DCAA Timekeeping & Labor Cost Tracking for Government Contractors

A practical guide to DCAA-compliant timekeeping and labor tracking.

Labor charging is consistently one of the highest-risk audit areas for federal government contractors, and for good reason. On most cost-reimbursable and time-and-materials contracts, labor is the single largest cost element, yet it is also the cost element with the least physical evidence behind it. There is no invoice, no packing slip, no purchase order to reconcile against only an employee's own record of how a day was spent.

That gap between cost significance and documentation strength is exactly why the Defense Contract Audit Agency (DCAA) scrutinizes timekeeping so closely, and why DCAA compliant timekeeping sits at the center of nearly every accounting system review, floor check, and incurred cost audit a contractor will face.

Getting labor charges wrong does not stay contained to a single timesheet. It ripples through contract profitability, distorts indirect rates, delays billing, and, in the worst cases, puts a contractor's accounting system adequacy determination at risk. This guide breaks down what DCAA timekeeping requirements actually demand, how contractors manage them inside Deltek Costpoint, where manual processes quietly break compliance, and how AI-driven automation is closing the gap between labor tracking and the rest of the finance function.

What Are DCAA Timekeeping Requirements?

DCAA does not certify or approve specific timekeeping software. Instead, it evaluates whether a contractor's accounting system, including its labor system, meets the criteria in DFARS 252.242-7006, Accounting System Administration, which explicitly requires "a timekeeping system that identifies employees' labor by intermediate or final cost objectives" and "a labor distribution system that charges direct and indirect labor to the appropriate cost objectives." FAR 31.201-2 reinforces this by making contractors responsible for maintaining records adequate to demonstrate that labor costs claimed were actually incurred and are allocable to the contract.

In practice, auditors are testing whether a contractor's written policy matches what employees actually do day to day. That consistency, not the sophistication of the software, is what determines whether a labor system passes review.

