How Businesses Stay Updated with New Jersey Sales Tax Changes

Staying updated with New Jersey sales tax changes can quickly become difficult for businesses managing multiple products, jurisdictions, exemptions, and filing requirements. Rules change frequently, digital products continue to create classification confusion, and missing even a small update can lead to penalties, audits, or incorrect tax collection.

The challenge is that most finance teams do not have the time to manually track every regulatory update, monitor rate changes, and validate whether new rules affect their transactions. As businesses grow, keeping sales and use tax compliance accurate becomes less about knowing the rules once and more about staying continuously updated as they evolve.

This blog is for finance managers, AP leads, controllers, and CFOs operating in or selling into New Jersey who want a practical way to stay compliant without building a manual tax tracking operation. It explains how businesses monitor tax changes, where compliance mistakes usually happen, and the systems and processes that help teams stay ahead of evolving regulations.

Why Staying Current with New Jersey Tax Rules Is an Operational Problem

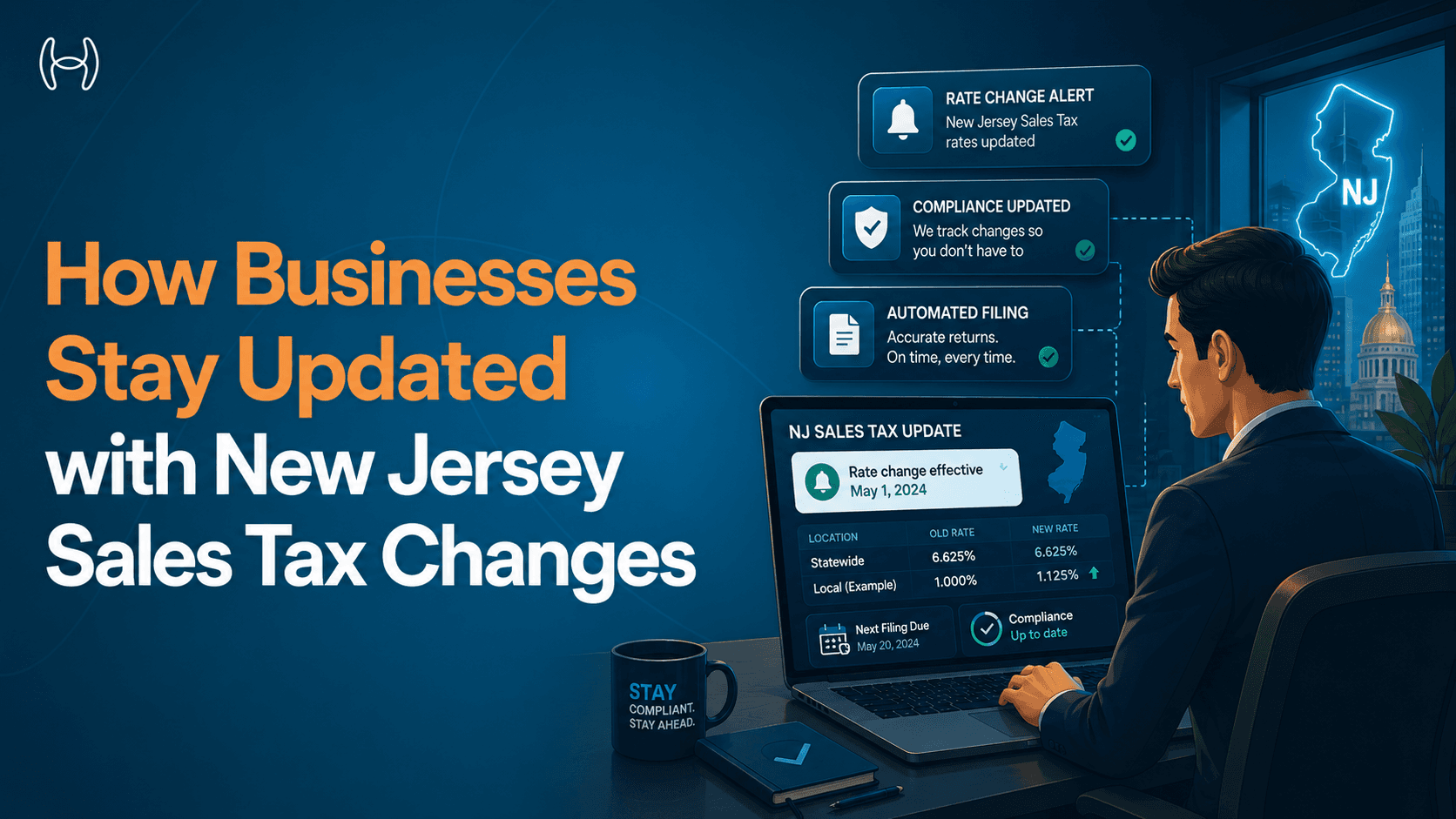

Most finance teams know what New Jersey's sales tax rate is today. The harder question is whether they will know the moment it changes, or the moment a product category their vendors supply moves from exempt to taxable.

New Jersey's 6.625% statewide sales tax has been stable since 2018. That stability can create a false sense of security. The rate itself rarely changes, but the rules around it do. Exemption classifications shift. Economic nexus thresholds are enforced more strictly following the 2018 Wayfair ruling. Urban Enterprise Zone provisions are updated. Digital products and cloud services have added new layers of complexity that did not exist a decade ago. Each of these changes has direct implications for how invoices from vendors should be validated before they are approved for payment.

For a business processing hundreds or thousands of invoices per month, missing a single rule change is not just a compliance risk. It is a financial risk. Overpaying tax because an exemption was missed, or underpaying because a newly taxable service was not caught, can result in either direct cost leakage or audit penalties that dwarf the original tax amount.

How New Jersey Sales Tax Actually Works

Before addressing how to stay updated, it helps to be clear on the structure of New Jersey's tax rules, because the update problem is directly tied to that structure.

