How to Build a Business Case for ERP: What CFOs Need to Justify the Investment to the Board

The board does not care that your current system cannot handle multi-entity consolidations, or that month-end close takes eleven days, or that your AP team is manually keying invoices into a spreadsheet before anyone has had their morning coffee. What the board cares about is a number: how much does this cost, what does it return, and when does it pay back.

Building a compelling ERP business case is not a technical exercise. It is a financial and strategic argument. Done right, it gives the board the clarity they need to approve the investment with confidence. Done wrong, it gets sent back for "more information" three times and eventually dies in a committee.

This guide covers how to structure that argument, what to include, what to leave out, and how to make the numbers actually hold up under scrutiny.

Why Most ERP Business Cases Fail to Get Approved

The most common reason an ERP business case stalls is not that the project is too expensive. It is that the case is built like a technology proposal rather than a financial one. It leads with features, lists integration requirements, and buries the ROI in a table at the back that nobody reads carefully.

A board is not evaluating whether the ERP has better workflows than the current system. They are evaluating whether this capital allocation beats competing uses of the same money. The business case needs to answer that question directly, in the language of investment returns, payback periods, and risk.

The second most common failure is that costs are underestimated and benefits are overestimated, and both are obvious to anyone who has seen an ERP implementation go sideways before. Boards have long memories. If your organization went through a difficult ERP project five years ago, you are carrying that history into the room whether you acknowledge it or not. A credible business case accounts for risk honestly rather than assuming everything goes to plan.

The third failure is presenting a single scenario. Boards are uncomfortable approving large capital expenditures based on a single set of assumptions. Presenting a base case, a conservative case, and an optimistic case gives the board a range to evaluate rather than a binary decision on one set of numbers.

What the Business Case Structure Should Look Like

A well-structured ERP business case has six sections. The order matters because each section earns the right to the next.

The current state problem quantifies the cost of doing nothing. It is not a list of complaints about the current system. It is a financial argument that the status quo is expensive. Manual processes have a cost per transaction. Slow financial close has a cost in delayed decision-making. Compliance gaps have a cost in audit findings and penalties. Fragmented systems have a cost in the reconciliation work required to produce a single version of the truth.

The proposed solution is a single paragraph describing what is being proposed, what it replaces, and what it does not replace. No feature lists. No vendor marketing language.

The investment required is a complete, fully loaded cost estimate covering software licensing, implementation services, data migration, integration, internal resource time, change management, training, and ongoing support. This is where most cases are undercooked. An incomplete cost estimate that gets corrected later destroys credibility with the board faster than almost anything else.

The benefits case is a quantified, defensible estimate of the financial benefits the investment produces, organized by category and mapped to the cost items in the current state section. Each benefit line needs a clear methodology behind it, not a percentage improvement sourced from a vendor's marketing materials.

