DCAA-Compliant ERP: 2026 Buyer's Guide + How AI Keeps You Audit-Ready

A practical guide for government contractors evaluating DCAA-compliant ERP software, understanding compliance requirements, and using AI to strengthen financial controls, improve data quality, and simplify audit preparation.

A DCAA-compliant ERP is an enterprise resource planning system configured to support the accounting requirements of the Defense Contract Audit Agency such as timekeeping controls, indirect cost pools, segregation of unallowable costs, and an audit trail sufficient to withstand an incurred cost audit or a pre-award accounting system review. For finance leaders at government contractors, this isn't optional infrastructure. It's the mechanism that determines whether a contract is eligible for cost-reimbursement in the first place.

Most contractors don't lose that eligibility because they picked the wrong software. They lose it or spend months remediating a finding because the system was never asked to prove itself under the specific conditions an auditor tests: a bulk-approved timesheet correction from eighteen months ago, an indirect pool that absorbed three miscoded invoices in Q2, a billing package that reconciles to the GL on the surface but not at the transaction level underneath. Those are the moments a Standard Form 1408 pre-award survey or an incurred cost audit is designed to surface.

This guide walks through what DCAA compliance actually requires, how the ERP and project accounting platforms contractors evaluate most often compare, where the operational gaps tend to show up even in systems that are technically compliant, and where AI-based validation is starting to close some of those gaps without becoming the system of record itself.

What DCAA Compliance Actually Means for an ERP

The DCAA does not certify or approve software. There is no official "DCAA-approved" software list, despite how the term is frequently marketed. Instead, the DCAA evaluates whether a contractor's accounting system, software, policies, and internal controls combined, satisfies the criteria outlined in the Standard Form 1408 Preaward Survey of Prospective Contractor Accounting System and the DCAA's Audit Manual (commonly referenced as DCAM 5-300 series).

A system is assessed against several core requirements:

Segregation of direct and indirect costs. The accounting structure must clearly separate costs chargeable to specific contracts from indirect costs allocated across a cost pool.

Identification and exclusion of unallowable costs. FAR Part 31.2 lists categories of cost that cannot be billed to the government, such as alcohol, entertainment, or certain legal fees. The system must isolate these so they never enter a billable cost pool.

Timekeeping with daily, contemporaneous entry. DCAA timekeeping standards require that labor be recorded daily, by the employee performing the work, with supervisor approval and an audit trail of any corrections.

Allocation of indirect costs through defined cost pools and bases. Overhead, fringe, and G&A pools must be calculated consistently and traceable to the general ledger.

Billing that reconciles to the general ledger. Invoices submitted to the government must tie directly back to recorded, supported costs, not estimates or manual adjustments outside the system.

An audit trail for all transactions. Every cost, from initial entry through allocation and billing, must be traceable without requiring the auditor to take the contractor's word for it.

It is worth noting plainly: DCAA compliance is a function of process and controls, not a checkbox in software configuration. A contractor can own project accounting software built specifically for government work and still fail an audit if timekeeping discipline, cost pool definitions, or unallowable cost identification are not enforced consistently. In practice, this is usually where the disconnect shows up first, not in the software's capability, but in whether the people entering and approving transactions are applying that capability the same way every time.

The Framework: What a Compliant System Needs to Demonstrate

Most experienced government contract auditors and consultants organize DCAA accounting system requirements into four operational pillars. Understanding this framework helps finance leaders evaluate any ERP or project accounting platform against the same criteria the DCAA itself applies.

1. Job cost accounting structure. The general ledger and project accounting module must support cost accumulation by contract, task order, and CLIN (Contract Line Item Number), with the ability to roll costs up for billing and down for variance analysis.

2. Labor distribution and timekeeping controls. This is consistently the area where contractors fail pre-award surveys. The system needs electronic timekeeping with audit logs, manager approval workflows, and the ability to demonstrate that labor charges match the work actually performed.

3. Indirect rate calculation and application. The ERP should calculate provisional and actual indirect rates, apply them consistently across contracts, and support the rate true-up process required for incurred cost submissions (ICE submissions under FAR 52.216-7).

4. Billing and reporting that reconcile without manual intervention. Public vouchers, SF1034/1035 forms, or invoices submitted through Wide Area Workflow (WAWF) should trace directly to GL detail.

A practical way to think about this: the ERP is the system of record, but compliance lives in the consistency between what the system captures and what actually happened operationally. A gap between the two, an uncoded timesheet correction, a manually adjusted indirect rate, an unallowable expense routed into a billable pool, is exactly what a DCAA auditor is trained to find.