New Jersey imposes a 6.625% sales tax on most tangible personal property sold at retail within the state. The rate is uniform across most of the state, though certain Urban Enterprise Zones and special economic areas carry adjusted rules. Use tax, which applies to goods purchased outside New Jersey and brought in for use within the state, mirrors the sales tax rate.

The complexity is not in the headline rate. It is in what is taxable and what is not, and how that boundary shifts over time.

Items that are taxable include electronics, furniture, clothing priced over $110 per item, and certain repair and maintenance services. Plumbing repair, for example, is taxable in New Jersey.

Items that are exempt include most grocery food, prescription drugs, most medical devices, and labor on new construction.

The grey area includes digital products, software-as-a-service, certain professional services, and industry-specific exemptions for sectors like manufacturing and nonprofit organizations.

It is the grey area that generates the most compliance risk, and it is the grey area that changes most often.

How Frequently Do New Jersey Tax Rules Change?

The headline rate changes rarely. The underlying rules change more often than most finance teams track. Here is a realistic picture of the types of updates that occur and how often they tend to appear:

Type of Change | Frequency | Example |

Statewide rate adjustment | Very rare (last change: 2018) | Rate moved to 6.625% |

Exemption category updates | Annually or with budget legislation | Changes to digital goods taxability |

Economic nexus threshold enforcement | Ongoing | Remote seller thresholds under Wayfair |

Urban Enterprise Zone rules | Periodically | Zone boundary changes, expiry of incentives |

Court decisions affecting taxability | Unpredictable | New rulings on specific product categories |

Regulatory guidance from Division of Taxation | Quarterly to annually | New bulletins on cloud services, SaaS |

The practical implication: a business that reviews its New Jersey tax posture once a year is likely operating on rules that are at least partially outdated.

Where Tax Updates Come From and Why Manual Tracking Fails

Finance teams typically rely on one or more of the following sources to stay current:

New Jersey Division of Taxation website is the authoritative source. It publishes tax bulletins, rate tables, updated guidance on exemptions, and notices about rule changes. The information is accurate and comprehensive. The challenge is that it requires someone to actively check it, understand how updates apply to the business's specific vendor and product mix, and translate that into updated AP controls.

Legal and accounting advisors provide reliable interpretation, particularly for complex or ambiguous rule changes. However, they are reactive rather than proactive, and relying on them for routine monitoring adds cost.

