Why ERP Modernization Is Not the Same as Finance Automation

Why Upgrading Your ERP Doesn’t Eliminate Manual Finance Work

Every CFO who has led an ERP migration remembers the promise. Faster close cycles. Better visibility. Fewer manual errors. And then, a year after go-live, the reality sets in: the AP team is still manually keying invoices. Month-end accruals are still driven by spreadsheets. Purchase requisitions are still sitting in someone's inbox waiting for approval. The ERP is live and functioning, but the finance operations are still deeply manual.

This is the central confusion at the heart of modern finance transformation: ERP modernization and finance automation are not the same thing. They address different problems, operate at different layers, and deliver different outcomes. Conflating them is one of the most expensive strategic mistakes a finance organization can make and it happens constantly.

This article unpacks that distinction in full. We will explore what ERP systems actually do, what they cannot do, why finance automation exists as a separate and complementary layer, and how organizations can build the kind of intelligent, truly automated finance function that closes the gap between what ERPs promise and what finance teams actually need.

What ERP Modernization Actually Means

ERP was born from a simple idea: unify the data and processes of a business into a single system of record. When SAP introduced its R/2 system in the 1970s, and later R/3 in the early 1990s, the goal was integration. Manufacturing, procurement, finance, HR, and logistics could share a common database, eliminating silos and reducing the inconsistencies that came from running separate departmental systems.

For decades, ERP modernization has meant moving from older, on-premise instances to newer versions usually something like migrating from SAP ECC to SAP S/4HANA, upgrading Oracle E-Business Suite to Oracle Cloud ERP, or moving from a legacy on-premise NetSuite setup to a modern cloud instance. More recently, mid-market companies have migrated from desktop accounting tools like QuickBooks to cloud ERP platforms like Oracle NetSuite, or from Microsoft Dynamics GP to Microsoft Dynamics 365 Business Central.

When companies "modernize" their ERP, they are typically doing some combination of the following:

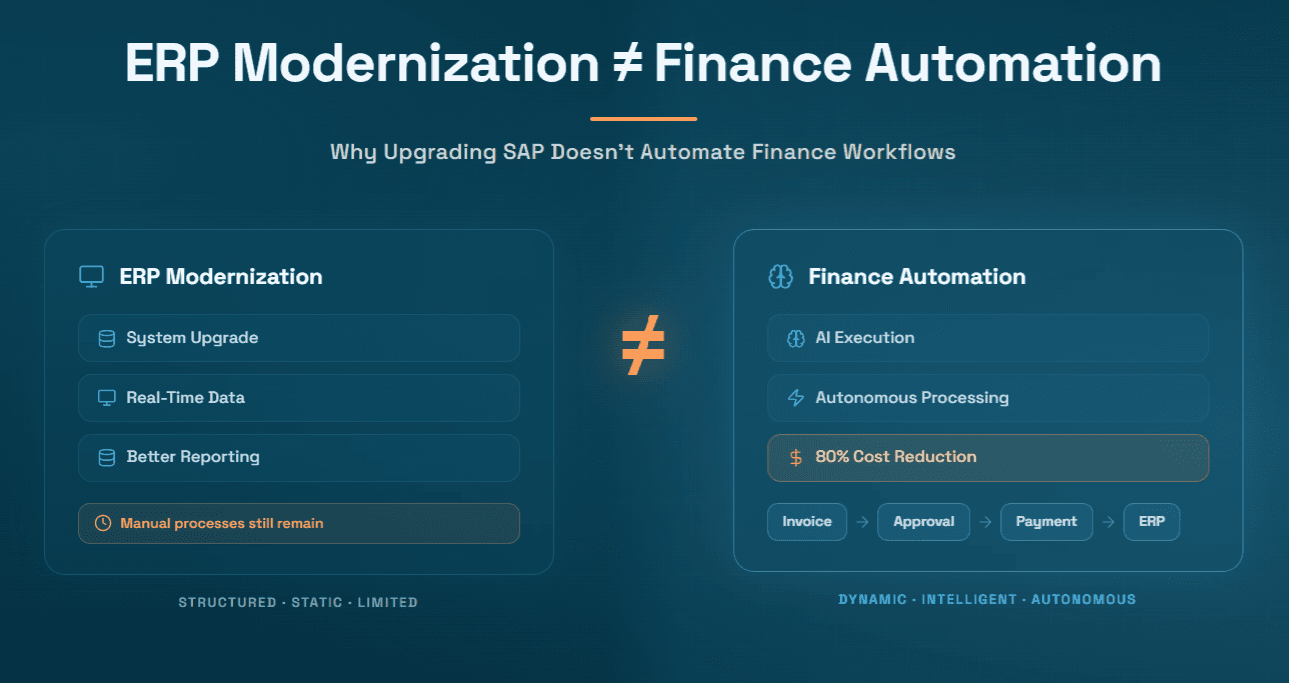

Moving from on-premise infrastructure to cloud hosting, which reduces hardware costs and IT maintenance burden. Upgrading to a new version of the ERP that supports better reporting, newer interfaces, and improved API capabilities. Consolidating multiple legacy systems into a single, modern ERP to reduce integration complexity. Extending the ERP with modules, adding procurement modules, treasury modules, or FP&A tools that sit within the same platform ecosystem.

