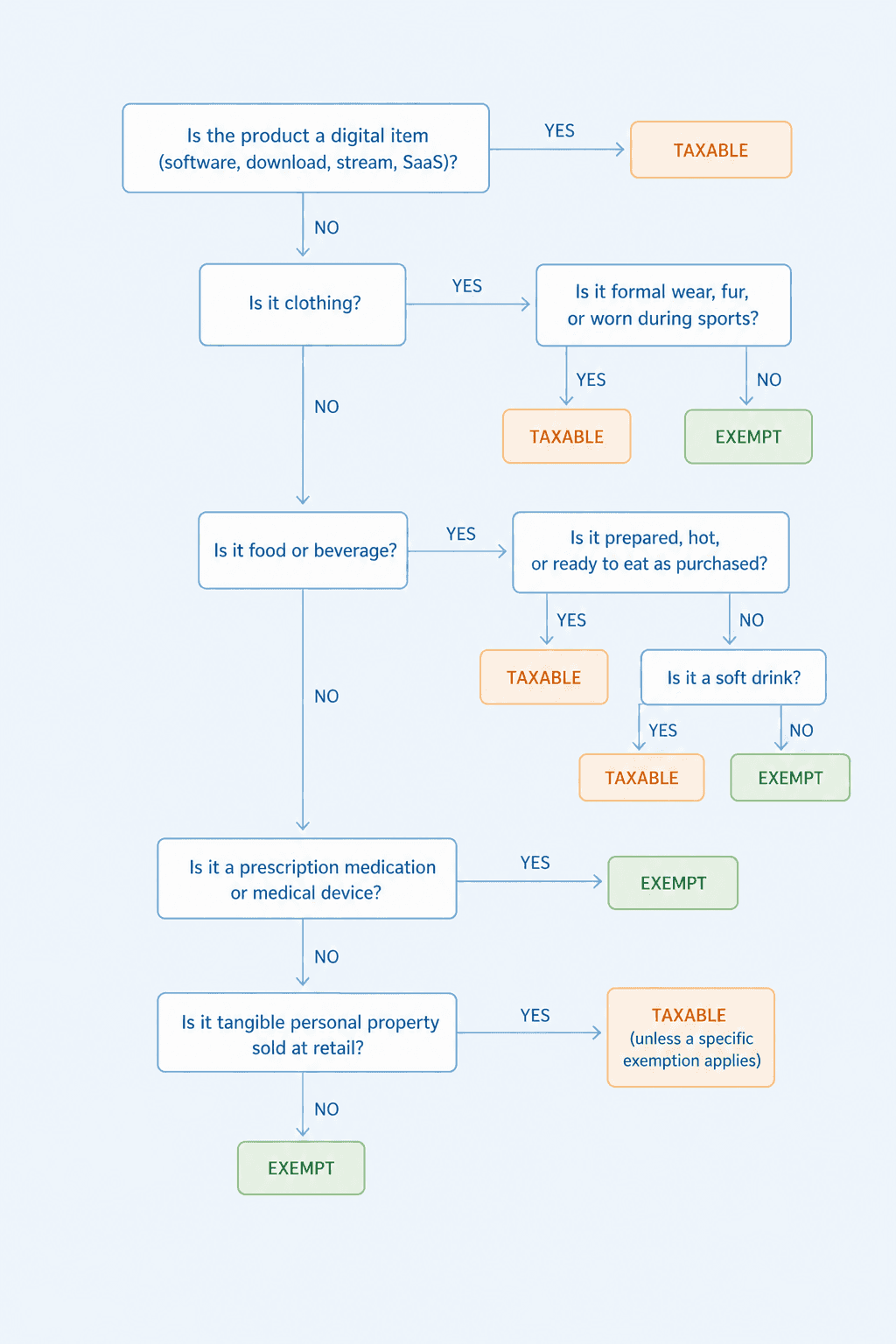

Prepared and ready-to-eat food. Sandwiches, hot food, salad bar items, restaurant meals, and catered food are all taxable regardless of where they are purchased. Soft drinks are always taxable, even when sold at a grocery store. Hand-dipped ice cream sold at retail is taxable. The practical test is whether the item is ready to eat as purchased. If it is, it is taxable. If it requires preparation at home, it is likely exempt.

Digital products. Pennsylvania taxes downloaded software, digital books, digital music, streaming services, and SaaS products that provide software functionality. Canned software, meaning software not custom-built for a specific purchaser, is taxable whether delivered on physical media or electronically. Any transfer of a digital product for consideration is taxable unless a specific exemption applies.

Certain services. Most services in Pennsylvania are exempt, but several are taxable: telecommunications, hotel accommodations, vehicle parking, vehicle rental, certain cleaning and repair services on tangible property, pest control, and personal care services such as tanning.

What Products Are Exempt from Pennsylvania Sales Tax

Pennsylvania's exemption list is broader than most states, which creates as much confusion as the taxable list does.

Most clothing. Everyday clothing is exempt in Pennsylvania: shirts, trousers, shoes, underwear, work uniforms, safety clothing, hosiery, scarves, and similar items. The exemption is intentionally broad. However, several categories are taxable: formal day or evening apparel, articles made primarily of real or synthetic fur, and sporting goods or clothing normally worn during sports activities. Tuxedos are taxable. A business suit is not. Football pads are taxable. A team jersey worn off the field is not.

Unprepared groceries. Most food sold at grocery stores and food retailers is exempt: produce, canned goods, meat and cheese by the pound, milk, bread, frozen foods, prepackaged ice cream, baked goods sold for home consumption, and unprepared seafood. Candy and gum sold at a retail store are also exempt. The exemption ends when food is prepared and ready to eat.