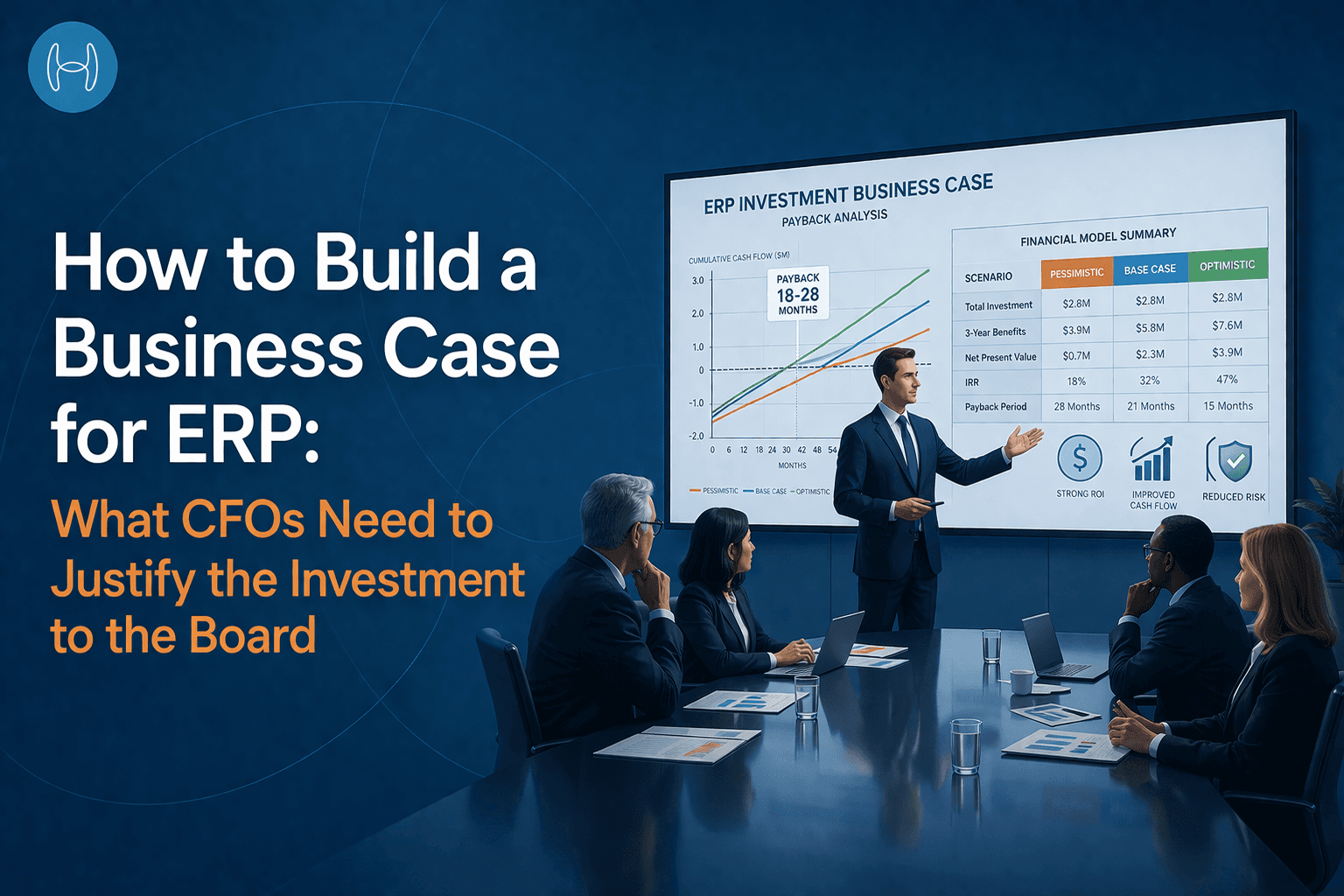

The ROI and payback analysis is a three to five year financial model showing net cash flows, cumulative returns, payback period, and net present value. This is the section the board actually scrutinizes. It should include sensitivity analysis showing how returns change under different assumptions.

The risk assessment is an honest account of what can go wrong, how likely it is, and what mitigation is in place. A business case that does not identify risks looks naive. One that identifies them and addresses them looks disciplined. The CFO toolkit for adopting AI includes practical risk and evaluation frameworks that translate directly into this section of the ERP business case.

Building the Cost Side: What Gets Left Out and Why It Comes Back to Haunt You

The total cost of an ERP investment has five components, and most business cases only budget properly for two of them.

Software licensing is the line item everyone starts with. For cloud ERP platforms, this is typically a per-user monthly subscription differentiated by license type. Getting this right requires knowing your actual user count by role, not just current headcount. Organizations consistently undercount users in the initial estimate because they forget occasional users: warehouse staff who need read access, regional managers who approve purchase orders once a month, auditors who need view-only access during year-end.

