What Breaks Across Procure-to-Pay and Order-to-Cash When Moving to SAP S/4HANA

Why core finance processes often slow down before they improve during S/4HANA transformation

Moving from SAP ECC to SAP S/4HANA is one of the most consequential decisions a finance organization can make. SAP has set 2027 as the mainstream maintenance deadline for ECC, meaning hundreds of thousands of companies are now in active migration planning. And yet, the conversation is still too often dominated by IT timelines, infrastructure costs, and licensing negotiations while the operational reality for the people who actually run Procure-to-Pay and Order-to-Cash workflows gets buried in slide decks.

This guide is for the finance controllers, AP leads, procurement managers, and CFOs who need an honest, granular answer to a simple question: what actually breaks?

What Fundamentally Changes in S/4HANA

The architecture shift you can't ignore

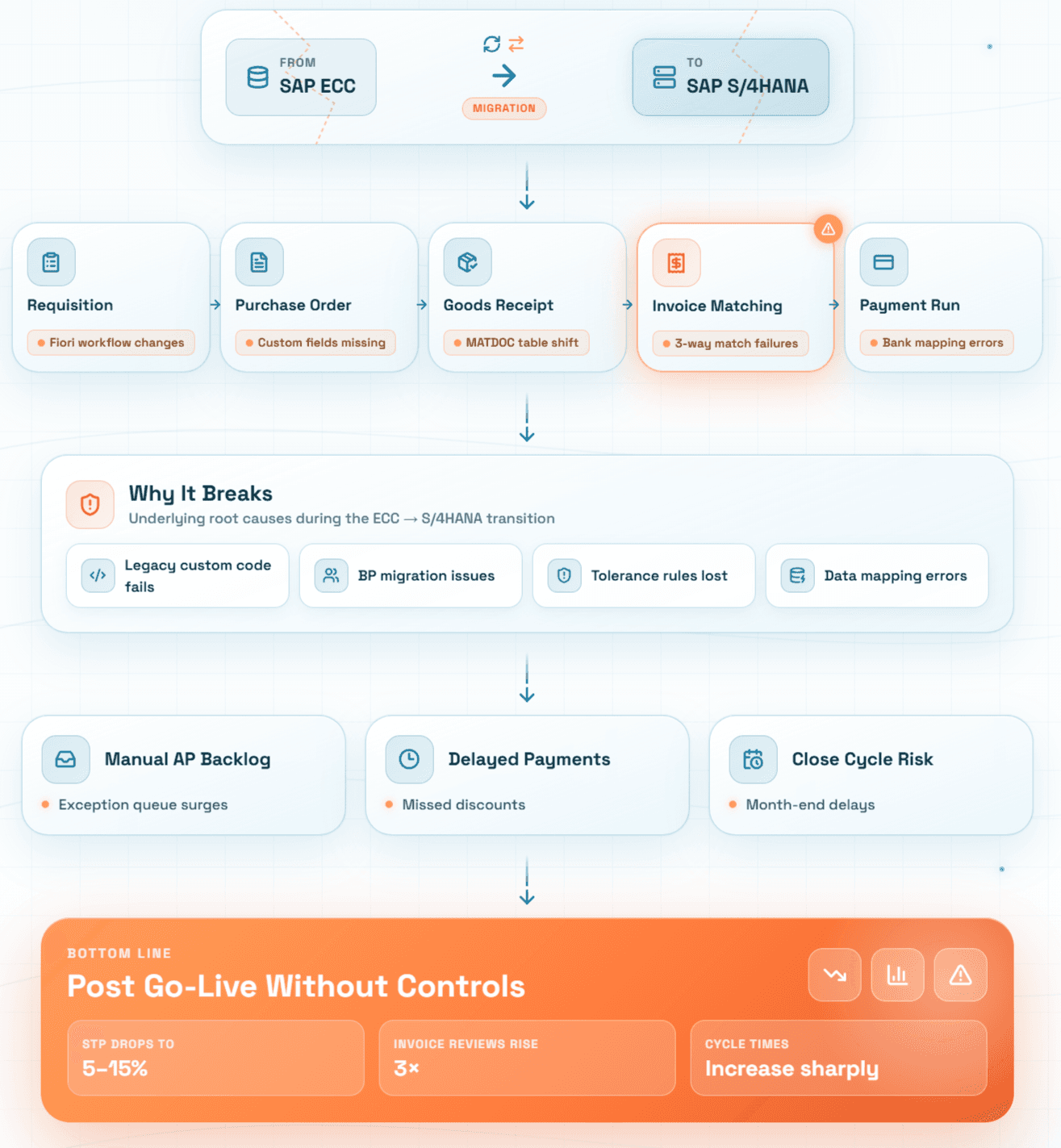

SAP S/4HANA is not an upgrade to ECC. It is a ground-up redesign built on the HANA in-memory database. Several core data models that ECC users have relied on for decades have been restructured or eliminated entirely. The most impactful change for finance teams is the universal journal (table ACDOCA), which consolidates what were previously separate tables like FI, CO, and Material Ledger, into a single line-item table.

For anyone who has customized ECC over years, this creates a fundamental compatibility problem: custom code, Z-programs, and third-party integrations that read or write to old table structures simply stop working. No warning, no graceful degradation, they fail.

