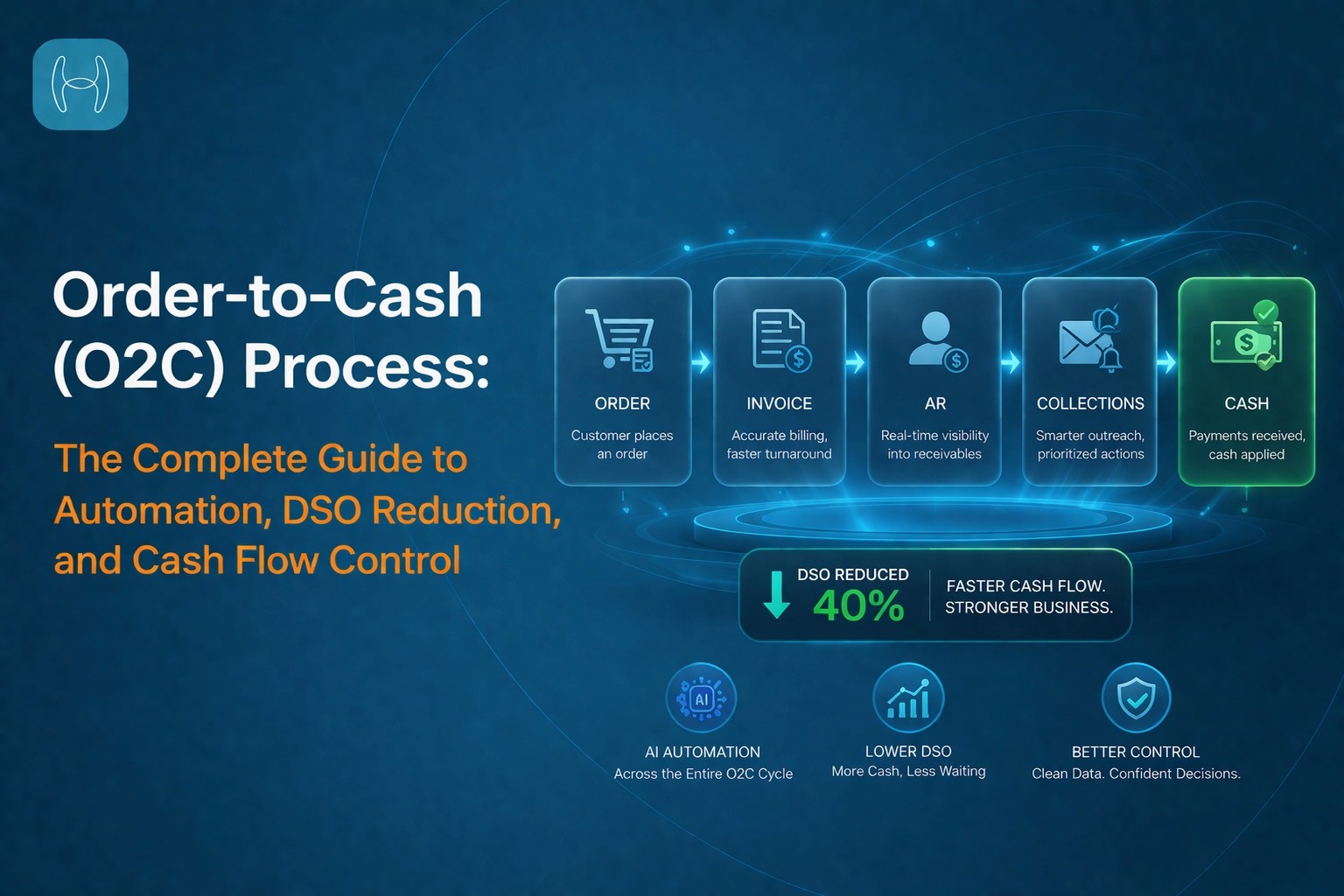

Order-to-Cash (O2C) Process: The Complete Guide to Automation, DSO Reduction, and Cash Flow Control

Your Order-to-Cash process is costing you more than you think, and the damage is invisible until it isn't.