Core DCAA Timekeeping Requirements

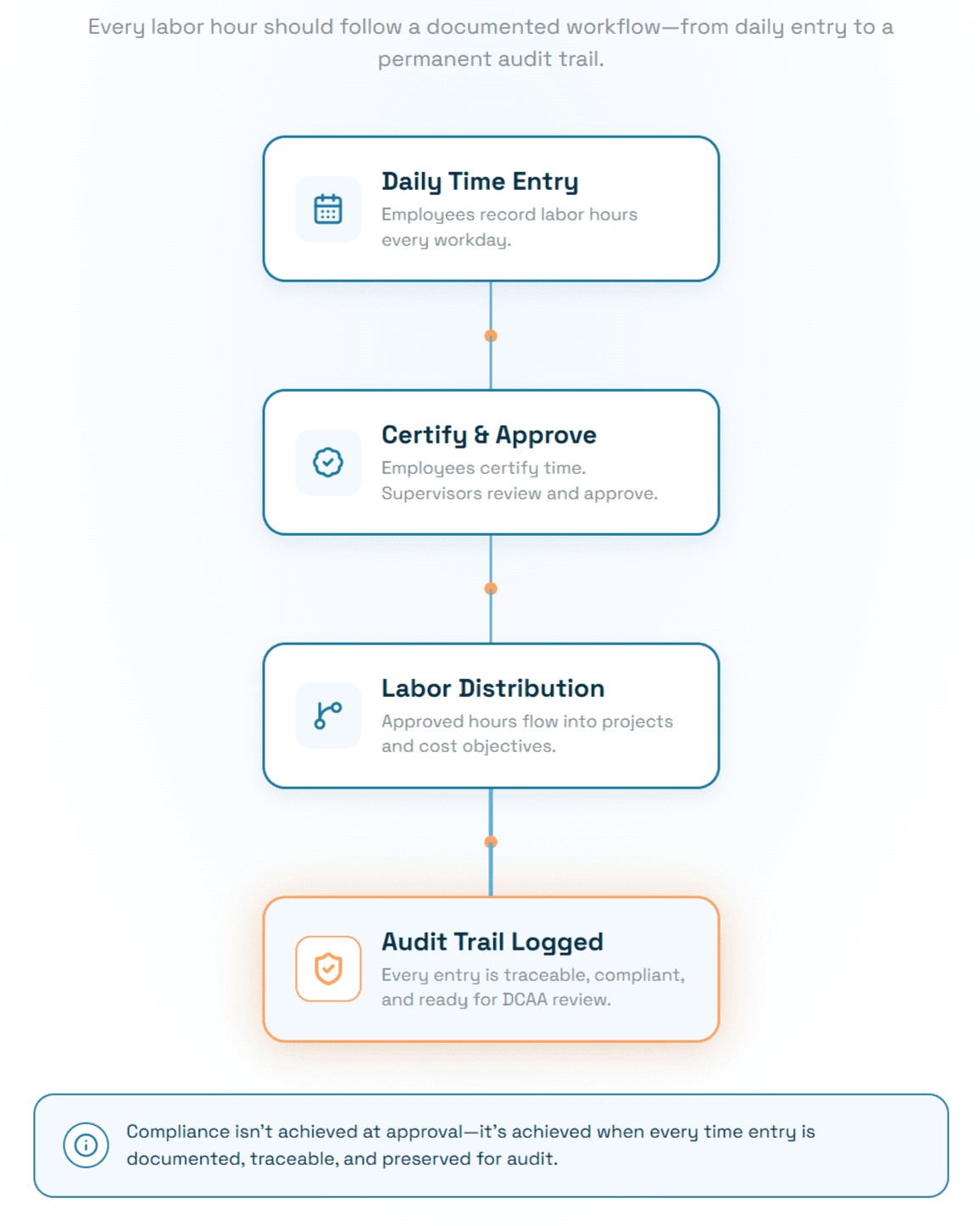

Total Time Accounting (TTA): All hours worked must be recorded, not just hours billed to a contract. This includes direct labor, indirect labor, overtime (compensated and uncompensated), and leave.

Daily time entry: Time should be recorded contemporaneously, at the end of each workday. Weekly or retroactive entry is considered a compliance gap because it relies on memory rather than real-time documentation.

Direct vs. indirect labor segregation: Every hour must be charged to the correct cost objective, distinguishing labor that is directly chargeable to a contract from labor that supports overhead or G&A functions.

Employee self-recording and certification: Employees are responsible for entering and certifying their own time. Only in documented exceptions (illness, extended leave) should someone else enter time on an employee's behalf.

Supervisor review and approval: A supervisor familiar with the employee's actual work must review and approve timesheets; supervisors accountable for contract budgets should not have unrestricted ability to alter employee time charges.

Documented correction procedures: Retroactive edits must be logged with what changed, who changed it, and why, rather than silently overwritten.

Audit trail requirements: The system must preserve a complete history of entries, approvals, and corrections that auditors can reconstruct during a floor check or incurred cost audit.

Written timekeeping policy: Policies must be documented, distributed to employees, and reinforced through periodic training.

Record retention: Contractors should generally retain timekeeping records for the duration required by contract terms, commonly cited as a minimum of two to three years after final payment, with many firms retaining records longer as a matter of practice.

DCAA validates these controls through labor floor checks, unannounced interviews and reviews conducted to confirm that documented policy matches actual employee behavior. A contractor can have a technically compliant written policy and still receive audit findings if employees cannot explain how they record time or if supervisors rubber-stamp approvals without genuine review.

Managing DCAA-Compliant Timesheets in Deltek Costpoint

Deltek Costpoint is the dominant ERP platform in the government contracting space precisely because its Time & Expense module is built around DCAA's labor system criteria rather than retrofitted to them. Electronic timesheets in Costpoint enforce charge-code validation against approved contracts and tasks, require employee certification at submission, and route timesheets through configurable supervisor approval workflows before labor costs post to the general ledger.

Costpoint's approach to manage timesheets compliantly centers on a few structural controls: charge trees that restrict which project and task codes an employee can select, linked user-defined tables that tie labor categories to specific contracts, and locked timesheet periods once approvals are finalized, so that corrections require a documented reopening process rather than a silent edit. Labor distribution runs automatically once timesheets are approved, charging direct and indirect hours to the correct cost objectives and feeding payroll and project accounting in the same cycle.

This tight coupling between timekeeping, payroll integration, and project accounting is what allows Costpoint customers to satisfy the DFARS 252.242-7006 labor distribution criterion without a separate reconciliation step.