Component | In ECC | In S/4HANA | Migration Risk |

Accounting tables | BKPF/BSEG (separate FI/CO) | ACDOCA (universal journal) | High |

Material ledger | Optional activation | Mandatory, always-on | High |

Inventory valuation | Moving average / standard | Actual costing mandatory | High |

Vendor/Customer master | LFA1 / KNA1 (separate) | Business Partner (BP) model | Medium |

Profit centers | EC-PCA (separate module) | Embedded in core FI | Medium |

Credit management | FI-AR-CR module | FSCM-CR (restructured) | Medium |

Purchasing info records | Separate ME1x transactions | Restructured, API-based | Low–Med |

Key insight: The ECC to S/4HANA finance impact is not just technical. It cascades into every manual process and every integration your team depends on, from how invoices are coded to how payment terms are stored.

The transition options and their trade-offs

Organizations typically choose between three paths:

Migration Path | Description | P2P/O2C Risk | Typical Timeline |

Greenfield | Implement S/4HANA from scratch; no legacy data ported | Very high; all integrations rebuilt | 18–36 months |

Brownfield (system conversion) | Convert existing ECC system to S/4HANA in-place | High; custom code breaks; data model changes | 12–24 months |

Selective data transition | Migrate selected processes; retain others in ECC temporarily | Medium; split-brain risk during transition | 18–30 months |