By the time a CFO sees DSO creeping upward, unapplied cash piling up, or the collections team working harder with diminishing returns, the process has already been leaking for months. The root cause is almost never a people problem. It is a process problem, and more specifically, it is an automation gap that sits across every stage of the O2C cycle.

This guide breaks down what the Order-to-Cash process actually involves at each stage, who owns each step, where the failures typically occur, what they cost, and how AI automation changes the outcome at every point in the cycle.

Order-to-Cash at a Glance

The Order-to-Cash process begins when a customer places an order and ends when payment is received, matched, and posted to the general ledger.

The eight stages in a complete O2C cycle are: order management, credit assessment, order fulfillment, shipping or delivery, customer invoicing, accounts receivable management, payment collections, and reporting.

The most common failure points are invoice errors that trigger disputes, aging-bucket-driven collections that miss the accounts that actually need attention, and cash application backlogs that distort the true AR position.

AI automation applied across the full O2C cycle reduces DSO by up to 40%, cuts collections cost by up to 70%, and eliminates up to 90% of unapplied cash.

What Is Order-to-Cash?

Order-to-Cash (O2C) is the end-to-end business process that covers everything from the moment a customer places an order to the moment payment for that order is received, verified, and recorded in the financial system.

It is not just a finance process. O2C spans sales, operations, logistics, and finance, which is exactly why it breaks down so often. When handoffs between teams are manual, data gets lost, invoices go out late or wrong, collections outreach is mistimed, and cash sits unmatched in the AR ledger for days after it arrives.

Why Optimizing O2C Matters

Most finance leaders think about O2C as a collections problem. It is actually a working capital problem that happens to manifest in collections. Every stage of the O2C cycle either accelerates or delays the point at which revenue becomes cash. A company running 60-day DSO on $50 million in annual revenue has roughly $8 million tied up in receivables at any given time. Bringing that down by 20 days releases approximately $2.7 million in liquidity without touching the revenue line.

Beyond liquidity, O2C performance affects billing accuracy, customer relationships, audit readiness, and the credibility of the AR aging report as a management tool. A process that produces a clean, current ledger is one a CFO can actually make decisions from.

O2C vs. Procure-to-Pay: What Is the Difference?

The two processes finance leaders most often conflate are Order-to-Cash and Procure-to-Pay. They are not the same, and optimizing one without the other only fixes half the working capital equation.

Process | Starting Point | Primary Focus | Teams Involved | Cash Direction | Goal |

Order-to-Cash (O2C) | Customer places an order | Revenue collection and AR management | Sales, operations, AR, finance | Incoming | Collect payment quickly and accurately after a sale |

Procure-to-Pay (P2P) | Internal need identified | Supplier management and cost control | Procurement, AP, finance | Outgoing | Pay suppliers accurately and on time |

O2C manages incoming cash from customers. P2P manages outgoing cash to vendors. They are mirror images of each other, and the gap between them is where working capital either accumulates or drains. Optimizing both together is what actually moves the needle on cash position.

The Eight Stages of the Order-to-Cash Process

1. Order Management

Owned by: Finance operations and sales teams

Order management is where the O2C cycle begins. A customer submits a purchase order, through email, an online portal, EDI, or direct sales confirmation, and that order needs to be captured, validated, and routed for fulfillment before anything else can happen.

In organizations still running this manually, an order can sit in someone's inbox for hours before it is touched. The data then gets keyed into the ERP by hand, which introduces errors that will only surface three stages later when the customer disputes the invoice.

Key responsibilities at this stage:

Validate order details against contract terms, pricing agreements, and available inventory

Route the order to the appropriate fulfillment team

Confirm that invoicing setup reflects the customer's agreed commercial terms

Flag and resolve discrepancies before the order moves forward

When order data is accurate at this stage, every downstream stage becomes faster and cleaner. When it is not, the errors compound.