Implementation services is where the largest variance typically sits. Mid-market ERP implementations for organizations with moderate complexity generally fall between $50,000 and $200,000 in services cost, depending on scope, data complexity, the number of integrations required, and whether the implementation partner is working from a pre-configured template or building from scratch. The single most reliable predictor of implementation cost overrun is the quality of the data being migrated. Bad master data takes time to clean, and that time is billed.

Internal resource cost is the line item that disappears from most business cases because it does not appear on an invoice. But the finance team members who spend six months on the implementation project have a cost. Their time has to come from somewhere, and either other work goes undone or backfill is required. A credible business case accounts for this explicitly.

Integration costs are underestimated almost universally. Every connection between the ERP and another system, whether that is a banking portal, a payroll system, a logistics platform, or a tax engine, requires scoping, development, testing, and ongoing maintenance. Organizations with mature technology stacks tend to have more integrations than they realize until someone maps them all.

Ongoing run costs include annual software maintenance or subscription increases, support contracts, system administration, and the ongoing cost of enhancements and upgrades. For a three to five year model, these need to be included explicitly. A business case that shows a sharp payback but does not account for year three support costs will not survive board scrutiny.

Building the Benefits Case: How to Quantify What Matters

Benefits in an ERP business case fall into three categories: hard savings, soft savings, and strategic value. Boards respond to hard savings. They are skeptical of soft savings. They discount strategic value unless it is tied to a specific financial outcome.

Hard Savings

Hard savings are reductions in costs that currently exist and will not exist after the ERP is implemented. They are the easiest to defend because they are tied to something currently being paid. A framework for measuring ROI from AI-led automation in finance is useful here: it provides the cost reduction metrics and productivity benchmarks that give each hard saving line a defensible methodology.

Process cost reduction is the most common hard saving in an ERP case. Manual processes that can be automated have a measurable cost today: headcount, overtime, error correction, and the management time spent chasing exceptions. The methodology is straightforward. Identify the process. Measure the current time spent on it. Multiply by the fully loaded cost of the people doing it. Apply a realistic automation rate. The automation rate is where finance leaders need to be conservative. A vendor claiming 90% automation may be accurate in their best-case customer, but a credible business case uses numbers the finance team is comfortable defending if the project underperforms.

System consolidation savings apply when the ERP replaces multiple point solutions currently being paid for separately. Licenses for standalone AP tools, procurement software, expense management platforms, and reporting tools that become redundant after implementation are genuine hard savings. Map every system being replaced and calculate the annual cost of each.

Audit and compliance cost reduction applies where the current environment generates significant manual work to produce audit evidence, reconcile records, or maintain compliance documentation. An ERP with strong audit trails and built-in controls reduces this cost measurably.

Soft Savings

Soft savings are real but harder to convert to a definitive dollar figure. They include faster decision-making from better data, reduced management time on exception handling, and improved finance team experience leading to lower turnover. Include them but label them clearly as soft. Do not use them as the primary financial justification for the investment.

Strategic Value

Strategic value covers the capabilities the organization does not currently have: the ability to support a new entity without a proportional increase in finance headcount, the ability to close the books in three days rather than ten, the ability to scale operations without scaling the back-office cost structure. These are real, but they need to be tied to a specific strategic objective the board already cares about, not presented as abstract future benefits.

The ROI Model: What the Numbers Need to Show

Year | Investment | Benefits | Net Cash Flow | Cumulative |

Year 0 | Full implementation cost | None | Negative | Negative |

Year 1 | Ongoing run cost | Partial year benefit (6 to 9 months post go-live) | Small negative or breakeven | Negative |

Year 2 | Ongoing run cost | Full year benefit | Positive | Approaching breakeven |

Year 3 | Ongoing run cost | Full year benefit | Positive | Positive cumulative ROI |

Years 4 and 5 | Ongoing run cost | Full year benefit | Positive | Strong cumulative return |

The payback period for a well-scoped mid-market ERP implementation with realistic benefit assumptions typically falls between 18 and 36 months from go-live. If the model shows payback in under 12 months, the benefits are probably overstated. If it shows payback beyond 48 months, either the implementation costs are higher than they should be or the benefits case needs more work.