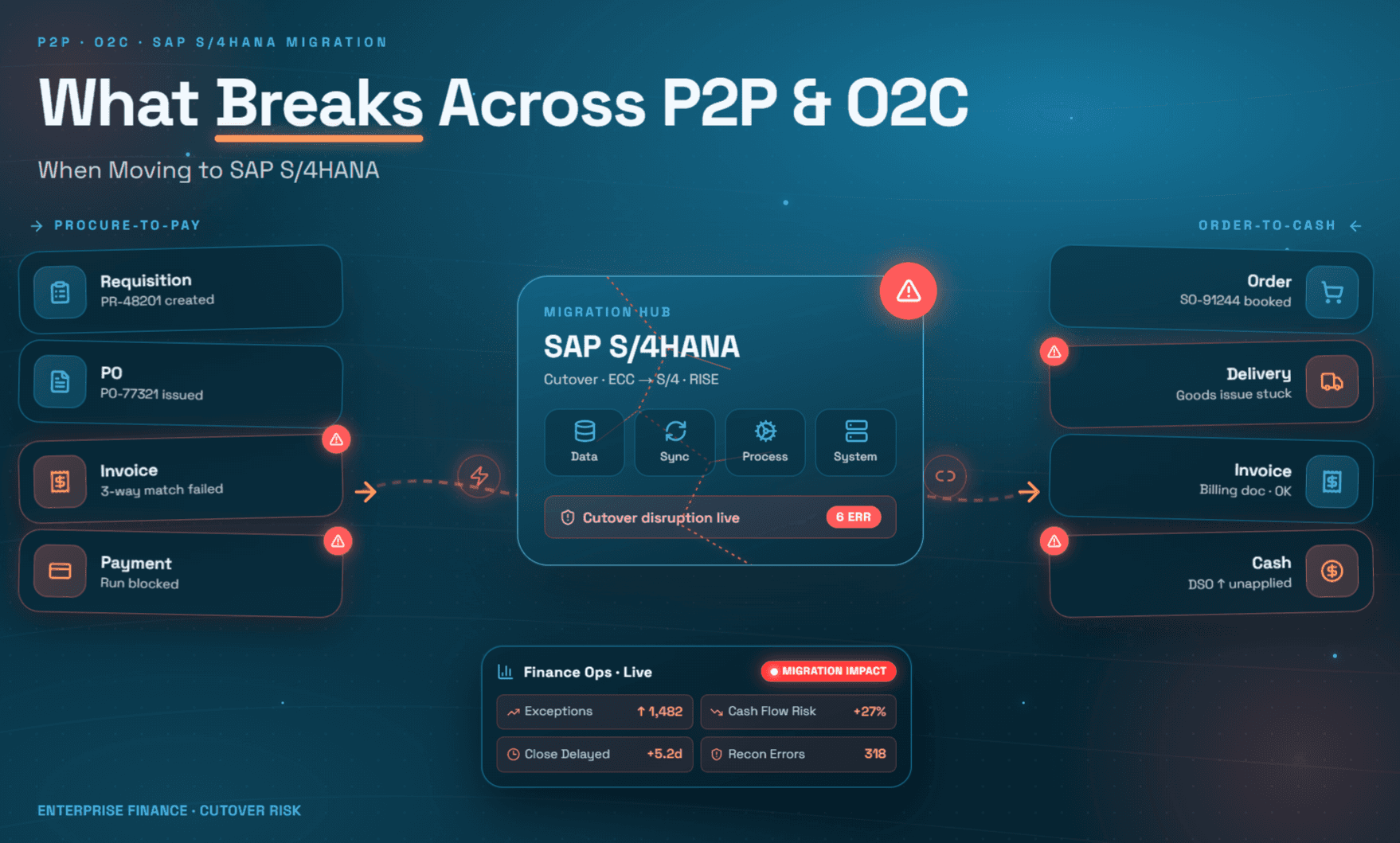

What Breaks in Procure-to-Pay (P2P)

The Procure-to-Pay process, from purchase requisition through vendor payment, is among the most integration-heavy workflows in any ERP. It touches vendor master data, inventory, GL coding, tax, approvals, and cash. Here is a systematic breakdown of where ECC to S/4HANA migration risks concentrate in P2P.

Purchase Requisition and Purchase Order creation

In ECC, the PR-to-PO handoff relied on a set of transaction codes (ME51N, ME21N) and approval workflows that were often extended through custom ABAP programs. In S/4HANA, many of these transactions have been replaced or restructured within the new SAP Fiori interface. Teams that automated PR drafting through non-standard screen exits find those exits no longer exist.

Specific failure points include:

Custom fields on purchase requisitions that were added via ECC screen variants, these must be rebuilt as Fiori extensions

Approval workflow rules hard-coded in ABAP (rather than configured via SAP Business Workflow) that do not survive the data migration

GL account determination logic that relied on old material master groupings, now affected by the new product master harmonization in S/4HANA

Blanket PO setups and matching strategies for blanket purchase orders that depended on old scheduling agreement structures

Invoice processing and 3-way matching

This is where ECC to S/4HANA migration risks are most acute. Three-way matching, reconciling the invoice against the PO and goods receipt, depends on the alignment of three separately managed data objects. In S/4HANA, the data structures underpinning POs (ME23N → now primarily managed in Fiori apps) and GRNs have changed. The result:

Failure Point | Root Cause | Operational Impact |

Tolerance rules on invoice matching disappear | FI settings not migrated correctly into new MIRO equivalent | All exceptions require manual approval; STP drops to near zero |

Custom invoice routing logic breaks | Workflow exit points removed in S/4HANA Fiori | Invoices stuck in queue; payment delays |

Historical GRN data inaccessible for match | MSEG table restructured into MATDOC in S/4HANA | Open POs from ECC cannot be matched against new-system invoices |

Parked invoices lost or corrupted | Document parking logic changed in universal journal context | Financial close impacted; duplicate payment risk |

Tax determination failures | TAXINJ / TAXINN condition routines not compatible | Incorrect tax posting; compliance exposure |

Why this matters for STP: Straight-through processing rates, the percentage of invoices that clear without human intervention, typically drop from 30–50% in mature ECC setups to single digits immediately after an S/4HANA go-live, because all the tolerance and routing rules that enabled automation have been disrupted. Recovery can take 12–18 months without deliberate remediation. See also: constraints on straight-through processing of invoices.