All of this has real value. Cloud ERPs are more scalable, more accessible to remote teams, and generally easier to maintain. A modern ERP gives finance teams better dashboards, better drill-down capabilities, and real-time data that was simply unavailable in older systems.

But here is the critical point: none of this makes finance operations automatic.

The Fundamental Limits of ERP Systems

ERP systems are designed to be systems of record, they store, organize, and surface data. They are not designed to be autonomous agents that act on that data. This distinction is subtle but profound.

Consider what happens when a vendor invoice arrives. In a modern cloud ERP, whether it is NetSuite, SAP S/4HANA, Microsoft Dynamics, or SAP Business One, the process typically looks like this: someone receives the invoice by email, downloads the PDF, opens the ERP, navigates to the AP module, manually enters the invoice header fields, manually keys the line items, assigns GL codes, routes it for approval, and eventually posts it. The ERP records everything faithfully. But the human did all the actual work.

The ERP's job is to hold the truth, the vendor master, the chart of accounts, the purchase orders, the general ledger. It is not designed to read an invoice, understand its content, match it to a PO, validate the tax, assign the GL codes, and route it for approval without human intervention. That is a fundamentally different kind of intelligence.

This gap becomes even more visible across several key finance processes.

Accruals: Every ERP allows users to post manual journal entries for accruals. But the ERP will not go looking for unbilled liabilities, calculate what is owed for services received but not invoiced, or automatically reverse those entries in the next period. A modern ERP might have tools to assist with accruals, but the discovery, calculation, and booking logic is almost entirely manual. Read more on how accruals remain a challenge in AP →

Purchase Requisitions and POs: ERPs have procurement modules, but they require humans to initiate requisitions, fill in required fields, select vendors, and route approvals. The system records and enforces policies, but it does not autonomously create or manage the procurement process. Understanding the PR to PO lifecycle →

Vendor Management: ERPs maintain vendor master data, but onboarding a new vendor involves collecting W-9s, verifying identity, checking for OFAC compliance, setting payment terms and it’s still primarily a manual process that the ERP records rather than drives. Vendor onboarding challenges →

Payment Decisions: ERPs process payments, but they do not think about payment timing. Should you pay early to capture a 2/10 Net 30 discount? Should you delay payment to preserve cash? The ERP has no opinion. It disburses what you tell it to disburse.

Sales Tax Verification: Modern ERPs can store tax rates, but automatically validating whether the tax on a vendor invoice is correct, checking the line-item categorization, the origin and destination addresses, the applicable jurisdiction rates, is beyond the scope of what an ERP does natively. Sales tax compliance complexity →

The pattern is consistent: ERPs are passive record-keepers, not active process drivers. They respond to instructions; they do not generate them.