Prescription medications and medical supplies. Prescription and non-prescription medicines, medical devices, eyeglasses prescribed by a licensed professional, artificial limbs, hearing devices, and similar therapeutic equipment are all exempt.

Resale purchases. Goods purchased for resale rather than personal use are exempt, provided the purchaser provides a valid resale certificate.

Most standalone services. Legal services, accounting services, medical services, educational services, and most personal professional services are exempt unless they involve the sale or installation of taxable goods.

Common Pennsylvania Sales Tax Classification Mistakes

Understanding the broad categories is one thing. The classification errors that generate audit findings and back-tax liabilities tend to happen at the edges of those categories, where the rules are less obvious.

Grocery versus prepared food. A grocery store that sells a rotisserie chicken, a hot sandwich from a deli counter, or a ready-to-eat salad from a salad bar must collect sales tax on those items, even though most of its other food products are exempt. Businesses that sell both exempt groceries and taxable prepared food in the same location need systems that classify each product correctly at the point of sale, not after the fact.

Clothing exemptions that are narrower than expected. Businesses that assume all clothing is exempt in Pennsylvania and fail to tax formal wear, fur articles, and sporting apparel are creating a liability. A bridal shop that does not tax wedding gowns, a fur retailer that does not tax coats, or a sporting goods retailer that does not tax clothing designed for active sports use are all making taxable sales without collecting the required tax.

Digital products that businesses treat as services. A common mistake is treating a software subscription, a streaming licence, or a digital download as a service and therefore exempt. Pennsylvania's tax code is explicit: sales and use tax applies to any transfer of a digital product where the purchaser pays consideration. SaaS platforms that provide software functionality are taxable. Businesses purchasing or selling digital products in Pennsylvania need to treat them as taxable goods unless a specific exemption applies.

Soft drinks purchased at exempt food retailers. Businesses operating food retail that stock soft drinks sometimes assume the grocery exemption covers all food and beverages. It does not. Soft drinks are always taxable in Pennsylvania regardless of the retail environment in which they are sold. A grocery store must separately track and tax its soft drink sales.

The guide on sales and use tax and the role of origin and destination covers how the shipping origin and delivery location affect tax applicability in Pennsylvania and other states, which matters particularly for businesses selling digitally across state lines.

How to Classify a Product Under Pennsylvania Sales Tax Rules

Pennsylvania Sales Tax Audits: What Businesses Risk When Classification Is Wrong

Pennsylvania's Department of Revenue audits businesses to verify that sales tax was properly collected and remitted. The general statute of limitations is three years, extending to the full lookback period if no return was filed or if fraud is involved. For 2025 and 2026, unpaid tax accrues interest at 7 percent annually, compounding daily.

The cost of a classification error is not just the back tax. It is the back tax plus interest plus penalties, applied across every transaction in the audit period where the same error was made. A business that has been misclassifying prepared food as exempt grocery items for three years faces a liability on every affected transaction.

The classification errors described above are not hypothetical. They are the findings that appear in Pennsylvania Department of Revenue audits regularly, because they reflect decisions that are genuinely ambiguous at the point of sale and easy to get wrong without a systematic approach to classification.

The guide on AI-driven sales tax verification strategy covers how automating the classification decision reduces this risk and what an AI-based approach to tax verification looks like in practice.

How Hyperbots Automates Pennsylvania Sales Tax Compliance

Pennsylvania's classification rules are specific enough that applying them consistently at volume is genuinely difficult without a system built for it. A business handling hundreds of vendor invoices a month, each potentially involving prepared food, digital products, clothing subcategories, or multi-jurisdiction rates, cannot rely on a person correctly recalling every rule for every transaction.

Hyperbots' Sales Tax Verification Co-Pilot is built specifically for this problem. It sits on top of the AP process and validates tax treatment at the line-item level on every invoice, before anything is posted to the ERP.

Tax category classification uses AI to classify each line item on a vendor invoice automatically, applying the correct taxable or exempt treatment based on product type, transaction context, and jurisdiction. For Pennsylvania transactions, this means the clothing exemptions, the prepared food rules, and the digital product classifications are applied consistently at every line item without relying on a person to remember each rule.

Tax mismatch identification and reporting flags invoices where the tax charged does not match what Pennsylvania requires, catching overpayments and underpayments before they are posted. A prepared food invoice incorrectly coded as exempt, a digital product invoice where no tax was charged, or a soft drink purchase where the exemption was incorrectly applied: all of these surface as exceptions before they become a liability.

Audit trails for sales tax verification maintain a complete record of every tax classification decision, the rule applied, and the outcome. When the Department of Revenue requests documentation, the business has a structured, timestamped record of every verification decision rather than a manual reconstruction from invoices and spreadsheets.

Go-live is within one month. For a detailed look at how Hyperbots specifically reduces tax risk in AP operations, the guide on fixing tax risk with the Hyperbots Sales Tax Verification Co-Pilot covers the validation logic, exception handling, and compliance outcomes in detail.

See it in action with a demo or start your free trial today.

Conclusion

Pennsylvania's sales tax system rewards businesses that understand its specific exemptions and penalises those that apply general assumptions. Clothing is largely exempt but not entirely. Food is largely exempt but prepared food is not. Digital products are taxable in full. The distinctions are clear once they are known, but they are not always obvious, and the cost of getting them wrong accumulates across every affected transaction until an auditor finds them.

Getting classification right consistently requires either deep familiarity with the rules for every product category sold, or a system that applies those rules automatically and flags the exceptions. The former is difficult to maintain as product ranges grow. The latter is what AI-based tax verification delivers.