2. Credit Assessment

Owned by: Credit and collections team

Credit assessment determines whether a customer should be extended credit terms before goods or services are delivered. For new customers, this means running a credit check against financial history and setting an appropriate credit limit. For existing customers, it means checking whether their current outstanding balance and recent payment behavior warrant fulfilling a new order on the same terms.

Most ERP systems enforce a hard credit limit but cannot assess behavioral risk. A customer who has paid consistently for two years but has suddenly gone quiet on three invoices is a different risk profile than one who always pays on day 58 of a 60-day term, but a static credit limit treats them the same way.

Key responsibilities at this stage:

Run credit checks on new customers

Review payment behavior trends for existing customers

Set or adjust credit limits based on current financial profile

Approve, modify, or flag orders that exceed credit thresholds

3. Order Fulfillment

Owned by: Operations and supply chain teams, tracked by finance

Order fulfillment is the operational stage: preparing goods for delivery, activating a software subscription, scheduling a service, or deploying a solution. Finance does not own this stage, but it has a direct stake in how quickly it moves. The invoice clock does not start until delivery is confirmed, so every delay in fulfillment is a delay in the O2C cycle.

Key responsibilities at this stage:

Confirm inventory availability or service readiness

Coordinate delivery timelines with logistics

Track fulfillment costs for accurate recording

Notify the invoicing team when delivery is confirmed

4. Shipping and Delivery

Owned by: Logistics team, monitored by finance

For product businesses, this is the physical movement of goods to the customer. For SaaS or services businesses, it is account activation, credential delivery, data migration, or go-live confirmation. Either way, it marks the point at which the performance obligation is satisfied and the invoice can be generated.

Finance monitors this stage for cost tracking and to ensure the invoicing trigger is not missed. In manual environments, the notification that delivery is complete sometimes never makes it to the AR team, resulting in invoices that go out days late or not at all.

5. Customer Invoicing

Owned by: Accounts receivable team

This is where most O2C processes first visibly break down. The invoice has to reflect exactly what was ordered, at the price agreed in the contract, with the correct PO reference, the right tax treatment, and the customer's specific billing requirements. An invoice that gets any of these wrong does not get paid. It gets disputed, and a disputed invoice can sit unresolved for weeks.

Key responsibilities at this stage:

Generate invoices accurately from order and fulfillment data

Apply the correct payment terms for each customer

Validate GL coding, PO references, and tax treatment before sending

Send invoices promptly after delivery confirmation

The shift that AI makes at this stage is moving validation before dispatch rather than after. Errors caught before the invoice reaches the customer do not become disputes. Errors caught by the customer do.

6. Accounts Receivable Management

Owned by: AR team

Once the invoice is sent, AR management takes over. This stage is about monitoring which invoices are outstanding, tracking which ones are approaching due dates, and managing the relationship with customers throughout the payment cycle.

A common failure here is treating all outstanding invoices the same way. An invoice at 30 days from a customer who always pays at 45 does not need the same outreach as an invoice at 30 days from a customer who has disputed two of the last five invoices. Managing AR by aging bucket rather than by account intelligence wastes effort and misses the accounts that actually need attention.

Key responsibilities at this stage:

Monitor open invoice status across the customer portfolio

Track payment behavior patterns by customer

Manage payment terms adherence and communicate proactively

Escalate high-risk accounts before they become bad debt situations

7. Payment Collections

Owned by: Collections team

Collections is where the effort of the previous six stages either pays off or does not. The collections team receives and processes incoming payments, reconciles them against open invoices, and resolves discrepancies.