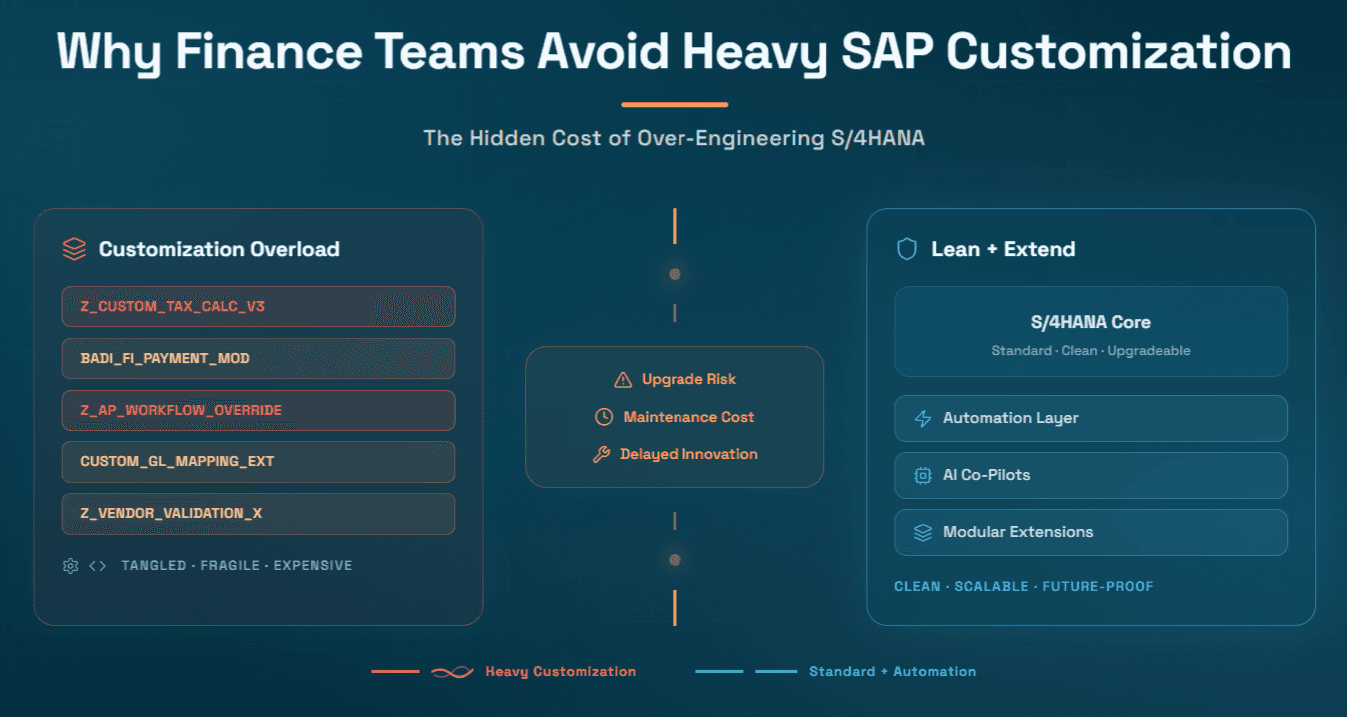

The Difference Is Not Features - It Is Intelligence

One objection that often arises is that modern ERPs do have automation features. SAP has workflow tools. Oracle NetSuite has SuiteFlow. Microsoft Dynamics has Power Automate integrations. Are those not automation?

They are but they are rules-based automation, and that distinction matters enormously.

Rules-based automation is the ability to say: "If invoice amount is under $500 and vendor is on the approved list, auto-approve." These workflows are valuable for structured, predictable processes. But the moment you encounter an exception, a vendor invoice with a missing PO number, a line item that doesn't match the goods receipt, an invoice in a non-standard format from a new vendor, the rule breaks down and a human has to intervene.

Real-world finance processes are dominated by exceptions. Industry data consistently shows that between 20% and 40% of invoices have some kind of discrepancy, mismatched amounts, incorrect tax, missing fields, layout variations that confuse extraction tools. Rules-based automation handles the easy 60%. It fails on the important 40%.

True finance automation requires judgment, the ability to understand context, apply company-specific policy, reason through discrepancies, and take appropriate action even on transactions that have never been seen before. That is the territory of AI, not workflow rules.

This is why the evolution from rules-based automation to AI-native reasoning is the defining shift in finance platforms today. ERP modernization upgrades the system of record. Finance automation, real finance automation, replaces judgment-intensive manual work with AI that can think.

Why Finance Teams Keep Discovering This the Hard Way

If the distinction is clear in theory, why do so many organizations discover it only after a costly ERP implementation?

There are a few reasons.

ERP vendors sell the promise of transformation, and the language of their marketing often implies automation that does not exist in practice. A "fully integrated cloud ERP" sounds like it handles everything. But integration is not automation. Having all your data in one place is very different from having that data acted upon intelligently.

Implementation partners, who earn fees based on ERP configuration complexity, are also not incentivized to point out where the ERP falls short. The conversation about automation gaps often only happens post-go-live, when the finance team realizes that the headcount reduction they expected has not materialized.

There is also a legitimate confusion about where the ERP's job ends and the automation layer's job begins. This boundary has shifted significantly with the emergence of AI-native platforms that sit on top of ERPs and fill the intelligence gap.

The evolution of finance automation from OCR to AI →

The Layers of Modern Finance Platforms

To understand the right way to think about this, it helps to map the layers of a modern finance platform architecture.