ERP configuration updates are how most finance teams try to operationalize rule changes once they are aware of them. A GL code gets a new tax flag. A vendor category is reclassified. But ERP updates require manual input, and they depend entirely on the finance team having caught the rule change in the first place.

Industry associations and tax newsletters provide useful context but are not designed to trigger immediate action.

The fundamental problem with all of these sources is that they place the burden of vigilance on the finance team. Someone has to be watching, interpreting, and acting. When that person changes jobs, when the team is understaffed at month end, or when a rule change is buried in a 40-page legislative document, the process breaks down.

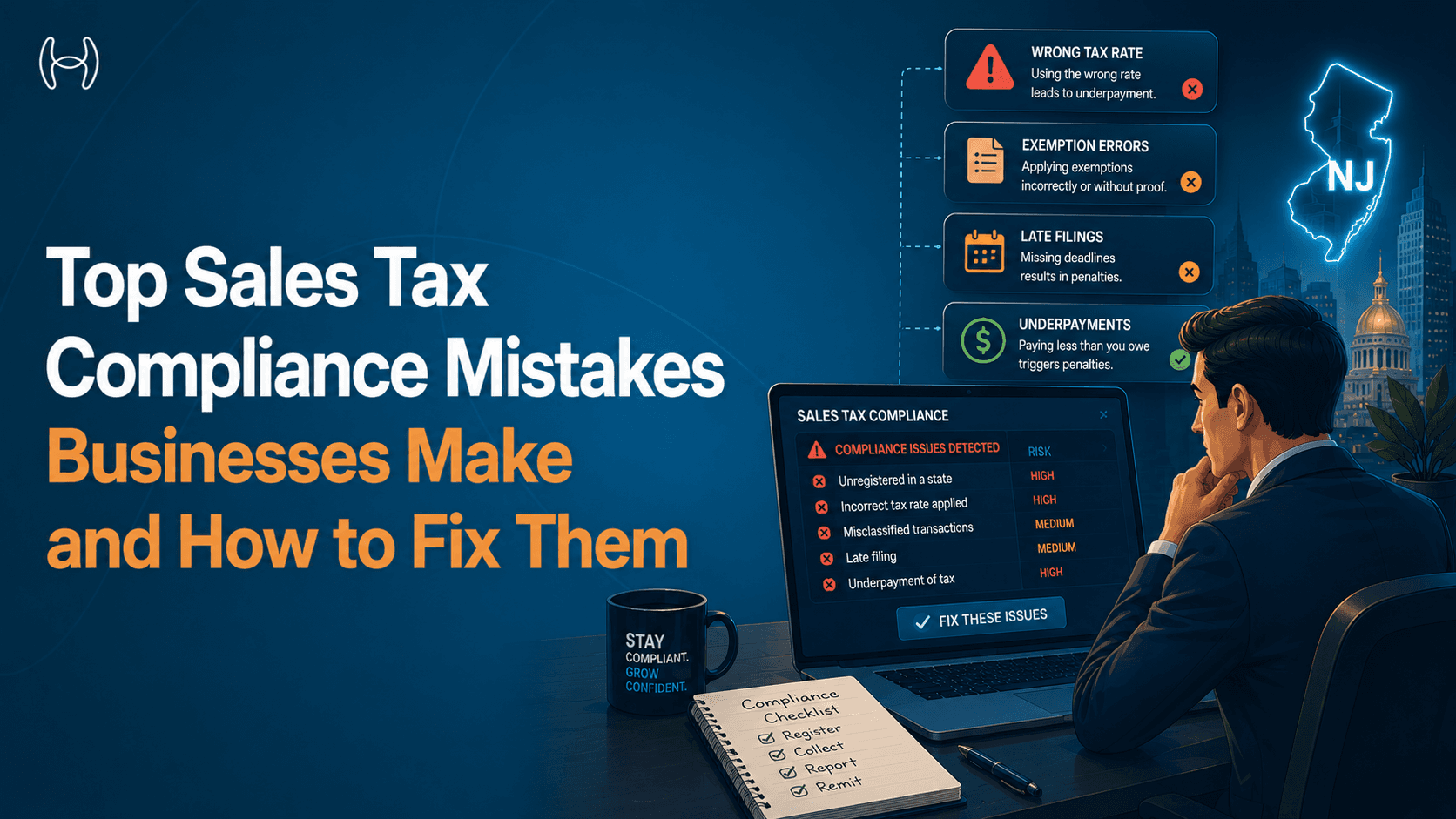

The Real Cost of Missing a Tax Update

The risk is not abstract. When a business misses a New Jersey sales tax update, it typically manifests in one of three ways:

Overpayment occurs when a vendor charges tax on something that is now exempt, and the AP team approves it without catching the error. The overpayment either sits unrecovered or requires a vendor dispute process that takes time and creates friction in the relationship.