Comparing Leading ERP and Project Accounting Platforms

There is no single "best" DCAA-compliant ERP. The right choice depends on contractor size, contract mix (cost-reimbursable vs. fixed-price vs. T&M), and in-house accounting maturity. A broader playbook for medium business ERP selection offers useful evaluation criteria beyond government-specific needs. The table below compares platforms most commonly evaluated by government contractor finance teams.

Platform | Best Fit | DCAA-Relevant Strengths | Considerations |

Deltek Costpoint | Mid-size to large contractors, especially defense and aerospace | Purpose-built for government contracting; native job costing, indirect rate calculation, and timekeeping designed around FAR/CAS | Higher implementation cost and longer rollout; requires dedicated administration expertise |

Unanet | Small to mid-size contractors and professional services firms | Project-centric accounting with strong timekeeping and billing controls; faster implementation than Costpoint | Less depth in complex multi-segment CAS environments compared to Costpoint |

Microsoft Dynamics 365 (with GovCon add-ons) | Mid-market contractors already standardized on Microsoft | Flexible reporting, broad ecosystem integration, lower licensing cost | DCAA-specific functionality typically requires third-party ISV add-ons rather than native capability |

QuickBooks (with GovCon timekeeping add-ons) | Very small contractors or new entrants to government work | Low cost, familiar interface, fast to deploy | Generally considered minimally adequate for pre-award surveys; lacks native indirect rate and job cost sophistication at scale |

NetSuite (with project accounting modules) | Growing contractors needing cloud scalability | Real-time reporting, strong multi-entity consolidation | Government-specific functionality is largely configured rather than out-of-the-box |

A point worth making clearly: passing a pre-award survey with QuickBooks or a lightly configured NetSuite instance is possible for very small contractors, but manual workarounds become harder to defend under audit as contract volume grows. Many GovCon consultants point to the first cost-reimbursable award, or revenue in the low eight figures, as the practical trigger for evaluating a project-accounting-native platform like Costpoint or Unanet though the right timing depends more on contract mix and audit exposure than on revenue alone. For contractors weighing this transition more broadly, a general ERP for professional services guide covers project accounting and time/billing considerations that overlap significantly with government contracting needs, and a step-by-step ERP implementation guide is useful for planning the migration itself.

Common Operational Gaps Even in Compliant Systems

Owning the right software does not guarantee passing an audit. In practice, the gaps that cause DCAA findings tend to cluster around four recurring issues.

Timekeeping discipline drifts over time. Electronic timesheets solve the daily-entry requirement on paper, but the failure mode DCAA floor checks are built to catch what happens downstream of entry. A supervisor with forty direct reports approves a week of timesheets in one batch on a Friday afternoon rather than reviewing each employee's hours against the work actually performed. An employee realizes three weeks later that four hours were charged to the wrong task order and submits a correction, but the justification field gets a placeholder note instead of a real explanation. By the time a controller is reconciling labor distributions for the monthly indirect rate calculation, dozens of these small corrections have accumulated, none individually alarming, but collectively enough that an auditor doing a floor check can reasonably ask whether the approval process is a control or a formality.

Unallowable costs are caught manually, if at all. FAR 31.205 unallowable cost categories (entertainment, alcohol, certain travel, lobbying costs) require a reviewer to recognize them at the point of entry. Manual AP review is inconsistent, especially across high invoice volumes.

Audit trail gaps appear at the transaction level, not the system level. The ERP itself may log changes, but if the underlying source document, an invoice, a PO, a timesheet correction, was never validated against policy before entry, the audit trail documents a flawed transaction cleanly rather than catching the flaw itself.

This last point is the crux of where most DCAA findings originate: the ERP faithfully records what it is told, but it does not independently validate that what it is told is correct, allowable, and properly classified before that data becomes part of the permanent financial record.