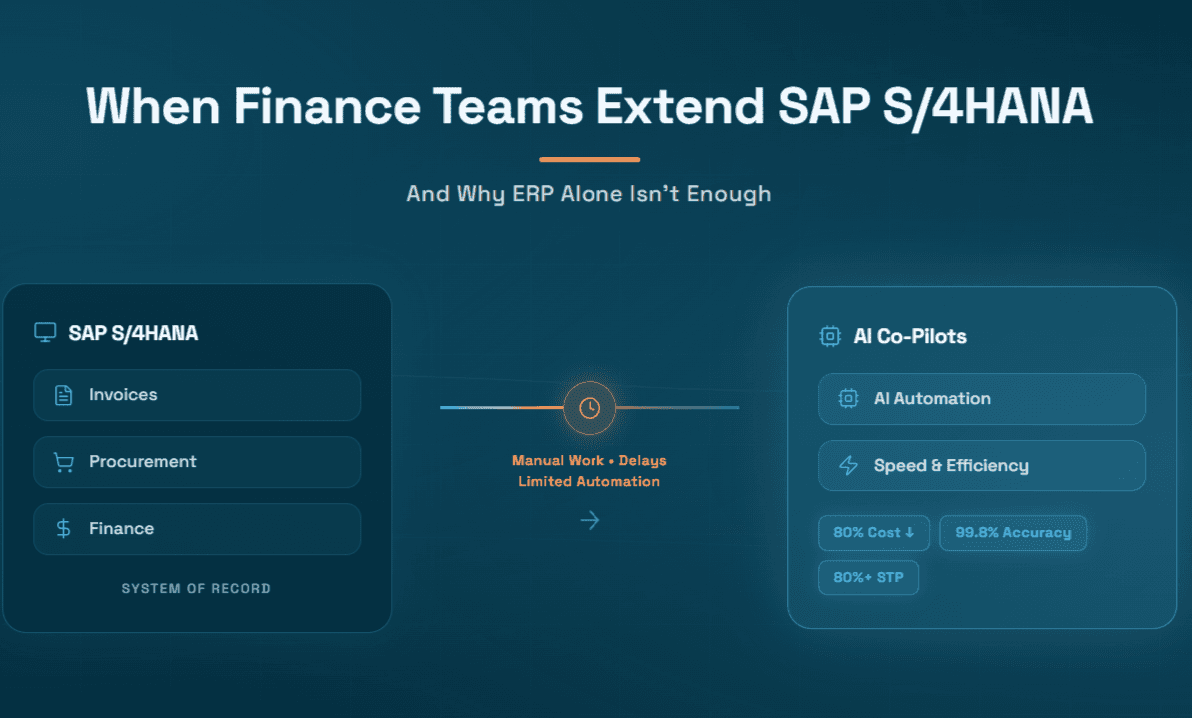

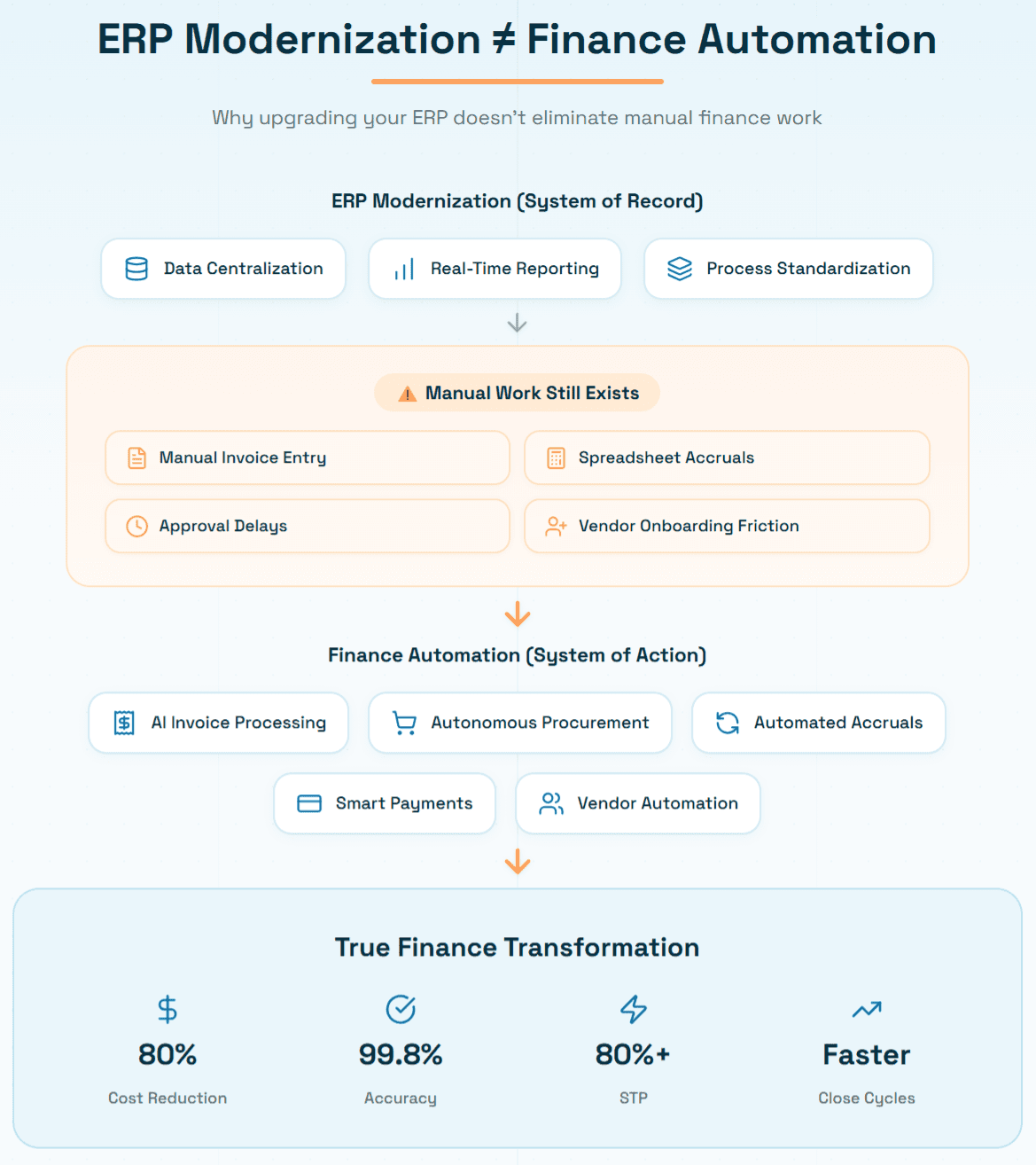

Layer 1: The ERP (System of Record) This is where financial truth lives. The chart of accounts, the general ledger, vendor master, purchase orders, payment history. The ERP is the authoritative source and should remain so. When you modernize the ERP, you are improving this layer, better UI, cloud scalability, more modules, better APIs.

Layer 2: Finance Automation (System of Action) This is where intelligence lives. AI co-pilots and automation platforms connect to the ERP, read its data, process incoming documents, apply policy, execute workflows, and write results back. This layer handles invoice processing, procurement automation, accruals, tax verification, payment decisions, and vendor management. It is the layer that actually reduces manual work.

Layer 3: Analytics and Reporting (System of Insight) This is where BI tools, FP&A platforms, and CFO dashboards live. They read data from the ERP and present it for decision-making. Tools like Tableau, Anaplan, or Adaptive Insights operate here.

Most ERP modernization initiatives invest heavily in Layer 1 and sometimes Layer 3. Layer 2 or the automation layer, is chronically underinvested, and it is precisely Layer 2 that determines how much manual work the finance team actually has to do.

How AI complements ERP systems rather than replacing them →

The Cost of Conflating the Two

The financial and operational costs of treating ERP modernization as a substitute for finance automation are significant and well-documented.

Direct labor costs remain elevated. AP teams that were expected to shrink after an ERP implementation often stay the same size or grow, because the volume of manual processing work has not decreased. The ERP just moved the manual work to a new interface.

Error rates remain high. Manual data entry is manual data entry, regardless of whether it happens in a legacy system or a modern cloud ERP. Duplicate payments, incorrect GL codes, missed early payment discounts, and tax compliance errors persist.

Month-end close remains slow. If accruals are still being assembled manually in spreadsheets, if GL coding is still being reviewed line by line, if invoice queues are still being processed by hand—the close cycle will not improve meaningfully, regardless of how good the ERP's reporting module is.