Cash application is the most operationally painful part of this stage. Customers pay in ways that are inconsistent and often non-standard: a single remittance covering 12 invoices, a payment referencing a wrong invoice number, a partial payment against a disputed balance, a deduction taken without documentation. Matching these payments to open invoices without automation is time-consuming, error-prone, and creates the unapplied cash backlog that distorts every downstream report.

Key responsibilities at this stage:

Process incoming payments across ACH, check, wire, and card

Match payments to open invoices using remittance data

Handle deductions, short payments, and disputed amounts

Post matched payments to the ERP

8. Reporting and Data Management

Owned by: Finance analytics and reporting team

The final stage closes the loop. Reporting on O2C performance tells the finance team where the cycle is working and where it is leaking. DSO trends, invoice accuracy rates, collection cycle times, unapplied cash levels, and bad debt ratios are the metrics that show whether optimization efforts are working.

Without real-time reporting, finance leaders are making decisions on data that is days behind the actual state of the AR ledger. That lag is itself a cost: slower response to at-risk accounts, delayed identification of process failures, and AR aging reports that do not reflect reality.

Key responsibilities at this stage:

Generate real-time reports on DSO, collection rates, and invoice status

Identify bottlenecks and failure patterns in the cycle

Use payment behavior data to refine credit and collections strategy

Provide accurate AR aging to support cash flow forecasting

Common Challenges in Running O2C Manually

Stage | Challenge | Financial Impact |

Order management | Manual data entry from customer POs; errors introduced at intake | Data discrepancies cascade into invoice disputes and delayed fulfillment |

Credit assessment | Static credit limits with no behavioral scoring; borderline accounts reviewed manually | Slow credit decisions delay order processing; inconsistent decisions create revenue risk |

Order fulfillment | Finance not notified when delivery is complete; invoice trigger is missed | Invoices sent late; payment clock delayed by days or weeks |

Customer invoicing | GL coding errors, wrong PO references, and incorrect tax treatment sent to customers | Disputed invoices stall payment and restart the collection clock |

AR management | Aging-bucket prioritization with no account intelligence | Collections effort directed at low-risk accounts; high-risk accounts missed |

Payment collections | Manual remittance matching; partial payments and deductions require individual resolution | Large unapplied cash backlog; AR aging reports do not reflect true position |

Cash application | Non-standard remittance formats require manual interpretation | Payments sit unmatched for days, inflating apparent DSO |

Reporting | Reports built from stale ERP data; no real-time visibility | Finance decisions based on AR position that is 3 to 5 days behind reality |

Best Practices for Optimizing the O2C Cycle

Standardize and document every handoff

The stages of O2C cross multiple teams, and every handoff is a point where data can be lost or delayed. Document the exact output each stage produces and the exact input the next stage requires. Review these handoffs quarterly and update them when business processes change. Most O2C failures are not technology failures. They are handoff failures.

Integrate systems so data flows without re-entry

ERP systems, CRM platforms, and collections tools need to share data in real time, not through batch syncs or manual exports. An order closed in the CRM should appear in the ERP without anyone keying it. A payment received in the bank should update the AR ledger without anyone matching it. Every manual re-entry step is a delay and an error opportunity.

Apply automation where volume creates inconsistency

The stages of O2C that are most painful to run manually are the ones with the highest transaction volume and the most format variability: invoice validation, cash application, and collections outreach. These are also the stages where automation delivers the most immediate ROI, because the improvement is consistent across every transaction rather than dependent on which team member happens to be working that day.

Track the metrics that actually indicate process health

DSO is the headline metric, but it does not tell you where the problem is. Track invoice accuracy rates to find the invoicing stage failures. Track collection cycle time by account segment to find the collections prioritization failures. Track unapplied cash as a percentage of total receipts to find the cash application failures. Each metric points to a specific stage in the process where intervention will move the needle.