Underpayment occurs when an item that is now taxable is processed without tax. The liability accrues on the buyer's side as a use tax obligation. If this is discovered in an audit, the resulting penalty and interest often exceeds the original tax amount.

Audit exposure is the longer-term consequence of both patterns. New Jersey's Division of Taxation can audit businesses for up to four years of prior filings. Systematic errors in tax treatment, even if individually small, aggregate into material audit findings.

The Process a Business Needs to Stay Compliant

Staying updated with New Jersey sales tax changes is not a one-time activity. It requires a repeating process with clear ownership and reliable execution. The flowchart below shows what that process looks like when it is designed properly:

New Jersey Division of Taxation publishes update

|

v

Update captured (automated monitoring or manual review)

|

v

Update interpreted: does it affect the business's vendor/product mix?

|

Yes | No

|

v

AP controls updated: ERP tax flags, vendor classifications, matching rules

|

v

Invoice validation reflects new rules at the point of processing

|

v

Mismatches flagged before payment is approved

|

v

Audit trail maintained for every tax decision

Most businesses have some version of this process. The gaps are almost always in the first two steps: capturing updates systematically and interpreting them quickly enough to act before the next batch of invoices arrives.

Where Current Technology Falls Short

ERP systems are built to record transactions accurately. They are not built to monitor external regulatory changes and update themselves. The tax logic in a standard ERP configuration reflects the rules as they were when the system was last configured, not the rules as they are today.

The practical result is that the accuracy of ERP-based tax processing degrades over time unless someone is continuously maintaining the tax configuration. For a business with multiple vendors supplying different product categories across multiple jurisdictions, that maintenance burden becomes significant.

Standard OCR-based invoice processing compounds the problem. It can capture the tax amount a vendor has charged. It cannot evaluate whether that amount is correct under current New Jersey rules. The validation step requires judgment, and judgment requires current knowledge of the rules.

How AI Changes the Equation for Sales Tax Compliance

AI-driven finance tools approach the tax update problem differently from traditional ERP configuration. Rather than relying on a human to catch a rule change and manually update the system, an AI platform built for finance applies current tax rules at the point of invoice processing without requiring a configuration update for every regulatory change. The difference is that the AI is trained on finance-specific tax logic and integrates directly with live tax dictionaries, so the rules it applies are current by design, not by manual maintenance.

The relevant capability here is not just extraction accuracy. It is the combination of live tax rule application and intelligent exception flagging that allows finance teams to catch mismatches before they become overpayments, underpayments, or audit findings.

How Hyperbots Handles New Jersey Sales Tax Compliance

Hyperbots' Sales Tax Verification Co-Pilot is designed specifically for this problem. It does not require a manual configuration update every time a tax rule changes. It reads every invoice line, classifies each item into the correct tax category based on origin and destination jurisdiction, and cross-checks the vendor-charged tax amount against the applicable rate for that specific combination of item, location, and buyer-seller relationship.

For New Jersey specifically, this means the co-pilot handles the jurisdictional complexity described above: Urban Enterprise Zone variations, use tax obligations on out-of-state purchases, exemptions for specific product categories, and the economic nexus rules that apply to remote sellers. Each of these is applied at the line-item level, not at the invoice level, which is where most manual processes fail. When a tax mismatch is detected, it is flagged with the exact detail the AP team needs to act on it before payment is approved.

The co-pilot integrates directly with the Invoice Processing Co-Pilot, which achieves 99.8% accuracy in invoice data extraction and processes 80% of invoices straight through without human intervention. The tax verification step runs within the same workflow, meaning that by the time an invoice reaches the approval queue, the tax has already been validated. The AP team reviews exceptions, not every invoice.