Straight-through processing (STP) rates stay low. Industry benchmarks suggest that most organizations without dedicated AI automation achieve STP rates of 30–50% for invoice processing. That means more than half of all invoices require some form of human intervention. An ERP upgrade alone does nothing to improve that number.

What constrains straight-through processing →

What Real Finance Automation Looks Like

Real finance automation is not about moving data around faster. It is about removing the humans from the loop on tasks where human judgment adds no value, and surfacing exceptions to humans only when genuine judgment is required.

The most sophisticated implementations of finance automation today operate on an agentic model, where AI agents autonomously handle entire process segments end-to-end, coordinating with each other and with ERP systems, and escalating only when policy thresholds or confidence limits are reached.

Multi-agent collaboration in finance and accounting →

Let us walk through what best-in-class automation looks like across the core finance processes.

Invoice Processing: An AI agent monitors email inboxes, vendor portals, and ERP queues for incoming invoices. It extracts all header and line-item data with near-perfect accuracy regardless of invoice format or layout. It validates the data against POs and goods receipts, applies matching tolerances, verifies sales tax, assigns GL codes, and routes exceptions for human review. Compliant invoices flow straight through to posting without any human touch. Target STP rate: 80%+.

Procurement (PR to PO): AI agents capture purchase requests from emails, forms, or chat interfaces. They validate against budget, check for duplicate requests, complete missing fields using vendor master and historical data, route for approval based on policy, and automatically generate and dispatch POs to vendors. The PR to PO cycle that once took three days can be compressed to under four hours.

Accruals: At period-end, AI agents scan the ERP for goods received but not invoiced, services delivered under open contracts, and recurring expenses without a corresponding PO. They calculate accrual amounts, book journal entries, and schedule reversals—without a single spreadsheet or manual calculation.