Vendor master data and onboarding

One of the most underestimated ECC to S/4HANA finance impacts is the Business Partner (BP) model. In ECC, vendors lived in table LFA1 and customers in KNA1. In S/4HANA, both are unified under the Business Partner object (using BUPA tables). This is not just a technical rename, it changes the entire vendor onboarding workflow, including how banking details, tax numbers, and payment terms are stored and validated.

Organizations that maintained vendor records across multiple company codes in ECC frequently discover duplicate BP records, missing bank data, and lost payment term assignments post-migration. The downstream effect is misdirected payments and broken early payment discount capture.

Payment processing

The payment run (F110 in ECC) has been replaced by a redesigned Fiori payment app in S/4HANA. Bank communication management (BCM) has also been restructured. Key breakage points:

Payment medium formats (DME Engine customizations) must be reconfigured

House bank assignments that were stored in company code configuration often lose their mapping

Early payment discount logic tied to payment term variants frequently fails if payment terms were set at the document level in ECC but are now expected at the BP level

Rationalized payment terms set up in ECC may not migrate cleanly to BP master records

GL coding and Chart of Accounts

The Chart of Accounts structure across ERPs changes meaningfully in S/4HANA. Secondary cost elements (used in CO) are abolished, they are now automatically derived from primary GL accounts. Cost center and profit center assignments are embedded in ACDOCA rather than separate CO line items. Any report or allocation that relied on secondary cost elements must be rebuilt. Custom GL coding rules in ABAP (substitution and validation exits) must be reviewed and migrated or replaced.

See: Chart of Accounts and GL coding for SAP for a detailed breakdown of what survives migration and what doesn't.

What Breaks in Order-to-Cash (O2C)

Order-to-Cash, from customer order entry through cash application, faces a different but equally serious set of migration risks. The O2C disruption is often underestimated because ECC-to-S/4HANA discussions tend to focus on the supply side. But AR, collections, and cash applications are profoundly affected.

Customer master and credit management

As with vendors, customers are migrated into the Business Partner model. The credit management module in ECC (FI-AR-CR) is replaced by SAP Financial Supply Chain Management Credit Management (FSCM-CM). This is a significantly different application:

Area | ECC Behavior | S/4HANA Behavior | Migration Risk |

Credit limit storage | Stored in FD32 per company code | Stored at BP level in FSCM, shared across company codes | High |

Credit check logic | Configured in SD credit control area | Restructured in FSCM rule-based engine | High |

Blocked orders | Released via VKM3/VKM4 | New Fiori apps; custom release rules must be rebuilt | Medium |

Customer payment history | Available directly in FD33 | Repointed to FSCM; reporting queries change | Medium |

Dunning configuration | Configured in company code settings | Migrates but custom dunning texts and exits often fail | Medium |

Accounts Receivable and collections

Collections in ECC were typically managed through custom aging reports and manual follow-up workflows. SAP Collections Management in S/4HANA (via FSCM) is a purpose-built module but it requires active setup and data load. Organizations that relied on custom ABAP aging queries find that the underlying table structures (BSID, BSAD) have changed in how they relate to ACDOCA, breaking those reports entirely at go-live.

The practical impact: collection teams lose visibility into outstanding receivables during cutover. Days Sales Outstanding (DSO) typically rises 15–30% in the months immediately following go-live as collection workflows are rebuilt.

Cash application

Cash application, matching incoming bank payments to open receivables, is among the most disrupted O2C processes in an S/4HANA migration. In ECC, many organizations used the Electronic Bank Statement (EBS) processing in FI-BL, often heavily customized. In S/4HANA, this is replaced by Multi-Bank Connectivity (MBC) and a new bank statement monitor. Custom interpretation algorithms for payment advice parsing must be rebuilt from scratch.

The result is a sharp increase in unmatched payments sitting in suspense accounts, requiring manual intervention to clear. For high-volume businesses, this can mean thousands of uncleared items per week immediately after go-live.

