Real-Time Budget Control in Procurement: How AI Stops Overruns Before They Happen

A complete guide to real-time budget control in procurement using AI, ERP integration, and policy enforcement to stop overruns before they occur.

Consider the following scenario, which is more common than most finance leaders would like to admit. A quarter concludes. The CFO reviews the consolidated spend report. Three departments have exceeded their procurement budgets, not marginally, but by amounts that require a formal board explanation. The natural question that follows is not simply how the overrun occurred, but why the organization's existing controls did not prevent it. The budget existed. The ERP was in place. The approval workflow was active. And yet the overspend happened, and was discovered only after the period had closed.

Budget overruns in procurement are almost universally a detection problem, not a data problem. The data to prevent them exists in every organization. The issue is that it is not being used at the right point in the process, which is the moment a purchase commitment is made, before a vendor is engaged, before a purchase order is raised, and before any obligation is incurred. This guide explains why that gap exists, what a well-designed budget control framework looks like, and how AI-powered automation is closing it.

What Is Budget Control in Procurement?

Budget control in procurement is the process of validating that a proposed purchase falls within the organization's approved financial limits before any commitment is made to a vendor.

It is not the same as budget reporting, which tells you what has already been spent. It is not the same as budget approval, which authorizes the budget allocation at the beginning of a period. Budget control is the active enforcement mechanism that sits between the approved budget and the purchase decision, ensuring that every requisition is evaluated against available funds before it progresses to a purchase order.

In a well-controlled procurement environment, no purchase order should be raised, and no vendor commitment should be made, without a confirmed budget check having been performed at the point of requisition. The budget check should reflect not just what has been spent to date, but what has already been committed in open purchase orders that have not yet been invoiced. Without that level of precision, the control is incomplete.

Budget control in procurement operates across three dimensions. The first is visibility: does the organization know its true available budget at any point in time? The second is enforcement: does the system prevent or escalate purchases that would breach the budget? The third is accountability: is there a complete, auditable record of every budget check, alert, and approval decision?

Most organizations have partial coverage across these three dimensions. Very few have all three operating in real time.

The Three Financial Figures That Drive Budget Control

Before examining why budget overruns occur, it is necessary to define the three financial concepts that any effective budget control framework must track. These are not interchangeable terms, and treating them as such is the root cause of most procurement overruns.

Budget is the authorized financial limit allocated to a department, cost center, project, or spend category for a defined accounting period. It is established through the annual or quarterly planning process, formally approved by finance leadership, and loaded into the ERP system as the baseline against which spend is measured. The budget figure is generally stable within a period and well-understood by all parties.

Committed spend is the aggregate value of purchase orders that have been formally raised and approved, but for which goods or services have not yet been delivered, invoiced, or paid. A purchase order is a legally binding financial commitment. The moment an organization raises a PO for $50,000 of consulting services, that $50,000 is committed against the relevant budget, regardless of when the invoice arrives or when the payment is processed. Committed spend is an obligation in substance even if it has not yet been recognized as actual expenditure in the accounting system.

Actual spend is the value of expenditure that has been formally invoiced by a vendor and posted to the general ledger following the completion of the accounts payable process. Actual spend is what appears in the profit and loss statement and in standard ERP budget variance reports. It represents completed financial transactions rather than forward-looking obligations.

The critical insight for budget control is this: the gap between committed spend and actual spend can represent weeks or months of procurement activity. During that interval, the ERP system may display available budget that is, in practice, already fully obligated through open purchase orders. A department manager reviewing their budget position in the ERP on the fifteenth of the month and seeing 40% remaining may not realize that an additional 35% has already been committed in purchase orders awaiting delivery and invoicing. The functional available budget is 5%, but the system reports 40%. Procurement continues. Invoices arrive. The overrun surfaces at period end.

What Budget Control Means for Each Stakeholder

Budget control is not purely a finance function. It affects every participant in the procurement process, and each stakeholder has a distinct interest in its effective operation.

For the CFO and finance leadership, budget control provides the assurance that organizational spend is being managed within authorized limits in real time, not retrospectively. It also provides the accruals accuracy needed for reliable financial reporting: when committed spend is tracked systematically, the gap between accrued and actual costs is minimized.

For department managers and budget owners, real-time budget control provides visibility into their true available balance at any point, including committed spend from open POs. This allows more informed purchasing decisions and eliminates the situation where a manager discovers mid-quarter that their budget is exhausted despite what the ERP dashboard showed.