Prioritize collections by account intelligence, not aging buckets

The single highest-leverage change most AR teams can make is moving from aging-bucket-driven outreach to intent-based prioritization. Not every account in the 45-day bucket is equally at risk, and not every account in the 60-day bucket needs a phone call. Scoring accounts based on payment history, dispute frequency, communication patterns, and invoice value produces a collections queue where effort is directed at the accounts that actually need it.

Key Metrics for O2C Performance

Days Sales Outstanding (DSO)

DSO measures the average number of days between invoice issuance and payment receipt. It is the single most widely used indicator of O2C health.

High DSO is almost always caused by a combination of factors: late invoicing, invoice disputes, ineffective collections, and cash application delays. Addressing one without the others produces limited improvement.

How to improve it: Automate invoice validation to prevent disputes before they occur. Apply intent-based scoring to collections outreach. Automate cash application to ensure payments are posted immediately upon receipt.

Invoice Accuracy Rate

Invoice accuracy measures the percentage of invoices sent without errors that require correction or generate a dispute. This is the upstream metric that drives DSO. An invoice dispute does not just delay payment from that customer. It consumes AR team time, occupies collections capacity, and often delays payment from other customers who are also waiting for the AR team's attention.

How to improve it: Validate GL coding, PO references, tax treatment, and billing address automatically before invoices are dispatched. Catch errors before the customer sees them rather than after.

Unapplied Cash as a Percentage of Total Receipts

Unapplied cash measures the volume of payments received but not yet matched to open invoices. High unapplied cash inflates apparent DSO, distorts AR aging reports, and makes it impossible to know the true outstanding receivables position.

How to improve it: Automate remittance reading and invoice matching. AI can handle non-standard remittance formats, partial payments, and deduction codes that rule-based systems cannot process without human intervention.

Collections Cost as a Percentage of Revenue Collected

This metric captures how much it costs to collect each dollar of revenue. High collections cost relative to revenue usually indicates that the collections team is spending time on accounts that would have paid without intervention, rather than on accounts that genuinely need attention.

How to improve it: Apply intent-based account scoring to direct outreach effort where it has the highest probability of improving the outcome. Automate outreach for low-risk accounts and reserve human effort for high-risk and high-value situations.

Cash Conversion Cycle (CCC)

CCC measures the number of days between investing in operations and receiving cash from customers. For O2C purposes, the relevant component is the receivables side: how quickly a sale becomes cash in the bank.

How to improve it: Compress each stage of the O2C cycle. Faster order processing, accurate invoicing, smarter collections, and immediate cash application all reduce the receivables component of CCC.

The O2C Automation Process Flow

The following is the end-to-end automated O2C workflow from order receipt through to cash posted in the ERP. This should be rendered as a swimlane diagram with three lanes: Customer, AI System, and Finance Team.

Step 1: Order received. Customer submits a PO via email, EDI, or portal. AI reads the document in any format, extracts all relevant fields, and validates them against contract terms and pricing. Clean orders move forward automatically. Exceptions are flagged with the specific discrepancy and routed to the finance operations team for resolution.

Step 2: Credit assessment. AI cross-references the customer's current outstanding balance, recent payment history, and behavioral risk signals. Orders within credit policy are automatically approved and move to fulfillment. Orders that breach credit thresholds are routed to the credit team with a pre-assembled summary of the customer's financial profile and the specific flag.

Step 3: Fulfillment confirmed. Operations confirms delivery or service activation. AI receives the fulfillment signal and notifies the invoicing team to generate the invoice. No manual handoff required.

Step 4: Invoice generated and validated. Invoice is auto-generated from order and fulfillment data. AI validates GL coding, PO reference, tax treatment, and billing requirements against the customer's contract before the invoice is sent. Clean invoices are dispatched automatically. Flagged invoices are held and routed for human review with the specific issue identified.

Step 5: Collections scoring and outreach. AI scores all open receivables daily based on payment history, invoice value, dispute frequency, and behavioral signals. Low-risk accounts receive automated reminders. High-risk and high-value accounts are escalated to the AR team with full account context pre-populated.