Present this model in three scenarios. The base case uses the most likely assumptions. The conservative case applies a 20 to 30 percent reduction in benefits and a 20 percent increase in costs. The optimistic case uses the full benefit estimates with a smooth implementation. Most boards make their decision based on whether the conservative case is acceptable, which is the right frame for the conversation.

The Process Flow: From Business Case to Value Realization

The following is the end-to-end sequence from business case development through board approval to benefit realization. This should be rendered as a swimlane diagram with three lanes: CFO and Finance Team, Board and Executive Stakeholders, and Implementation Team.

Step 1: Current state assessment. Finance team quantifies the cost of the status quo across process cost, system cost, compliance cost, and strategic constraints. Output is a defensible baseline.

Step 2: Solution scoping. Finance team works with IT and the selected implementation partner to define scope, user count, integration requirements, and implementation approach. Output is a fully loaded cost estimate with a stated confidence range.

Step 3: Benefits modeling. Finance team builds the benefits case by process area, applies conservative automation rates, and maps benefits to the current state cost baseline. Output is a three-scenario ROI model with payback and NPV calculations.

Step 4: Risk assessment. Finance team documents implementation, benefit realization, disruption, and change risks with specific mitigations. Output is a risk register with owners and monitoring cadence.

Step 5: Board presentation. CFO presents the business case. The board reviews the conservative scenario, stress-tests the assumptions, and approves, requests modifications, or requests additional information.

Step 6: Implementation governance. Implementation team executes against the approved scope. Finance team monitors against the benefit realization plan quarterly. Variance from plan is reported to the board at regular intervals.

Step 7: Post-go-live value tracking. Finance team measures realized benefits against the business case assumptions. Results are reported to the board as part of the investment closure review.

How AI Automation Compresses the ERP Payback Period

One section of the ERP business case that most CFOs underuse is the opportunity to accelerate the return by layering AI automation onto the ERP from day one, rather than treating it as a future phase.

The logic is straightforward. An ERP investment produces most of its hard savings by consolidating systems and standardizing processes. But ERP systems do not, by themselves, automate the work within those processes. Invoice processing still requires human review. Purchase orders still require manual creation in most cases. Month-end accruals still require a finance analyst to identify unbilled liabilities and book them by hand. The ERP records these transactions more cleanly than the legacy system did, but the labor cost of executing them does not fall dramatically from ERP implementation alone.

How AI complements ERP systems is well understood: the ERP is the system of record, and AI automation sits on top to handle the execution layer that ERP platforms are not designed to manage autonomously. In a board business case, this matters because including the automation layer changes the payback calculation materially. An ERP implementation that achieves a 30-month payback on its own achieves a shorter payback when finance automation is included, because the automation benefits begin delivering from go-live rather than from a future phase that may or may not happen on schedule.

The AI advantage in finance is not theoretical at this point. Finance teams across mid-market organizations are using AI co-pilots to automate the operational layer of finance that ERP systems record but do not execute.

Hyperbots is one example of this automation layer. It connects to ERP platforms through native integrations and deploys AI co-pilots for invoice processing, procurement, accruals, payments, vendor management, and sales tax verification. Relevant to a payback model: invoice processing costs can be reduced by up to 80%, up to 80% of invoices can achieve straight-through processing without human intervention, PO creation and dispatch cycle time can be reduced by 80%, and accruals variance can be brought below 5% of actual costs. The co-pilots are pre-trained on finance-specific data, which means they are operational within one month of go-live without requiring a lengthy model training period. ROI from the automation layer is realized within six months of go-live.