Payment Management: AI agents analyze the full payment queue, identify early payment discount opportunities, flag invoices approaching late fees, model cash flow implications of different payment timing scenarios, and recommend optimal disbursement schedules. Payments are batched, approved through workflow, and posted to the ERP automatically.

Vendor Management: Onboarding a new vendor triggers an automated workflow: document collection via a self-service portal, identity verification, OFAC screening, W-9 validation, and master data creation in the ERP. No email chasing, no manual data entry.

Sales Tax Verification: Every invoice line item is evaluated against tax dictionaries, jurisdiction rules, origin and destination addresses, and economic nexus thresholds. Incorrectly charged tax is flagged for dispute before payment is made. CFO case study: $200K in tax leakage eliminated →

ERP Modernization and Finance Automation: How They Work Together

The most important insight is that these are not competing strategies, they are complementary ones. The question is not "ERP upgrade or finance automation?" It is "ERP upgrade first, then finance automation" or "ERP upgrade alongside finance automation."

A modern ERP provides better APIs, cleaner data structures, and more reliable master data, all of which make the finance automation layer more effective. An AI co-pilot working on top of SAP S/4HANA has better data to work with than one working on top of a legacy on-premise system. ERP modernization lowers the technical debt that the automation layer has to deal with.

Conversely, finance automation makes ERP investments more valuable. A NetSuite instance with AI-driven invoice processing, automated accruals, and intelligent payment management delivers dramatically better ROI than one where all those processes remain manual. The ERP becomes a true system of record for a finance function that is actually automated rather than a system of record for a finance function that is still largely manual.

Advancing Oracle NetSuite operations with AI co-pilots →

The organizations that win in the next five years will be those that invest in both layers deliberately, with a clear understanding of what each layer does and does not provide.

Industry Dimensions: Automation Needs Vary by Sector

The gap between ERP capabilities and automation needs plays out differently across industries, and the ROI of closing that gap varies accordingly.

Manufacturing: High-volume, PO-driven procurement means invoice matching complexity is enormous. Thousands of POs, multiple goods receipts per PO, multi-site operations with different approval hierarchies, a manufacturing ERP can store all of this, but the matching and exception-handling work is immense without automation. Hyperbots for manufacturing →

Professional Services: Time-and-material contracts, milestone billing, and project-based accruals create accounting complexity that ERPs handle at a structural level but not at an operational intelligence level. Knowing which services have been delivered but not yet invoiced requires AI discovery, not ERP configuration. ERP for professional services →

Retail: High transaction volumes, complex sales tax obligations across multiple jurisdictions, and supplier diversity make retail AP one of the highest-volume manual workloads in finance. Automation ROI in retail can be among the highest of any sector.

Healthcare: Procurement compliance and vendor credentialing requirements make vendor management automation particularly valuable in healthcare, where manual onboarding creates both operational friction and compliance risk. Automated POs in healthcare →

Wholesale and Distribution: Multi-entity operations, complex payment terms across large supplier networks, and high-volume 3-way matching make distribution a strong candidate for automation beyond ERP. Cloud ERP for wholesale distribution →

The industries served by the Hyperbots platform reflect this diversity—the AI co-pilots are configured not just for company-specific policies but for industry-specific workflows that generic ERP modules cannot replicate.

The ROI Case: Why the Automation Layer Is Where the Financial Returns Are

It is worth examining where the actual financial returns from finance transformation come from, because this is where the ERP vs automation distinction becomes most commercially important.

ERP modernization delivers ROI primarily through: reduced IT infrastructure and maintenance costs; better reporting that supports faster decision-making; elimination of duplicate or fragmented legacy systems; and improved compliance through consistent data models.

These are real savings. But they are primarily IT savings and they are relatively modest compared to the operational labor savings that finance automation delivers.

Finance automation delivers ROI through: elimination of manual invoice processing labor; reduction in duplicate and erroneous payments; capture of early payment discounts that were previously missed; reduction in late payment penalties; acceleration of month-end close; reduction in tax compliance errors and associated penalties; and faster vendor onboarding that reduces procurement lead times.

Measuring ROI in procurement automation →

The math is stark. A company processing 10,000 invoices per month at an industry benchmark cost of $15 per invoice (manual) is spending $150,000 per month on invoice processing alone. Automating 80% of that volume at $2 per invoice brings the cost to $46,000, a saving of over $100,000 per month. No ERP upgrade delivers savings of that magnitude to the finance operations function.

ROI on AI-led automation in finance →

How Hyperbots AI Co-pilots Close the Gap ERP Leaves Open

Hyperbots is an AI co-pilot platform built specifically for finance and accounting automation. It is designed to sit on top of your existing ERP whether that is NetSuite, SAP, Microsoft Dynamics, QuickBooks, Sage, Deltek Costpoint, Epicor, or any other major platform and provide the intelligent automation layer that ERPs cannot deliver on their own.