Revenue recognition

If your organization is on IFRS 15 or ASC 606, S/4HANA introduces Revenue Accounting and Reporting (RAR), which replaces the old SD revenue recognition module. This is a near-complete rebuild. Custom billing rules, milestone billing setups, and deferred revenue schedules all need to be re-implemented and tested. The GL impact can be significant: revenue that was recognized on billing in ECC may be deferred in S/4HANA RAR until performance obligations are confirmed.

Data Migration: The Silent Killer

Most ECC to S/4HANA migration risks discussions focus on process and code changes. But data migration is often the single largest cause of post-go-live failures in P2P and O2C. Here is what actually goes wrong:

Data Category | Common Migration Failure | P2P or O2C Impact |

Open purchase orders | Line items with partial GRNs fail to migrate with correct commitment values | P2P: 3-way match fails on all in-flight POs at go-live |

Vendor bank details | IBAN/BIC format validation rejects legacy formatted records | P2P: Payment runs fail for affected vendors |

Open invoices (parked/posted) | Document number ranges collide; some parked documents lost | P2P: Duplicate payment risk; audit trail broken |

Customer open items | BSID/BSAD records don't map cleanly to ACDOCA without delta migration | O2C: Collections team loses AR visibility |

Payment terms (customer/vendor) | Terms stored at document level in ECC not migrated to BP master | Both: Discount capture fails; incorrect due dates |

Tax condition records | Condition tables restructured; records must be remapped | P2P: Tax misposting on all migrated invoices |

GL historical balances | Secondary cost element balances not migrated (they no longer exist) | P2P/O2C: Management reporting comparisons broken for 12+ months |

Best practice: Run a parallel data quality audit 6 months before cutover. Use automated reconciliation to identify every vendor record missing a Business Partner assignment, every open PO with a GRN discrepancy, and every customer record with missing credit terms. Remediating data before migration is 10x cheaper than fixing it after go-live.

Top Migration Mistakes Finance Teams Make

No. | Mistake | Why It Happens | Consequence |

1 | Treating migration as an IT project, not a finance project | Finance teams not included in design workshops | Approval workflows and COA rebuilt without finance input |

2 | Not testing with real transaction volumes | UAT done with clean sample data | Match failures and tolerance errors only discovered at go-live |

3 | Assuming custom code will be migrated | SI says "we'll handle it" | Dozens of Z-programs fail silently; no fallback |

4 | Forgetting third-party integrations | AP automation, e-invoicing, and banking platforms not in scope | Invoice feed and payment file integrations break at cutover |

5 | No cutover playbook for in-flight transactions | Cutover planning focused on system, not business process | Open POs, unposted invoices, and unmatched payments pile up |

6 | Underestimating Business Partner migration effort | Vendor/Customer BP conversion treated as a one-click migration tool | Missing bank data, broken payment terms, duplicate records |

7 | No post-go-live hypercare for P2P and O2C | Budget exhausted by implementation | Finance team overwhelmed; manual backlog builds for months |

For a deeper look at the process layer, see: the evolution of the P2P process and why each layer must be explicitly validated before and after cutover.

Industry-Specific Impact

The severity of P2P and O2C disruption during an S/4HANA migration varies significantly by industry. Here is a summary of the most acute impact areas by sector:

Industry | Highest-Risk P2P Area | Highest-Risk O2C Area | Learn More |

Manufacturing | MRP-driven PO generation; inventory valuation changes | Revenue recognition on delivery milestones | |

Retail | High-volume invoice matching; vendor deductions | Returns processing; credit note reconciliation | |

Professional services | Time & material PO matching; subcontractor invoices | Milestone billing; IFRS 15 compliance | |

Healthcare | Regulated vendor onboarding; formulary POs | Insurance AR; payer reconciliation | |

Distribution/Wholesale | EDI-based PO processing; blanket orders | High-volume cash application; deduction management |

For manufacturing specifically, the combination of mandatory actual costing, MRP-generated PO restructuring, and multi-plant inventory valuation changes makes the ERP migration challenge particularly acute.