For procurement and purchasing teams, budget control provides clear operational guidance: which requisitions can proceed under standard workflow, which require escalation, and which must be deferred pending budget availability. It removes the ambiguity that leads to approval delays and exception handling backlogs.

For internal audit, budget control provides an automated, timestamped record of every budget check, alert, policy enforcement decision, and approver action, without relying on manually assembled email chains or reconstructed approval logs.

Why ERP Budget Fields Alone Do Not Provide Adequate Control

Enterprise Resource Planning systems are designed to be reliable systems of record. They record completed transactions with precision and generate accurate historical reports. However, the fundamental architectural characteristic of most ERP systems is that they are updated when transactions are posted, not when commitments are made. This distinction is the source of most budget control failures.

In a standard ERP configuration, the budget encumbrance, which is the accounting entry that records the budget impact of a purchase order at the point it is raised rather than when it is invoiced, is often a manual step, an optional configuration, or a process that depends on consistent data entry discipline across every individual creating purchase orders. When that discipline is not maintained, the encumbrance ledger understates the organization's true commitments, and the available budget displayed to users is overstated accordingly.

Furthermore, ERP budget reports are typically generated at a point in time rather than updated continuously. A manager who checks their available budget at 9am may see a figure that does not reflect a purchase order raised by a colleague at 8:30am. For organizations where multiple departments draw from a shared category budget, this creates a race condition in which two budget owners can independently see available funds that, in aggregate, do not exist.

The consequence is that ERP budget fields, without additional controls, provide a historical view of what has been spent rather than a real-time view of what has been committed. Finance teams relying on ERP budget displays to prevent overruns are working with information that is structurally unable to perform that function.

How Procurement Budget Overruns Occur: Four Recognized Patterns

The mechanisms by which budget overruns occur are well-documented and consistent across organizations of different sizes and sectors. Understanding these patterns is necessary for designing controls that address root causes rather than symptoms.

Pattern 1: The committed spend gap. This is the most prevalent cause of procurement overruns. A manager views available budget in the ERP and, seeing a positive balance, raises additional purchase requisitions. The ERP budget figure does not reflect the committed spend from open purchase orders already in the system. By the time those purchase orders are delivered and invoiced, the actual spend against the budget exceeds the authorized limit. The manager acted reasonably on the information available. The information was structurally incomplete.

Pattern 2: Concurrent commitment against shared budgets. In organizations where multiple cost centers or departments draw from a shared category budget, such as a central IT equipment budget or a corporate professional services allocation, simultaneous requisition activity can collectively commit expenditure that exceeds the available balance, even when each individual requisition appears acceptable in isolation. Without a system that reduces the displayed available balance at the moment each requisition is committed, this aggregation effect is invisible until period-end reconciliation.

Pattern 3: Budget-blind approval workflows. A purchase order approval process that routes requisitions based on value thresholds informs approvers about the magnitude of the requested purchase. It does not inform them about whether the organization has authorized budget available for it. An approver presented with a well-justified requisition for a legitimate business requirement will ordinarily approve it, having no practical means of checking the current budget position without leaving the approval workflow and navigating to a separate budget report.

Pattern 4: Period-end spend acceleration. Organizational spending characteristically accelerates at the close of quarters and financial years, as departments seek to utilize remaining budget allocations before they lapse. This generates a concentrated volume of purchase requisitions at precisely the point when budget positions are most constrained and when manual verification processes are least reliable due to time pressure and volume.