The platform delivers an average 80% reduction in operational costs and achieves 99.8% accuracy across its co-pilot suite. These are not configuration-dependent theoretical figures, they are outcomes delivered at customer sites, including the documented case of Extreme Reach (XR), which achieved 80% straight-through processing with 99.8% accuracy and zero manual touch-ups.

What makes Hyperbots genuinely different from both ERP-native automation tools and legacy AP platforms is the agentic AI architecture underneath. Rather than rules that trigger on predefined conditions, Hyperbots' co-pilots reason through transactions, applying company-specific policy, vendor history, ERP master data, and document context to make intelligent decisions on transactions they have never seen before.

The Procure-to-Pay Co-pilot Suite

The Invoice Processing Co-pilot is the most comprehensive in the market. It handles the full invoice lifecycle: autonomous discovery across email and portals, AI-native extraction with no templates required, validation against ERP data, configurable 2-way and 3-way matching, intelligent GL coding, integrated sales tax verification, and GL posting directly into the ERP. The result is that finance teams stop processing invoices and start reviewing exceptions, a fundamentally different use of their time.

The benefit is not just cost reduction. It is a qualitative shift in what the AP team does. Instead of keying data, they are reviewing AI decisions, managing vendor relationships, and driving process improvement. The team becomes a quality-control function rather than a data-entry function.

The Vendor Management Co-pilot automates the entire vendor lifecycle, onboarding, identity verification, portal communication, PO acknowledgment, remittance delivery, and invoice acceptance. Organizations that once spent weeks onboarding a new vendor can do it in hours, with higher compliance and lower fraud risk. For manufacturing and retail companies managing hundreds of active vendors, the operational impact is transformational.

The Procurement Co-pilot transforms requisition-to-PO into an autonomous workflow. AI fills missing PR fields, validates against budget controls, routes for approval based on configurable policies, and generates and dispatches POs to vendors. The traditional 3-day PR-to-PO cycle is cut to under 4 hours. For organizations where procurement delays are a real bottleneck to operations, this is a measurable competitive advantage.

The Sales Tax Verification Co-pilot is unique in the market. It validates every invoice against tax jurisdiction rules, line-item categorizations, origin-destination addresses, and economic nexus thresholds. It flags mismatches before payment, protecting against both overpayment to vendors and underpayment to tax authorities. The $200,000 in tax leakage identified for a single CFO illustrates the financial stakes.

The Payments Co-pilot brings intelligence to disbursement decisions that ERPs simply cannot provide. It recommends early payment where discounts are available, models the cash flow implications of payment timing, prevents duplicate payments through anomaly detection, and automates bank reconciliation. Organizations that actively optimize payment timing can generate meaningful working capital benefits, benefits that sit entirely in the automation layer, not the ERP.

The Accruals Co-pilot is one of the most impactful capabilities for organizations trying to accelerate month-end close. It discovers accrual candidates autonomously, goods received but not invoiced, services received under open contracts, recurring expenses without POs, calculates amounts, books journal entries, and schedules reversals. Finance teams that spend days assembling accruals in spreadsheets can close days faster with this single co-pilot.

The Order-to-Cash Co-pilot Suite

Beyond P2P, Hyperbots extends automation into the order-to-cash cycle.

The Collections Co-pilot automates AR collections workflows, monitoring overdue accounts, generating and sending dunning communications, prioritizing collection activity by risk and value, and escalating accounts that require human intervention. For organizations where DSO reduction is a priority, this co-pilot directly improves cash flow.

The Cash Application Co-pilot automatically matches incoming payments to open invoices, handling partial payments, short pays, and remittance-heavy transactions that confuse rule-based tools. Faster cash application means cleaner AR aging and more accurate cash position reporting.

Platform Capabilities That Create Transformational Impact

Several platform-level capabilities differentiate Hyperbots beyond individual co-pilot features.

The unlimited user licensing model means organizations can deploy across the entire finance team without per-seat costs that limit adoption. This is commercially significant: most automation ROI models assume full deployment, but per-user pricing often constrains rollout in practice.

The pre-trained, ready-to-deploy models mean finance teams go live in days, not months. Unlike ERP implementations that take quarters, Hyperbots leverages finance-domain AI that arrives with deep knowledge of invoice formats, accounting conventions, and procurement processes already embedded.

The self-learning AI means accuracy improves over time as the system learns from feedback, approvals, and exception patterns. This is the opposite of rules-based automation, which degrades as processes evolve and exceptions multiply.

The explainable AI architecture means every AI decision comes with an audit trail that explains why it was made essential for CFO-level auditability and compliance readiness.