How Hyperbots AI Co-Pilots Protect P2P and O2C During and After S/4HANA Migration

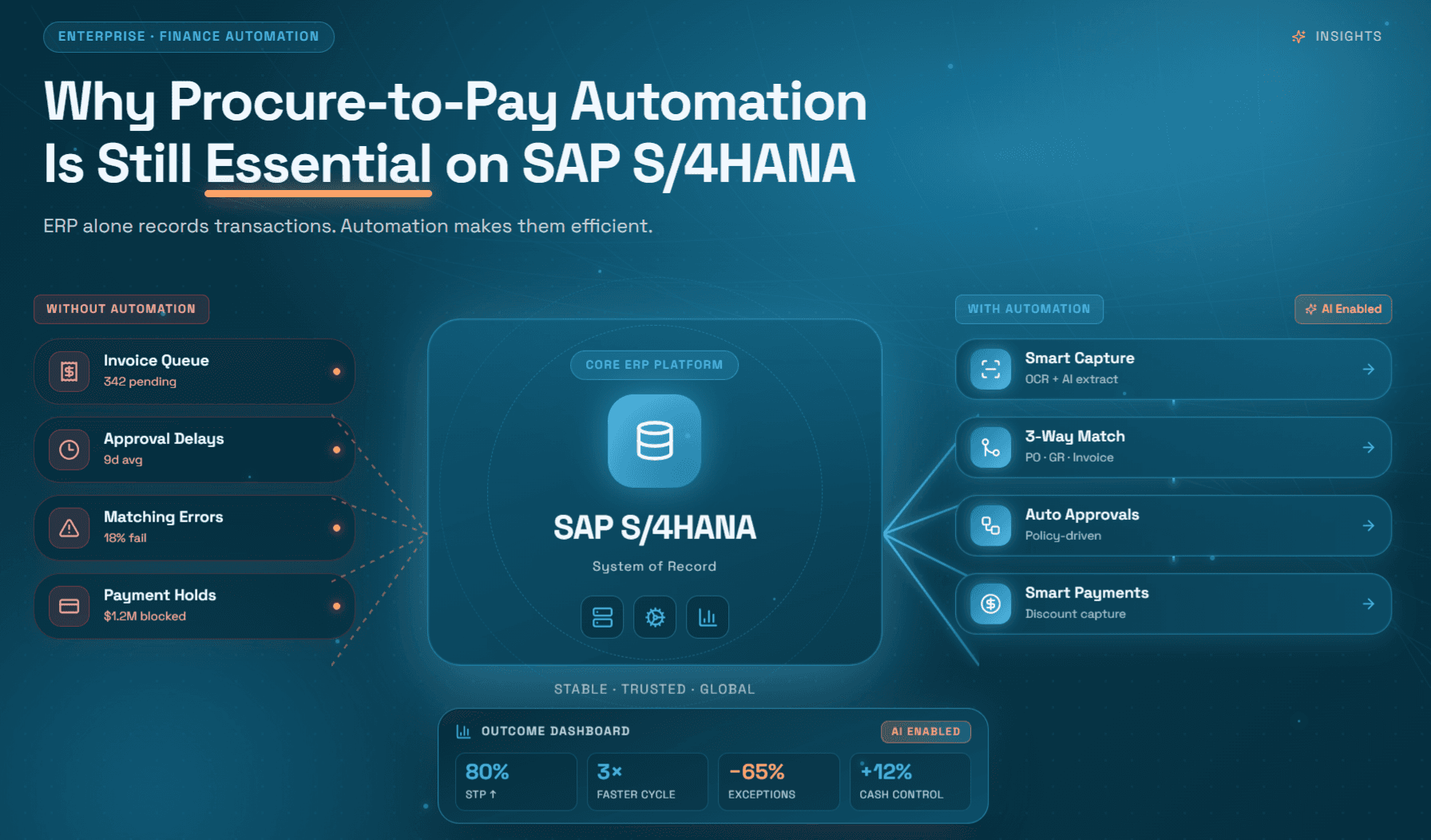

SAP S/4HANA is a powerful platform but it is not a finance automation platform. It is an ERP that records transactions. The intelligence needed to process invoices at 99.8% accuracy, route approvals based on policy, capture early payment discounts, and apply cash automatically lives outside the ERP. That is exactly where Hyperbots operates.

Hyperbots deploys as an AI layer on top of S/4HANA (or any ERP), connecting through pre-built integrations that do not depend on the legacy table structures that break during migration. This means Hyperbots can go live independently of your cutover date and hence, protecting operational continuity while the ERP transitions beneath it.