That said, a properly configured Costpoint environment does not eliminate every operational challenge. Contractors still commonly struggle with:

Employees missing daily entry deadlines, particularly on multi-project or matrixed teams

Charge code sprawl that makes it hard for employees to select the correct project quickly

Delayed corrections that pile up around month-end close

Supervisors approving timesheets in bulk without reviewing individual entries against actual work assignments

Disconnected downstream processes like expense reports, accruals, and GL coding, that still rely on manual review even after labor data is captured correctly

Costpoint gives contractors the labor system controls DCAA expects. What happens to that labor data afterward, in accruals, expense validation, and month-end close, is often where the manual effort, and the audit risk, actually lives.

Where Manual Timekeeping Breaks Compliance

Contractors that rely on spreadsheets, paper timecards, or loosely governed digital tools tend to fail DCAA scrutiny in predictable, recurring ways:

Late or batch entries. Recording a week's worth of hours in one sitting on Friday afternoon undermines the contemporaneous-record standard auditors expect.

Shared logins or proxy entry without documentation. When someone other than the employee enters time without a documented, approved reason, DCAA treats this as a fundamental self-certification failure.

Spreadsheet-based tracking. Spreadsheets carry no built-in audit trail, no charge-code validation, and no reliable way to prove that a number wasn't changed after the fact.

Incorrect labor charging. Miscoding direct labor as indirect, or vice versa, distorts both contract cost data and the indirect rate pools that apply across the entire contract portfolio.

Missing or delayed supervisor approvals. Unapproved timesheets create gaps in the audit trail and, if labor still posts to the GL, expose the contractor to reliability findings.

Undocumented retroactive edits. A DCAA auditor who cannot see what changed, when, and why on a corrected timesheet will treat the entire record as unreliable.

Weak or absent audit trails. Without a system-enforced log of entries, approvals, and changes, contractors cannot reconstruct the record floor checks required.

Incomplete documentation. Missing training records, undocumented policy exceptions, and informal correction processes all become findings during accounting system audits.

Manager overrides. Supervisors who can freely edit employee time charges, especially supervisors accountable for hitting a contract budget, create the exact internal control weakness DFARS 252.242-7006 is designed to prevent.

Manual expense-to-timesheet matching. When travel, materials, or subcontractor costs tied to a labor-intensive task are reconciled by hand, errors and delays compound at month-end close.

The financial consequences of these failures extend well beyond a single audit finding. A significant deficiency in the labor system can lead to disallowed costs, withheld payments on cost-reimbursable contracts, conversion of favorable contract terms, and,in an accounting system audit, a broader finding that jeopardizes eligibility for future cost-type awards.

How AI Improves Labor Cost Accuracy Beyond Timekeeping

A compliant timekeeping system, whether built on Costpoint or another ERP, solves the labor capture problem. It does not solve everything downstream of labor capture and that is where a growing number of finance teams are applying AI.

It's worth being direct about scope here: platforms like Hyperbots are not timekeeping applications, and government contractors should continue to rely on their ERP's certified labor system, Costpoint or otherwise, to record, certify, and approve employee time. Software time entry and DCAA-specific labor controls remain squarely an ERP function. Where AI adds value is in the finance workflows that consume labor and project cost data once it has already been recorded and approved.

Once labor hours post through the ERP, several downstream processes still tend to rely on manual review, and each one carries its own compliance and accuracy exposure:

Expense validation: Verifying that travel and other direct-charge expenses tied to labor-intensive tasks match contract terms and per diem policy before they hit the GL, similar to the logic Hyperbots applies in invoice validation.

Labor distribution reconciliation: Cross-checking that GL postings from Costpoint's labor distribution match project budgets and burn rates, flagging anomalies before month-end close rather than during it.

Policy validation: Applying company-specific charging policies consistently across contracts, similar to how AI assists with broader finance compliance checks in AP and procurement.

Receipt and expense matching: Automating the reconciliation of receipts against expense reports connected to project work, reducing the manual matching burden that often falls on program accountants.

GL coding: Applying learned coding patterns to ensure labor-adjacent transactions, subcontractor invoices, travel, materials, post to the correct project and cost objective, an extension of the discipline covered in GL coding best practices.

Month-end accrual support: Identifying unbilled labor-related liabilities, such as subcontractor time not yet invoiced, and supporting the accrual discovery and booking process so close doesn't stall waiting on late documentation.

Audit documentation: Maintaining a system-generated, explainable record of how downstream financial data was validated, which complements the labor audit trail Costpoint already produces and supports the kind of AI-driven auditability auditors increasingly expect to see.