ROI Delivered Across P2P and O2C

The quantified outcomes from Hyperbots implementations speak for themselves:

80%+ straight-through processing rate for invoices (vs. industry average of 30–50%)

99.8% invoice extraction accuracy

80% reduction in operational costs across finance workflows

PR-to-PO cycle time: 3 days reduced to under 4 hours

$200,000+ in tax leakage identified and recovered for a single CFO

Month-end close acceleration through automated accrual discovery and booking

DSO reduction through automated collections workflows

Working capital optimization through AI-driven payment timing

For manufacturing companies, the PO-matching and procurement automation capabilities are particularly valuable. For retail, sales tax verification and high-volume invoice processing dominate the ROI case. For professional services, accruals automation and collections are the highest-impact deployments.

You can model your own ROI using Hyperbots' suite of ROI calculators which covers invoice processing, procurement, payments, vendor management, accruals, collections, cash application, and more.

The Strategic Question for Finance Leaders

Every CFO evaluating a finance transformation investment needs to ask a clear-eyed question: "Where is the manual work in my team's day, and what is causing it?"

If the answer is outdated systems, fragmented data, or poor reporting visibility, ERP modernization addresses that. If the answer is people manually processing invoices, chasing approvals, assembling accruals, verifying tax, and managing vendor data, finance automation addresses that.

For most finance organizations, the honest answer is both. But the operational cost savings, the ability to do more with the same headcount or to reduce headcount while improving quality, lives primarily in the automation layer. That is where the 80% cost reduction numbers come from. That is where the 99.8% accuracy gains come from. That is where the month-end close acceleration comes from.

Finance automation software: the definitive 2025 guide →

ERP modernization is necessary. But it is not sufficient. The organizations that will lead in finance efficiency over the next decade are those that build both layer, a modern ERP as the system of record, and an intelligent AI co-pilot layer as the system of action.

The gap between what ERP systems do and what finance teams actually need has never been more clearly defined or more readily closable. The technology to bridge it exists today, deploys in weeks, and pays for itself within months. Book a demo with Hyperbots to see how you can enhance your current financial operations.

The only remaining question is when you build the automation layer, not whether.

Frequently Asked Questions

Q1: Can we implement finance automation before completing our ERP modernization?

Yes, and in many cases it makes sense to do so. Hyperbots and similar AI co-pilot platforms connect to existing ERPs through standard APIs and pre-built connectors. You do not need to complete an ERP upgrade before deploying automation. In fact, automation often helps organizations capture ROI faster than waiting for a multi-year ERP modernization to complete. That said, a modern ERP with cleaner APIs and better data structures will make the automation layer more effective over time.

Q2: Does finance automation replace the ERP?

No. Finance automation complements the ERP, not replace it. The ERP remains the system of record for all financial data. The automation layer reads from the ERP, processes documents and decisions, and writes results back. The ERP's job (holding the truth) and the automation layer's job (acting on that truth) are complementary, not competing.

Q3: How long does it take to see results from AI co-pilot deployment?

Because platforms like Hyperbots use pre-trained, finance-domain AI models, deployment timelines are measured in days to weeks rather than months. Many organizations see measurable STP rate improvements within the first month of going live. This is fundamentally different from ERP implementations, which typically take six to eighteen months before delivering business value.

Q4: What is straight-through processing (STP) and why does it matter?

STP refers to the percentage of invoices (or other transactions) that flow from receipt to posting without any human intervention. Industry averages for manual organizations are 30–50%. Hyperbots customers achieve 80%+. The difference directly translates to labor cost: at 80% STP on a 10,000-invoice-per-month volume, the AP team handles 2,000 exceptions rather than 10,000 transactions. That is a structural reduction in headcount requirement or a structural expansion in processing capacity.

Q5: How does AI-based finance automation differ from RPA (Robotic Process Automation)?

RPA automates rules-based repetitive tasks by mimicking human clicks in a user interface. It is brittle, any change to the interface or process breaks the bot. It handles no exceptions. AI-based automation understands document content, applies contextual reasoning, learns from feedback, and handles novel transactions gracefully. RPA in accounts payable—still viable? →

Q6: Does Hyperbots work with our existing ERP?

Hyperbots has pre-built integrations for all major ERP platforms including SAP, Oracle NetSuite, Microsoft Dynamics (GP and 365), QuickBooks, Sage (300 and Intacct), Deltek Costpoint, Epicor, and others. The integrations page provides the full list.

Q7: What is the difference between Hyperbots and tools like Ramp or Tipalti?

Ramp is primarily a spend management and corporate card platform. Tipalti is a global payments platform. Neither offers the depth of ERP-integrated, agentic AI automation that Hyperbots provides across the full P2P and O2C stack. Hyperbots achieves 99.8% invoice accuracy versus Tipalti's lower rates, and covers a broader set of finance processes including accruals, sales tax verification, and procurement—areas where Ramp and Tipalti have limited or no capability. Hyperbots vs Tipalti: full comparison →