This matters because the cost of manual tax review at scale is significant. Hyperbots delivers an 80% reduction in invoice processing cost, and the elimination of tax-related rework is a meaningful part of that.

The co-pilot maintains a complete, timestamped audit trail for every tax decision. For a business operating in New Jersey with a four-year audit window, that documentation is the difference between a straightforward audit response and an expensive reconstruction exercise. Finance teams that have deployed it have recovered significant tax leakage — see how one CFO eliminated $200,000 in tax leakage using Hyperbots' sales tax verification capabilities.

Go-live takes one month. ROI is typically reached within six months, driven by recovered overpayments, eliminated penalty risk, and reduced AP team time spent on tax-related exception handling.

See it in action with a demo or start your free trial today.

What Good Tax Compliance Looks Like in Practice

The table below compares the typical manual approach to New Jersey sales tax compliance with an AI-driven process:

Compliance Activity | Manual Approach | With Hyperbots AI |

Monitoring for NJ tax rule changes | Periodic manual review of Division of Taxation website | Integrated with live tax dictionaries |

Applying correct rate at invoice processing | Based on ERP configuration at last update | Applied at line-item level per current rules |

Handling Urban Enterprise Zone variations | Manual lookup or missed | Automatically handled by jurisdiction mapping |

Catching vendor overcharges | Rarely identified before payment | Flagged before approval with exact mismatch detail |

Managing use tax on out-of-state purchases | Tracked manually or not at all | Captured within invoice validation workflow |

Audit documentation | Reconstructed from email and ERP logs | Automatically maintained timestamped trail |

Multi-entity compliance | Separate processes per entity | Unified across entities in a single platform |

The Connection to Procurement Controls

Tax compliance does not sit in isolation. It is part of the broader AP and procurement control environment. A business that has weak purchase order and AP controls will typically also have weak tax controls, because the underlying problem is the same: manual processes cannot scale reliably across high invoice volumes. For businesses operating in New Jersey specifically, that gap is compounded by the frequency of rule-level changes that standard procurement controls are not designed to track.

The relationship between purchase order management, accounts payable approval workflows, and tax verification is direct. A three-way match between a purchase order, a goods receipt, and an invoice is only complete if the tax on that invoice has also been verified. Without the tax step, the match is technically complete but financially incomplete.

Finance leaders building out their AP control environment should treat tax verification as a component of invoice processing, not a separate compliance function. The AI invoice processing platforms that deliver the highest straight-through processing rates are the ones that include tax verification within the core processing workflow rather than treating it as an afterthought.

Frequently Asked Questions

How often does New Jersey's sales tax rate actually change?

Rarely. The current rate of 6.625% has been in place since 2018. The more frequent changes involve exemption classifications, new guidance on digital products and services, and enforcement of economic nexus rules for remote sellers. Finance teams should monitor these rule-level changes even when the headline rate is stable.

What is the difference between sales tax and use tax in New Jersey?

Sales tax applies to taxable goods and services sold at retail within New Jersey. Use tax applies to goods purchased outside New Jersey and brought in for use within the state, at the same 6.625% rate. Businesses that purchase from out-of-state vendors and do not pay sales tax at the point of purchase are responsible for self-assessing and remitting use tax.

What is the audit risk for New Jersey sales tax non-compliance?

New Jersey's Division of Taxation can audit businesses for up to four years of prior filings. Systematic errors in tax treatment, even if individually small in dollar terms, can aggregate into material findings. Interest and penalties on understated tax liabilities can exceed the original tax amount.

How does Hyperbots stay current with New Jersey tax rule changes?

Hyperbots' Sales Tax Verification Co-Pilot integrates with live tax dictionaries that are maintained with current jurisdiction-level rules. The co-pilot applies current rules at the point of invoice processing without requiring a manual ERP configuration update each time a rule changes.

How long does it take to go live with Hyperbots?

Implementation is complete within one month. The co-pilot connects to the existing ERP through a pre-built native connector and requires no custom development.

Does Hyperbots handle multi-entity and multi-state tax compliance?

Yes. The co-pilot supports multi-entity environments with separate tax rules, approval workflows, and ERP instances. For businesses operating across multiple states, the jurisdiction mapping handles the different rules that apply in each state.