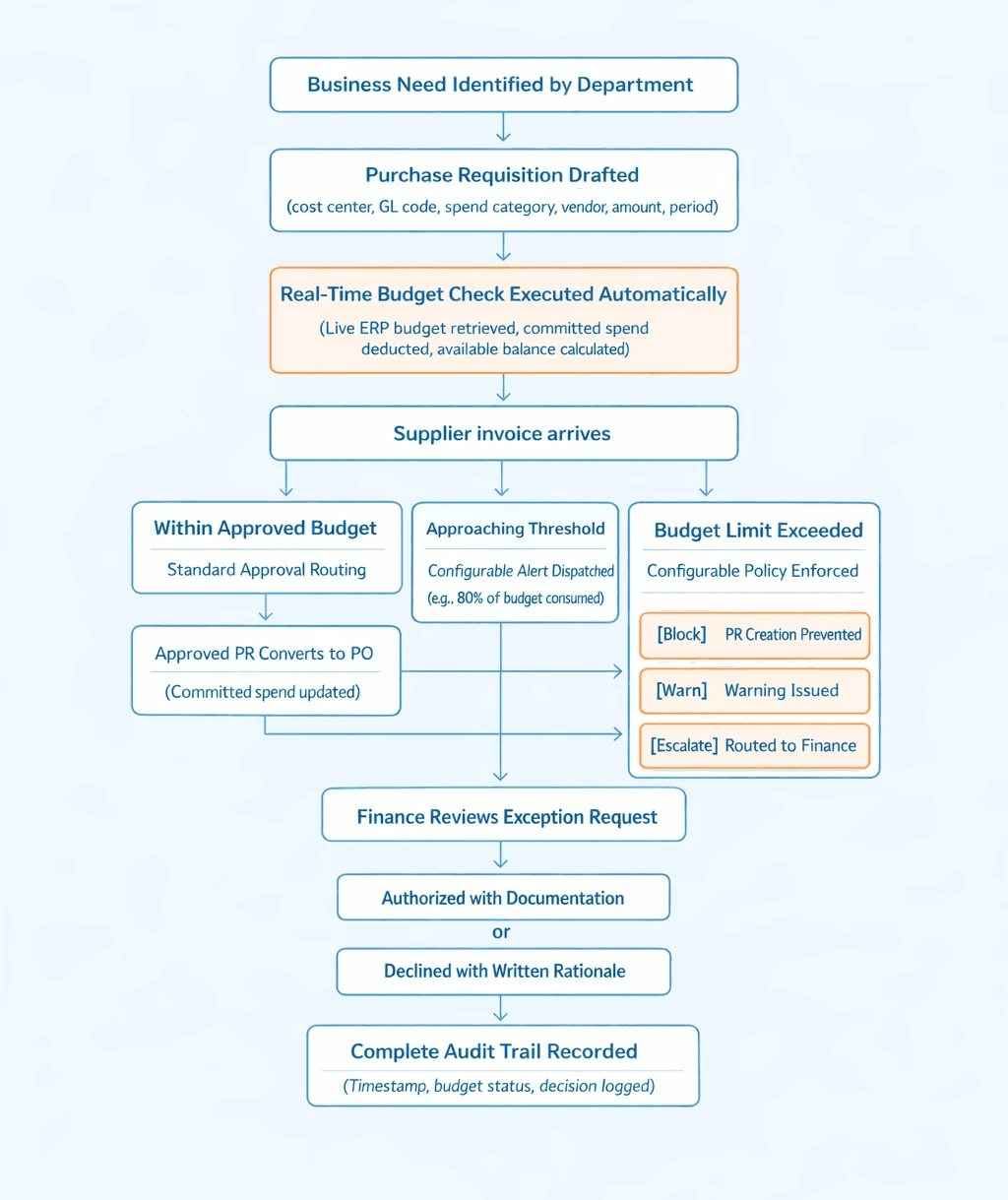

The Framework for Effective Real-Time Budget Control

Effective budget control requires interception at the earliest point of commitment, which is the purchase requisition stage, before any vendor is engaged and before any legal obligation is created. The following flowchart illustrates the process flow that a well-designed budget control system should enforce:

The framework depends on three conditions being satisfied simultaneously: budget data retrieved in real time from the ERP at the moment of requisition, committed spend deducted from available budget before the check is performed, and organizational policy enforced automatically without relying on individual judgment or memory.

Where Current Approaches Fall Short

Most procurement organizations have implemented at least rudimentary budget controls. The limitations of those controls, however, are systematic rather than incidental.

Manual verification processes are not scalable controls. A policy requiring department managers to verify available budget before raising a requisition is a procedural guideline, not an automated control. Its effectiveness is entirely dependent on individual compliance, which degrades under time pressure, at high requisition volumes, and during personnel transitions.

ERP encumbrance accounting requires perfect process discipline. Commitment accounting within ERP systems, which records the budget impact of a purchase order at the point of raising rather than invoicing, is technically capable of addressing the committed spend gap. In practice, however, it requires every individual involved in purchase order creation to follow the encumbrance posting process without exception. A single instance of a PO raised outside the standard workflow, or a manual purchase without a corresponding encumbrance entry, creates a gap in the commitment ledger that cannot be identified until an overrun has occurred.