For a CFO building the business case, the practical implication is this: when you model the ERP investment alone, you are presenting a partial picture. The operating cost reduction that the board is looking for comes primarily from what the finance function stops doing manually, not from the ERP license itself. Including the automation layer in the investment case, with its own cost line and its own benefit line, produces a more complete and more compelling financial argument.

CFOs who want to understand how peers are approaching this combined investment have found the perspective from finance leaders on agentic AI in practice useful context for framing the conversation internally.

Common Board Objections and How to Address Them

"We tried this before and it went over budget." Acknowledge the history directly. Present the specific reasons the previous project overran and explain the structural differences in this proposal: fixed-fee implementation, phased go-live, data quality assessment completed upfront, and a governance model that monitors the business case through to completion rather than closing the file at go-live.

"The benefits look optimistic." Walk the board through the conservative scenario line by line. Show the methodology behind each benefit estimate: the current process cost, the automation rate applied, and the resulting saving. A benefit that cannot be explained in two sentences should not be in the business case.

"Can we do this in phases?" Yes, and phasing is often the right approach. Present a phased option with a smaller initial investment, a faster first-phase payback, and a clear decision point before committing to subsequent phases. A phased approach also reduces implementation risk directly.

"What happens if we do nothing?" This is the question that often gets asked last but deserves to be answered first. The cost of the status quo is not zero. Quantify it: the ongoing labor cost of manual processes that automation would eliminate, the compliance risk of running on a system that cannot support future reporting requirements, and the competitive cost of a finance function that cannot close fast enough to support the business decisions that need to be made.

What the Executive Summary Should Look Like

The one-page summary that goes to the board before the detailed presentation should answer four questions: What is the problem? What are we proposing? What does it cost? What does it return and when?

Current state cost (annual) | Quantified cost of manual processes, system redundancy, compliance work |

Proposed investment (total, 3 years) | Software, implementation, integration, internal resource, ongoing costs |

Expected annual benefit (steady state) | Hard savings by category, conservatively estimated |

Payback period (conservative case) | Months from go-live to cumulative breakeven |

Net present value (3 years, conservative) | Discounted net benefit at the organization's cost of capital |

Primary risk and mitigation | Single biggest risk and the specific mitigation in place |

This format forces discipline on the numbers and gives the board exactly what it needs to make a decision without reading a 40-page document before they are ready to engage with it.

Frequently Asked Questions

How long should an ERP business case take to build?

Four to eight weeks done properly. The current state cost assessment requires data gathering from finance, procurement, and operations. The implementation cost estimate requires scoping conversations with at least two implementation partners. The benefits model requires input from process owners across the business. Rushing any of these steps produces a business case that falls apart under scrutiny.

Should the CFO or IT lead the business case?

The CFO should lead it. ERP is a financial and operational investment, not a technology project. The CFO owns the numbers and is the most credible voice in front of the board on the financial argument. IT is a critical input on technical scope and cost, but the business case lives in finance.

What discount rate should be used for the NPV calculation?

Use the organization's weighted average cost of capital if known. If not, 8 to 12 percent is a reasonable range for most mid-market organizations. The choice of discount rate matters less than consistency: use the same rate for all scenarios and state it explicitly so the board can adjust it if they have a different view.

How do you handle benefits that are difficult to quantify?

Include them as a qualitative appendix, not as a number in the model. A benefit that cannot be quantified credibly should not be used to make the financial case add up. If the case only works with unquantifiable strategic benefits, the quantifiable case is not strong enough and the project scope or cost structure needs to be revisited.

What is the most common reason ERP business cases get rejected?

Incomplete cost estimates and benefit assumptions that cannot be defended under questioning. Both are avoidable. Get to a complete cost estimate before building the benefits model. Build the benefits model from process data, not vendor benchmarks. Present the conservative scenario as the primary case, not the optimistic one.

For a detailed breakdown of what ERP systems actually cost across major platforms, including licensing models, implementation ranges, and total cost of ownership guidance that feeds directly into the investment model described here, the ERP pricing comparison guide is the right starting point.