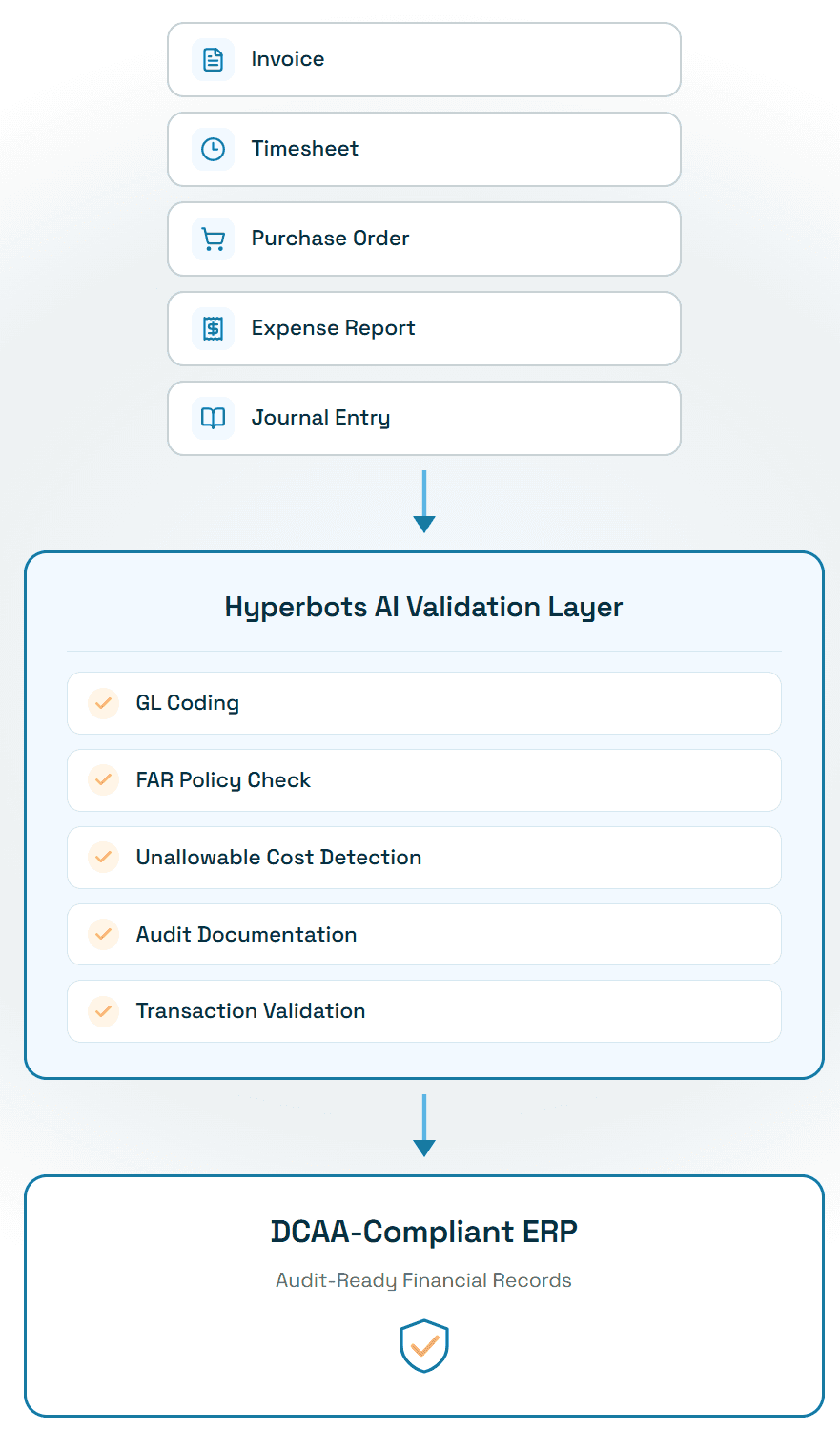

Where AI Fits: A Validation Layer, Not a Replacement

ERP systems were not built to make judgment calls about individual transactions before they post. They are systems of record, they store, calculate, and report based on whatever data is entered into them. Whether that data is correct, allowable, and properly classified has traditionally been a manual review problem, and manual review has a ceiling: it works when invoice volume is low and the reviewer is experienced, and it degrades as volume grows or turnover moves that judgment to someone less familiar with the contract structure.

Over the past few years, a category of AI-based validation tools has emerged specifically to sit upstream of the ERP, reviewing transactions like vendor invoices for GL coding accuracy, policy compliance, and cost classification before they post, rather than after a controller or auditor finds the error later. The premise isn't that AI replaces the ERP's role as system of record; it's that a validation step which used to depend entirely on a person's attention and available time can now catch a meaningful share of the same issues consistently, at higher volume, before the data becomes part of the permanent financial record.

Hyperbots is one example of this approach. It operates as an AI validation layer that reviews vendor invoices before they post to the ERP, checking for GL coding accuracy, policy compliance, and sales tax classification. It doesn't replace Costpoint, Unanet, Dynamics, or NetSuite as the system of record, it sits on top of them, with the goal of improving the quality and consistency of what actually reaches the ledger, which is the same thing a clean DCAA accounting system review is ultimately checking for.

For a government contractor finance team, the distinction is practical, not semantic: the ERP remains the authoritative ledger and the artifact an auditor examines, while a validation layer's job is to reduce how often a miscoded indirect cost, an unallowable expense, or a tax misclassification reaches that ledger in the first place.