P2P Co-Pilots

Invoice Processing Co-Pilot

Captures invoices from email, portals, and EDI. Extracts every field with 99.8% accuracy using AI trained on finance documents, not templates. Performs 2-way and 3-way matching, GL coding, and routes exceptions. When your S/4HANA tolerance rules are being rebuilt post-migration, this co-pilot maintains straight-through processing independently. Customers like Extreme Reach have achieved 80% STP and 99.8% accuracy with zero manual touch-ups.

Procurement Co-Pilot

Automates the full PR-to-PO lifecycle. During S/4HANA migration, when Fiori approval workflows are being configured, the Procurement Co-Pilot maintains policy-driven approval routing, budget validation, and PO dispatch and thus, reducing the procurement cycle from 3 days to 4 hours. It handles the gaps that exist between go-live and full Fiori stabilization.

Vendor Management Co-Pilot

Manages vendor onboarding, identity verification, and master data validation. Directly addresses the Business Partner migration risk: the co-pilot validates bank details, tax IDs, and payment terms during and after migration, ensuring vendor records are clean before they hit the new ERP. Vendor onboarding that previously took weeks can be completed in hours.

Payments Co-Pilot

Makes intelligent payment timing decisions based on discount windows, cash position, and vendor relationship data. During migration, when payment medium formats and house bank assignments are being reconfigured, the Payments Co-Pilot maintains payment schedule continuity, preventing missed discounts and late payment penalties. Manages ACH, check, wire, and virtual card payments.

Sales Tax Verification Co-Pilot

One of the most acute S/4HANA migration risks is broken tax condition records. The Sales Tax Verification Co-Pilot validates tax rates, nexus applicability, and line-item categorization on every invoice, independent of the ERP's condition record state. A CFO using this co-pilot identified and eliminated $200,000 in tax leakage that had gone undetected in their ECC environment.

Accruals Co-Pilot

Automates accrual discovery for goods received, services rendered, and recurring expenses even when no PO exists. During S/4HANA cutover, when the period-end close process is under the most stress, the Accruals Co-Pilot maintains accurate unbilled liability capture, automated journal entry booking, and configurable reversal, reducing month-end close time significantly.

O2C Co-Pilots

Collections Co-Pilot

Automates overdue invoice follow-up, dispute routing, and customer communication. Directly addresses the DSO spike that accompanies every S/4HANA go-live: when the FSCM collections module is being configured and AR visibility is disrupted, the Collections Co-Pilot maintains outreach cadence and dispute tracking, preventing the receivables backlog from compounding. AI-driven prioritization ensures high-value accounts receive attention first.

Cash Application Co-Pilot

Matches incoming payments to open invoices automatically across ACH, wire, check, and virtual card remittances. This directly solves the cash application breakdown that occurs when ECC bank statement interpretation routines are replaced by S/4HANA's MBC. The co-pilot operates independently of the ERP's bank statement processing, maintaining match rates and preventing suspense account backlog during cutover.

Platform capabilities that create transformational impact

Beyond individual co-pilots, Hyperbots' platform provides capabilities that make the migration window manageable:

Capability | What it means in practice |

Pre-trained, ready-to-deploy models | No months of training data needed. Co-pilots go live in days, not months which is highly critical when migration timelines are already stretched. See: how pre-trained AI co-pilots transform finance fast |

ERP-agnostic connectivity | Connects to S/4HANA, ECC, and any intermediate state including selective data transition environments where both systems run in parallel |

Policy-driven AI | Company-specific approval rules, GL coding logic, and matching tolerances are configured in the co-pilot, not hard-coded in ABAP. These survive the ERP migration entirely. See: policy-driven AI and 80% productivity gains |

Unlimited-user licensing | No per-seat cost means the full finance team can use co-pilots during hypercare without budget shock. See: unlimited access model |

Self-learning AI | Accuracy improves over time through feedback loops so the co-pilots get better as your S/4HANA environment stabilizes |

Multi-agent collaboration | Co-pilots work together across P2P and O2C, a payment co-pilot can reference vendor relationship data managed by the vendor management co-pilot. See: multi-agent collaboration in finance |

ROI: What AI-Led Continuity Actually Delivers

The cost of P2P and O2C disruption during an S/4HANA migration is rarely quantified in project business cases. Here is a framework for understanding it and what Hyperbots delivers in measurable terms.