Periodic budget reports are retrospective instruments. A monthly budget variance report is an important management tool for understanding historical spend patterns. It is not a control for preventing future overruns. By the time a report identifies that a department has exceeded its budget allocation, the expenditure has been committed, the vendor has been engaged, and the financial obligation is established.

Value-threshold approval routing does not incorporate budget context. Approval workflows designed to route high-value purchases to senior approvers provide governance over the authorization of large individual transactions. They do not provide governance over cumulative budget consumption. An approver who receives a $15,000 requisition routed because it exceeds the delegated approval limit has no automated visibility into whether the organization has $15,000 of available budget remaining in the relevant cost center.

How AI Automation Addresses the Budget Control Gap

The application of AI to budget control does not introduce conceptually new principles. The principles of sound budget management are well-established. What AI provides is the operational capability to apply those principles consistently, at scale, and in real time, without dependence on manual processes or individual discipline.

The value of policy-driven AI in procurement is its consistency. A configured policy executes identically at every transaction, regardless of volume, time of day, seniority of requester, or proximity to period end. There is no degradation in enforcement under pressure.

For procurement budget control specifically, AI automation delivers three capabilities that manual processes cannot reliably replicate.

Live budget retrieval at the point of requisition. An AI system connected directly to the ERP retrieves the current budget position, including all posted actuals and all committed open purchase orders, at the moment a new purchase requisition is being created. The figure presented to the requester and approver reflects the actual available balance at that specific moment, not a cached snapshot from an earlier point in the day or period.

Real-time deduction of committed spend. Every approved requisition and open purchase order reduces the displayed available balance immediately and simultaneously. When a second department head raises a requisition against the same shared budget, the system has already deducted the first department's committed spend from the available balance. The race condition described earlier is eliminated structurally rather than procedurally.

Configurable policy enforcement administered by finance. The organization's budget threshold policies, including the actions to be taken when spending approaches or exceeds authorized limits, are configured by finance leadership and enforced automatically by the system. The configuration requires no IT involvement, no code changes, and no integration work beyond the initial ERP connection. Different cost centers, spend categories, entity types, and value ranges can carry distinct policies reflecting the organization's risk tolerance and governance structure.

How Hyperbots Delivers Real-Time Budget Control

The Procurement Co-Pilot from Hyperbots incorporates a dedicated Budget Control capability that addresses each of the failure modes described in this guide. The following capabilities are confirmed from the Hyperbots product documentation.

Real-time budget monitoring integrated into the requisition workflow. The co-pilot tracks available budget positions in real time as purchase requisitions are submitted. Budget data is retrieved directly from the connected ERP at the moment of each requisition, reflecting posted actuals and all committed open purchase orders. The requester sees the true available balance before the requisition is submitted for approval.

Automated threshold alerts with contextual information. When a purchase requisition approaches or exceeds a configured budget threshold, the co-pilot dispatches immediate alerts to the requester and the relevant budget owner. Each alert contains the current budget position, the value of the requisition being submitted, and the remaining available balance following the proposed commitment, providing decision-makers with complete context without requiring them to navigate to a separate system.

Native ERP integration for continuous budget synchronization. The co-pilot connects directly to the organization's ERP and finance systems, maintaining continuous synchronization of budget data. The procurement workflow and the financial ledger operate from a single, consistent data source, eliminating the discrepancy between what the procurement system displays and what the ERP records.

Configurable approval workflows for budget exceedances. Purchase requisitions that exceed authorized budget limits are automatically routed in accordance with the organization's configured policy. The available options include blocking the requisition entirely pending budget reauthorization, requiring mandatory escalation to finance leadership for exception approval, or applying a documented-justification workflow in which the requester proceeds with a formal written rationale. Distinct policies can be configured for different departments, spend categories, geographic entities, and value bands.

Structured exception alerts for out-of-budget requisitions. When a requisition exceeds a budget limit, the co-pilot dispatches structured alerts containing the specific overage amount, the current budget position by cost center, and the identity of the requester. Finance and procurement leadership receive the information required for a timely and informed decision without the need for manual data assembly.

The measurable outcomes for procurement automation ROI include purchase requisition creation completed in under 5 minutes with budget validation incorporated into the same workflow, PO creation and dispatch time reduced by 80%, accruals variance at period end reduced to less than 5% between accrued and actual costs, and a complete, automatically maintained audit trail for every budget check and approval decision. Implementation is complete and live within one month. Return on investment is typically realized within 6 months of go-live.