Step 6: Payment received and matched. Incoming payments are read by AI regardless of remittance format. Payments are matched to open invoices using pattern recognition and contextual reasoning. Matched payments are posted to the ERP automatically. Unmatched exceptions are queued for human review with suggested matches pre-populated.

Step 7: Exceptions resolved and ledger updated. Disputed invoices, deductions, and residual unmatched payments are resolved through a structured exception workflow. Once resolved, the transaction posts to the ERP and the AR ledger reflects the accurate, current receivables position.

How Hyperbots Automates the O2C Cycle

Most O2C automation investments produce partial results because they try to cover the entire cycle thinly rather than solving the stages where the real cash is stuck. The honest reality is that for most mid-market finance teams, two stages account for the overwhelming majority of working capital leakage: cash application and collections. These are where payments sit unmatched, DSO inflates, and the collections team burns hours chasing accounts that may have already paid.

Hyperbots focuses precisely here, not because the other stages do not matter, but because fixing these two moves the needle on DSO, unapplied cash, and collections cost faster and more materially than anything else. The majority of cash in an O2C cycle flows through these two stages, and that is where the automation gap is most expensive.

Cash Application Co-Pilot

The Cash Application Co-Pilot automates the end-to-end matching of incoming payments to open invoices. It ingests payments from any source such as bank feeds, lockboxes, ACH, wire transfers, checks, email remittances, and customer portals and reads remittance advice in any format, including non-standard, incomplete, or inconsistent ones that rule-based tools cannot handle without manual intervention.

Finance-trained AI agents match payments to invoices using invoice numbers, PO references, amounts, dates, customer behavior patterns, and historical matching data. Matched payments post directly back to the ERP in real time with full GL coding and read-back validation. Unapplied cash is reduced to below 10%. Reconciliation costs are reduced by up to 80%. The volume of transactions requiring human review drops sharply, and the ones that do reach a reviewer arrive with suggested matches already pre-populated.

The system also handles deductions, short payments, and overpayments by classifying root causes and routing exceptions through configurable workflows rather than dumping them into a manual queue.

Collections Co-Pilot

The Collections Co-Pilot addresses the stage before cash arrives. It replaces aging-bucket-driven outreach with AI-driven dynamic prioritisation, continuously rescoring every open receivable based on payment behavior, invoice risk, dispute history, customer value, and behavioral signals. The collections team stops working a static list and starts working a ranked queue where effort is directed at the accounts that genuinely need attention today.

Dunning, follow-up emails, promise-to-pay tracking, and pre-due reminders all run autonomously. Accounts that will self-resolve with an automated nudge get one. Accounts that need a human conversation get an AR team member with the full account context already assembled. Early dispute signals such as price mismatches, PO discrepancies, quantity variances that are detected before the due date and routed to the right owner before they become aged items.

The outcomes: DSO reduced by up to 40%, cost to collect reduced by up to 70%, and more than 70% of collection tasks automated without adding headcount.

What Makes Hyperbots Different From Generic Automation

Most automation tools in this space apply fixed rules to structured data. They work when transactions are clean and predictable. They fail when transactions are messy, which in cash application and collections is the case most of the time. Customers bundle invoices, reference wrong numbers, take undocumented deductions, and pay partially without explanation. Collections queues are full of accounts with entirely different risk profiles that a static aging bucket treats identically.

Hyperbots handles this variability in three specific ways. The co-pilots are pre-trained on over 35 million financial document fields, which means the system understands non-standard remittance formats, industry-specific deduction codes, and customer payment patterns out of the box without months of configuration. The platform uses agentic reasoning rather than rule matching, interpreting context and handling exceptions the way a skilled AR analyst would rather than failing when a transaction does not fit a predefined template. And it integrates bidirectionally with the ERP in real time such as matched payments, resolved exceptions, and posting confirmations write back directly to the system of record, not to a parallel database that drifts from the truth.