Metric | Typical Post-Go-Live Without AI Layer | With Hyperbots AI Co-Pilots |

Invoice straight-through processing rate | 5–15% (down from pre-migration 30–50%) | 80%+ maintained throughout migration |

Invoice processing accuracy | Highly variable; match failures surge | 99.8% accuracy |

PR-to-PO cycle time | 3–7 days (manual fallback during disruption) | 4 hours |

Days Sales Outstanding (DSO) | +15–30% in first 3–6 months post-go-live | 40% reduction in DSO; collections continuity preserved |

Manual invoice review volume | Surges 3–5x during hypercare period | 80% reduction in manual reviews vs. baseline |

Early payment discount capture rate | Drops significantly as payment timing is disrupted | AI-driven recommendations maintain capture rate |

Tax leakage exposure | Increases as tax condition records break in migration | Automated verification catches errors; one CFO recovered $200K |

Operations cost reduction | Cost typically rises during migration hypercare | Up to 80% reduction in P2P operations costs |

For a tailored estimate of what AI co-pilots would deliver for your organization, Hyperbots provides dedicated ROI calculators for invoice processing, procurement, payments, and collections.

To see what Hyperbots looks like in practice for your ERP environment, request a personalized demo or start a free trial.

Frequently Asked Questions

Q1. What is the biggest P2P risk when migrating from ECC to S/4HANA?

The most operationally acute risk is invoice matching failure. In S/4HANA, the goods receipt table (MSEG) is restructured into MATDOC, and the universal journal (ACDOCA) consolidates FI and CO postings. Any custom tolerance rules, tax conditions, or workflow exits built in ECC must be rebuilt. Until they are, virtually all invoices with exceptions require manual intervention which can paralyze a high-volume AP team. See: how AI solves 3-way matching challenges.

Q2. Does the Business Partner migration actually break payment runs?

Yes, frequently. In ECC, vendor bank details were stored under the LFA1/LFBK tables at the vendor level. In S/4HANA, these are stored under the Business Partner model in BUPA-linked bank tables. If the migration tool fails to map IBAN/BIC formats correctly, which is common with legacy-formatted data, payment runs will reject affected vendors. The result is manual payment processing until records are corrected, with associated fraud risk during the unstructured remediation period.

Q3. How long does it take for P2P to stabilize after an S/4HANA go-live?

Without deliberate AI-layer protection, 12 to 18 months is a realistic stabilization timeline for complex ECC environments. With an AI co-pilot layer like Hyperbots operating independently of the ERP, stabilization can be achieved in weeks rather than months, because the co-pilots maintain process continuity while the ERP is being tuned. For a benchmarked view of fast deployment timelines, Hyperbots customers typically go live in days.

Q4. What happens to open purchase orders at S/4HANA cutover?

Open POs are migrated using the Migration Cockpit (LTMC), but partial GRNs, special stock indicators, and custom fields often cause line items to arrive in an incorrect state. The safest approach is to close as many open POs as operationally possible before cutover, and to have a dedicated data cleansing workstream for in-flight commitments. Any PO that cannot be closed must be manually validated post-migration before invoices can be matched against it.

Q5. Does Order-to-Cash require as much migration attention as P2P?

Yes and it is often given less attention because the symptoms are slower to emerge. Collections performance degrades gradually as AR visibility is lost; DSO rises over weeks, not on day one. Cash application failures like unmatched payments in suspense, accumulate quietly. Organizations that invest in O2C continuity tools before go-live avoid the receivables backlog that typically takes 6+ months to clear manually.

Q6. Can Hyperbots co-pilots work during a selective data transition (where ECC and S/4HANA run in parallel)?

Yes. Hyperbots is ERP-agnostic and connects via pre-built integrations that do not depend on specific ECC or S/4HANA table structures. It can process invoices and route approvals against both systems simultaneously, essential during selective data transitions where some company codes are on S/4HANA while others remain on ECC. See: faster onboarding with Hyperbots ERP integration.

Q7. What is the ECC to S/4HANA finance impact on GL coding and Chart of Accounts?

Significant. Secondary cost elements are abolished. Profit center accounting is embedded in the universal journal. Any ABAP substitution or validation exits on GL posting must be rebuilt. Organizations with complex cost center hierarchies should expect substantial FI/CO configuration work. Hyperbots' GL coding AI handles account determination independently of the ERP's condition configuration, maintaining coding accuracy during the transition period. See also: GL coding for SAP.