Exception detection: Surfacing anomalies, a labor charge that doesn't align with an approved task, a GL entry that deviates from historical coding patterns, for human review rather than letting them pass silently to close.

Workflow automation: Routing exceptions, approvals, and documentation requests to the right person automatically, reducing the manual chase that typically consumes finance teams during pre-award and post-award accounting system reviews.

For contractors running Costpoint specifically, this kind of automation sits alongside the ERP rather than replacing any part of it, connecting to Costpoint to pull approved labor and project data and apply automation to the finance processes that follow, including the Chart of Accounts coding conventions Costpoint environments typically use. For contracts involving open-ended service arrangements, similar logic extends to matching strategies for time-and-material engagements, where labor and invoice data must reconcile against variable-quantity contract terms.

The result is not a replacement for DCAA-compliant timekeeping controls. It's a tighter, more auditable connection between the labor data a compliant timekeeping system produces and the finance processes, accruals, GL coding, expense validation, that determine whether the resulting cost data holds up under audit.

Conclusion

DCAA-compliant timekeeping is not a single feature or checkbox, it's a combination of daily discipline, documented policy, and system controls that together produce labor cost data auditors can trust. Total time accounting, clear direct/indirect segregation, employee certification, supervisor approval, and a defensible audit trail form the foundation. Deltek Costpoint provides the labor system controls DCAA expects, but the accuracy of the broader cost picture, accruals, GL coding, expense validation, still depends on what happens after time is recorded and approved.

Contractors that treat timekeeping and downstream labor cost accuracy as separate problems tend to find compliance gaps at the worst possible moment: during a floor check or an incurred cost audit. Closing that gap means pairing disciplined timekeeping practices with automation that keeps the finance processes surrounding labor data just as accurate and audit-ready.

If your team is looking to strengthen labor and expense accuracy alongside your existing Costpoint or ERP environment, request a demo to see how AI-driven finance automation supports stronger DCAA compliance from timekeeping through close.

Frequently Asked Questions

Q1. What is DCAA compliant timekeeping?

DCAA compliant timekeeping is a labor tracking system and set of practices that meet the accounting system criteria in DFARS 252.242-7006 and FAR 31.201-2 including daily time entry, total time accounting, direct/indirect segregation, employee certification, supervisor approval, and a documented audit trail for corrections.

Q2. What are DCAA timekeeping requirements?

Core requirements include recording all hours worked (not just billable hours), daily contemporaneous entry, accurate charging to direct or indirect cost objectives, employee self-certification, supervisor review and approval, documented correction procedures, and retained records that support labor floor checks and incurred cost audits.

Q3. How often should employees enter time?

Employees should enter time daily, at the end of each workday. DCAA treats weekly or retroactive entry as a compliance risk because it relies on memory rather than a contemporaneous, verifiable record of work performed.

Q4. Can timesheets be corrected?

Yes, but corrections must be documented, showing what was changed, who made the change, and why, rather than silently overwritten. Most compliant systems lock a timesheet after approval and require a formal reopening process for any retroactive edit.

Q5. Does Deltek Costpoint support DCAA compliance?

Costpoint's Time & Expense module is built around DCAA's labor system criteria, including charge-code validation, employee certification, configurable approval workflows, locked periods, and automated labor distribution to direct and indirect cost objectives. Proper configuration and consistent use are still required to maintain compliance.

Q6. What software helps government contractors maintain compliant labor records?

Government contractor timekeeping software, most commonly an ERP-integrated system like Deltek Costpoint, provides the core labor system controls DCAA requires. AI-driven finance automation can complement it by improving the accuracy of downstream processes such as accruals, GL coding, and expense validation tied to labor-intensive project work.

Q7. What happens if a contractor fails a DCAA timekeeping review?

Consequences can include disallowed labor costs, withheld payments on cost-reimbursable contracts, conversion of contract terms, and broader findings against the contractor's accounting system adequacy which can affect eligibility for future cost-type contract awards.

Q8. Is manual or spreadsheet-based timekeeping ever acceptable to DCAA?

Paper or manual systems can be acceptable for smaller contractors if strong controls are in place such as secure storage, ink entries, documented corrections, employee certification, and supervisor approval. As headcount and contract complexity grow, most contractors move to electronic systems for reliability and audit-trail strength.