The result is automation that holds up across the full range of transaction complexity, not just the clean, predictable subset that rules-based tools can handle.

Before and After: What Hyperbots Changes

O2C Stage | Before Hyperbots | After Hyperbots |

Cash application | Manual remittance matching across formats; large unapplied backlog distorting AR aging | AI reads any remittance format, matches and posts automatically; exceptions pre-populated for review |

Collections prioritisation | Aging-bucket outreach; same cadence applied to all accounts regardless of risk or payment behavior | Intent-based scoring daily; high-risk accounts escalated with full context, low-risk accounts automated |

Unapplied cash | Persistent backlog inflating apparent DSO | Reduced to below 10% |

DSO | Industry average 45 to 60 days in mid-market | Reduced by up to 40% |

Collections cost | High headcount cost relative to revenue collected | Reduced by up to 70% |

ERP posting | Manual or batch; ledger lags actual payment position by days | Real-time bidirectional write-back; AR ledger reflects true position after every matched payment |

Both Co-pilots connect natively to your existing ERPs such as Oracle NetSuite, SAP S/4HANA, SAP ECC, SAP B1, Microsoft Business Central, Sage Intacct, Sage 300, Deltek, and QuickBooks - reading and writing data in real time. The ERP remains the system of record. Hyperbots handles the two stages of O2C where most of the cash, and most of the manual effort, actually lives. Go-live is within one month. ROI is typically reached within six months.

See it in action with a demo or start your free trial today

Frequently Asked Questions

What is the difference between Order-to-Cash and accounts receivable?

Accounts receivable is one stage within Order-to-Cash. It covers the management of outstanding invoices after they have been sent. O2C is the full cycle: order intake, credit assessment, fulfillment, invoicing, AR management, collections, and cash application. Improving accounts receivable in isolation without addressing the stages before it, particularly invoicing accuracy and collections prioritization, produces limited improvement in overall cash performance.

What causes DSO to remain high even when the collections team is working hard?

High DSO almost always has multiple causes. Invoices going out late because fulfillment data is slow to reach finance. Invoice disputes caused by GL coding errors, wrong PO references, or incorrect billing terms. Collections effort directed at accounts that would have paid without intervention rather than the accounts that genuinely need attention. And cash application backlogs that mean payments received last week are still sitting unmatched, inflating apparent DSO. Addressing any one of these in isolation does not move the headline number. All of them need to be fixed together.

How does AI handle cash application when customer remittances are inconsistent?

This is the stage where rule-based automation most consistently fails, because customer payment behavior is genuinely unpredictable. Customers bundle invoices, reference wrong numbers, take undocumented deductions, and send partial payments without explanation. AI handles this variability through pattern recognition and contextual reasoning rather than fixed matching rules. It reads remittance advice in any format, identifies the most probable invoice matches based on amounts, dates, and historical patterns, and posts matched payments automatically. The exceptions that reach a human are genuinely ambiguous cases, not simply non-standard formats.

Can O2C automation work with an existing ERP rather than replacing it?

Yes, and this is the correct implementation model. The ERP is the system of record for the AR ledger, and automation that does not connect to it in real time creates a parallel record that diverges from the source of truth. AI co-pilots for O2C connect to existing ERP systems through native integrations, reading customer data, open invoices, and payment records directly from the ERP and writing matched payments and resolved exceptions back in real time.

How long does implementation take and when does the investment pay back?

With pre-trained AI co-pilots and pre-built ERP connectors, O2C automation is live within one month. ROI is typically realized within six months of go-live, driven by measurable reductions in DSO, collections headcount cost, and the finance team time consumed by manual cash application and exception handling.

For a broader view of how ERP systems manage business processes across the enterprise, including procurement, invoicing, accruals, and compliance, and how AI co-pilots extend ERP capability beyond what any platform delivers natively, the full guide to ERP and business processes is the right place to start.