Before and After: Budget Control in Procurement

Dimension | Without Real-Time Budget Control | With Hyperbots AI Budget Control |

Budget visibility at requisition | Stale ERP snapshot, committed spend not reflected | Live ERP retrieval including all open POs at the precise moment of requisition |

Overrun detection | At invoice posting, weeks after the vendor commitment was made | At requisition stage, before any vendor obligation is created |

Shared budget management | Race condition between cost centers, overcommitment invisible until period end | Committed spend deducted immediately, true available balance displayed to all requesters |

Policy enforcement | Dependent on individual compliance with procedural guidelines | Block, warn, or escalate enforced automatically and consistently at every requisition |

Approver context | Request value displayed, budget position not visible in approval workflow | Full context: request value, current budget, committed spend, and available balance |

Alert mechanism | None until monthly variance report is produced | Immediate alert at configurable threshold levels, approaching and exceeding limit |

Accruals accuracy at period end | Manual estimation, material variance common | Less than 5% variance between accrued and actual costs |

Audit trail | Reconstructed manually from email correspondence and ERP logs | Automatically maintained timestamped record of every check, alert, decision, and approver |

PR creation time | 30 to 60 minutes including manual budget verification | Under 5 minutes with budget validation integrated into the requisition workflow |

PO creation and dispatch | Manual process, inconsistent timelines | 80% reduction in creation and dispatch time |

FAQs

What is budget control in procurement, and how does it differ from budget reporting?

Budget control in procurement is the active enforcement of financial limits at the point of purchase commitment, before a vendor obligation is created. It prevents overspending by validating available funds at the requisition stage. Budget reporting, by contrast, is a retrospective function that records and communicates what has already been spent. The two serve different governance purposes and operate at different points in the procurement cycle.

What is the difference between committed spend and actual spend?

Actual spend is expenditure that has been invoiced by a vendor and posted to the general ledger. It appears in the profit and loss statement and in standard ERP budget reports. Committed spend is the value of approved purchase orders that represent financial obligations but have not yet been invoiced or paid. ERPs typically display actual spend against budget, which causes available budget to appear larger than it is in practice because open purchase order commitments are not deducted.

Why do budget overruns occur in organizations that have both an ERP and an approval workflow?

Because ERP budget fields reflect posted actuals rather than committed spend, and because approval workflows route on the basis of transaction value rather than budget availability. The combination means that approvers are authorizing purchases against a budget figure that excludes existing commitments, and that the true extent of budget consumption only becomes visible when invoices are posted, often weeks after the commitment was made.

What does configurable policy enforcement mean in the context of budget control?

It means the organization determines, in advance, what action is taken when a purchase requisition reaches a budget threshold. The available configurations typically include blocking the requisition until additional budget is authorized, requiring escalation to finance leadership for exception approval, or permitting the requisition to proceed with a mandatory documented justification. Each cost center, spend category, or value band can carry a distinct policy aligned to the organization's governance requirements.

Does implementing real-time budget control require changes to the existing ERP?

No changes to the ERP are required. The AI co-pilot layer connects to the ERP through a pre-built native connector, retrieves budget data in real time, and applies the configured enforcement policies at the requisition stage. Budget check outcomes and approval decisions are written back to the ERP as part of the standard workflow. The ERP continues to function as the system of record. Implementation is complete within one month.

How does real-time budget control improve the month-end close process?

When committed spend is tracked systematically throughout the accounting period, the accrual calculation at period end becomes significantly more precise. Finance teams have accurate visibility into expenditure that has been committed but not yet invoiced, allowing accruals to be calculated on a factual basis rather than estimated. The result is a reduction in accruals variance to less than 5% between accrued and actual costs, compared with the material variances commonly produced by manual estimation processes.

For a comprehensive view of how artificial intelligence is transforming purchase order processing across the full procurement lifecycle, from requisition through approval, dispatch, delivery, and invoice matching, see the guide to how AI is transforming purchase order processing.

The Hyperbots Procurement Co-Pilot retrieves live ERP budget data at every purchase requisition, enforces configurable spend policies automatically, and routes exception requests with full contextual information. Purchase requisition creation in under 5 minutes. PO dispatch time reduced by 80%. Live within one month.

Request a demo at hyperbots.com.