Responsibility Split: ERP vs. AI Validation Layer

Function | ERP System of Record | AI Validation Layer |

Stores contract, project, and GL data | Yes | No |

Calculates indirect rates and cost pools | Yes | No |

Validates invoice GL coding before posting | Limited (manual review) | Yes |

Flags potentially unallowable costs pre-entry | Limited (manual review) | Yes |

Maintains the official audit trail | Yes | Supports it by improving source data quality |

Generates billing documents (vouchers, WAWF) | Yes | No |

Performs timekeeping approval workflows | Yes | No |

The practical effect is a cleaner handoff: data enters the ERP closer to audit-ready condition, which reduces the burden on controllers during incurred cost submissions and pre-award surveys.

Best Practices for Maintaining a DCAA-Compliant Environment

Finance leaders who consistently pass DCAA reviews tend to follow a similar set of disciplines, regardless of which ERP platform they use.

Document your accounting system in writing. A formal accounting policies and procedures manual, reviewed annually, is one of the first items a DCAA pre-award survey requests.

Reconcile indirect rates monthly, not just at year-end. Catching pool misclassifications early prevents large adjustments during the annual incurred cost submission.

Require daily timesheet entry with documented correction workflows. Any correction should show who made it, when, and why.

Maintain a clean, audit-friendly Chart of Accounts. A COA with redundant or ambiguous GL codes makes cost segregation harder to defend during audit, and the impact of GL coding accuracy on financial reporting and audits is well documented. For organizations on Deltek Costpoint specifically, getting the Costpoint Chart of Accounts coding scheme right early avoids costly remapping later.

Train AP and project accounting staff on FAR 31.2 unallowable cost categories. Awareness at the point of invoice entry catches more issues than after-the-fact review.

Run periodic internal mock audits. Simulating a DCAA floor check or incurred cost review surfaces gaps before an actual auditor does.

Treat audit trail completeness as a system design requirement, not an afterthought. Every transaction type, labor, materials, indirect allocations, should be traceable from source document to GL entry to billing.

Conclusion

A DCAA-compliant ERP is necessary but not sufficient on its own. The software provides the structure with job cost accounting, indirect rate calculation, timekeeping, and an audit trail but compliance ultimately depends on the discipline with which transactions are classified and validated before they become part of the permanent record. Whether you operate Costpoint, Unanet, Dynamics, or another platform, the contractors that pass audits consistently are the ones who treat data quality as a continuous process rather than a year-end scramble.

If your team is evaluating where transaction-level validation gaps might be putting audit readiness at risk, it's worth reviewing how AI-driven automation empowers CFOs to improve auditability through more consistent, explainable documentation as one input into a broader accounting system review, alongside your ERP platform decision itself. See how Hyperbots helps finance teams keep Costpoint data accurate, well-documented, and audit-ready - book a demo.

Frequently Asked Questions

Q1. Is there an official list of DCAA-approved ERP software?

No. The DCAA does not certify or approve specific software products. It evaluates whether a contractor's overall accounting system i.e. software combined with policies and internal controls meets the criteria in the Standard Form 1408 and DCAA Audit Manual.

Q2. What is the difference between a pre-award survey and an incurred cost audit?

A pre-award survey (SF1408) evaluates whether a contractor's accounting system is adequate before award of a cost-reimbursable contract. An incurred cost audit reviews actual costs billed against contracts after the fact, typically through the annual ICE submission required under FAR 52.216-7.

Q3. Can a small contractor use QuickBooks and still be DCAA compliant?

Generally yes, for very small contractors with limited contract complexity, provided timekeeping, job costing, and indirect rate calculation are properly configured through add-ons or manual controls. Most contractors outgrow this approach as contract volume and complexity increase.

Q4. What triggers a DCAA accounting system review?

Reviews are typically triggered by a contracting officer's request ahead of awarding a cost-reimbursable contract, by the size or risk profile of incurred cost submissions, or periodically for contractors with an active business systems oversight relationship.

Q5. How often should indirect rates be recalculated?

Provisional rates are typically set annually and trued up through the incurred cost submission, but leading practice is to reconcile indirect pools monthly so that variances are caught and corrected long before year-end.

Q6. Does AI automation replace the need for a DCAA-compliant ERP?

No. AI validation tools improve the accuracy and audit-readiness of data before it reaches the ERP, but the ERP remains the system of record that auditors examine. The two function as complementary layers, not substitutes for one another.

Q7. What is the biggest reason contractors fail DCAA accounting system reviews?

Timekeeping inconsistency is the most frequently cited finding, followed by inadequate segregation of unallowable costs and indirect cost pools that cannot be clearly traced back to source documentation.